Bathroom Furniture Market Size

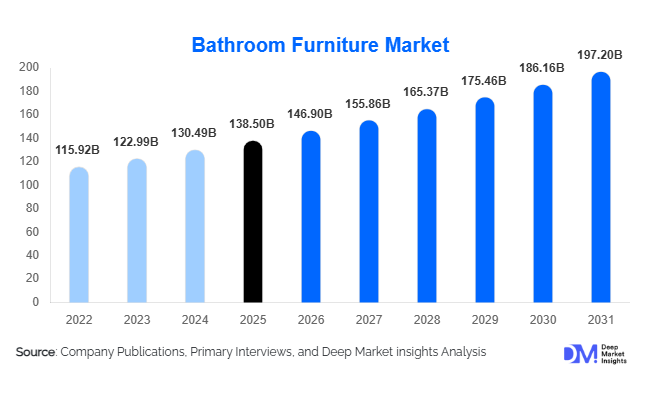

According to Deep Market Insights, the global bathroom furniture market size was valued at USD 138.5 billion in 2025 and is projected to grow from USD 146.9 billion in 2026 to reach USD 197.2 billion by 2031, expanding at a CAGR of 6.1% during the forecast period (2026–2031). The bathroom furniture market growth is primarily driven by rapid urbanization, increasing residential construction activities, rising home renovation spending, and growing consumer preference for aesthetically designed and space-efficient bathroom interiors.

Bathroom furniture includes vanities, cabinets, mirror cabinets, storage units, and modular furniture systems designed to enhance both functionality and aesthetics in bathrooms. With the global housing sector expanding and interior design trends evolving, bathrooms are increasingly viewed as lifestyle spaces rather than purely functional areas. This transformation has significantly boosted demand for modern furniture solutions that integrate storage, design, and technology.

Key Market Insights

- Bathroom vanities represent the largest product segment, accounting for more than 40% of global demand due to their combined functionality and storage benefits.

- Residential construction and home renovation projects are the primary demand drivers, contributing nearly 70% of the total market revenue.

- North America dominates the global market, supported by strong home improvement spending and premium interior design adoption.

- Asia-Pacific is the fastest-growing region, driven by urbanization, rising disposable income, and expanding housing development in China and India.

- Smart and modular bathroom furniture solutions are gaining traction as consumers demand integrated lighting, smart mirrors, and compact storage systems.

- Online furniture retail platforms are expanding rapidly, enabling consumers to access customized bathroom furniture products with transparent pricing and convenient delivery.

What are the latest trends in the bathroom furniture market?

Smart Bathroom Furniture Integration

The adoption of smart home technologies is gradually influencing bathroom furniture design. Manufacturers are introducing LED mirrors with touch controls, anti-fog technology, Bluetooth connectivity, and motion-activated lighting. Smart vanities with integrated charging ports, temperature-controlled drawers, and digital displays are becoming increasingly popular in luxury residential and hospitality projects. These innovations not only enhance convenience but also improve the overall bathroom experience. The growing popularity of connected homes and digital ecosystems is expected to accelerate the integration of IoT-enabled furniture components, positioning smart bathroom furniture as a premium segment within the broader market.

Space-Efficient and Modular Furniture Designs

Urban housing trends are driving the demand for compact and modular bathroom furniture solutions. Floating vanities, wall-mounted cabinets, and integrated storage units are increasingly preferred in modern apartments where space optimization is critical. Modular furniture systems allow homeowners to customize storage layouts while maintaining minimalist aesthetics. Manufacturers are also developing moisture-resistant materials and durable coatings to improve product longevity in humid bathroom environments. The shift toward flexible furniture designs is enabling manufacturers to target a broader range of consumers, including urban apartment residents and renovation-focused homeowners seeking efficient storage solutions.

What are the key drivers in the bathroom furniture market?

Growth in Residential Construction

The expansion of global residential construction is one of the most significant drivers for the bathroom furniture market. Rapid urbanization in emerging economies such as China, India, Indonesia, and Brazil has resulted in a large number of new housing developments. Each residential unit requires bathroom fixtures and furniture installations, creating strong demand for vanities, cabinets, and storage units. Developers are increasingly delivering fully equipped bathrooms with pre-installed furniture systems to enhance property value and attract buyers, further boosting market demand.

Rising Home Renovation and Remodeling Activities

Home renovation spending has increased significantly in developed economies, particularly in North America and Europe. Bathrooms are among the most frequently remodeled spaces within residential properties. Consumers are investing in modern vanities, mirror cabinets, and designer furniture to improve aesthetics and functionality. Renovation-driven demand is also supported by the growing popularity of DIY home improvement culture and the availability of modular furniture products that can be installed without extensive construction work.

What are the restraints for the global market?

Volatility in Raw Material Prices

The bathroom furniture industry relies heavily on materials such as wood, engineered boards, metal, glass, and stone composites. Fluctuations in timber prices, steel costs, and transportation expenses can significantly impact manufacturing costs and profit margins. Environmental regulations related to sustainable forestry practices have also increased raw material costs in some regions. These factors can influence product pricing and affect the affordability of bathroom furniture products for consumers.

Supply Chain Disruptions

Global supply chain challenges continue to impact furniture manufacturing and distribution. Delays in raw material procurement, logistics disruptions, and rising shipping costs can lead to longer lead times and higher product prices. Manufacturers that rely on international supply chains may experience inventory shortages and production delays, particularly during periods of global trade instability.

What are the key opportunities in the bathroom furniture industry?

Expansion in Emerging Housing Markets

Rapid urbanization and population growth in emerging economies present significant opportunities for bathroom furniture manufacturers. Countries such as India, Vietnam, Indonesia, and Saudi Arabia are experiencing strong residential construction growth. Government housing initiatives and rising middle-class incomes are increasing demand for modern bathroom interiors. Establishing regional manufacturing facilities and localized distribution networks can help companies capture market share in these high-growth regions.

Growth of Technology-Integrated Bathroom Furniture

The integration of smart technologies into bathroom furniture presents a major opportunity for manufacturers to differentiate their products and enter premium market segments. LED mirrors, voice-enabled controls, motion sensors, and smart storage systems are increasingly being incorporated into bathroom furniture designs. As consumers adopt connected home ecosystems, the demand for technologically advanced furniture solutions is expected to grow steadily.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 138.5 Billion |

| Market Size in 2026 | USD 146.9 Billion |

| Market Size in 2031 | USD 197.2 Billion |

| CAGR | 6.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Bathroom vanities represent the largest product segment in the market, accounting for approximately 40% of global revenue in 2025. These products combine sink support with storage functionality, making them essential components of modern bathroom interiors. Double-sink vanities are particularly popular in larger residential homes and luxury apartments, while compact single-sink vanities dominate urban apartment installations. Bathroom cabinets and storage units also represent a significant share of the market, providing organized storage solutions for toiletries, towels, and cleaning supplies. Mirror cabinets with integrated lighting are gaining popularity as multifunctional furniture products that combine storage, reflection, and lighting in a single unit.

Application Insights

The residential sector represents the dominant application segment for bathroom furniture, accounting for nearly 70% of global demand. New housing developments and home renovation projects are the primary drivers for this segment. Commercial applications such as hotels, offices, healthcare facilities, and retail complexes also contribute significantly to market demand. Hospitality infrastructure expansion has increased procurement of durable and aesthetically appealing bathroom furniture solutions designed for high-traffic environments. Healthcare facilities require hygienic and moisture-resistant furniture products, while corporate offices and commercial buildings demand modern bathroom storage systems that complement overall interior design.

Distribution Channel Insights

Offline retail channels remain the dominant distribution channel for bathroom furniture, accounting for more than 60% of global sales. Consumers often prefer to physically inspect furniture products before making purchasing decisions, particularly when evaluating material quality and finishing. Specialty bathroom showrooms and home improvement retailers play a key role in product sales. However, online retail platforms are expanding rapidly as e-commerce adoption increases. Direct-to-consumer websites and online marketplaces allow customers to compare designs, access customization options, and benefit from competitive pricing. Digital marketing and influencer-driven interior design trends are further accelerating online sales growth.

Explore more data points, trends and opportunities Download Free Sample Report

Bathroom Furniture Market Segmentations

By Product Type

- Bathroom Vanities

- Bathroom Cabinets

- Bathroom Storage Units

- Mirror Cabinets & LED Mirrors

- Modular Bathroom Furniture Sets

By Material Type

- Solid Wood

- Engineered Wood

- Metal

- Stone & Composite Materials

- Plastic & Polymer Composites

By Installation Type

- Freestanding Bathroom Furniture

- Wall-Mounted Bathroom Furniture

- Modular/Custom-Built Bathroom Furniture

By Distribution Channel

- Online Retail

- Furniture & Home Improvement Stores

- Specialty Bathroom Showrooms

- Contract/B2B Sales

By End-Use Industry

- Residential Housing

- Hospitality (Hotels & Resorts)

- Commercial Offices

- Healthcare Facilities

- Educational Institutions

Regional Insights

North America

North America holds approximately 32% of the global bathroom furniture market in 2025. The United States dominates regional demand due to strong home renovation spending and high consumer preference for premium interior design products. Rising investments in smart home upgrades and luxury residential construction are further boosting demand for technologically advanced bathroom furniture solutions. Canada also contributes significantly to regional demand through urban housing developments and remodeling activities.

Europe

Europe accounts for nearly 28% of the global market, with major demand centers including Germany, Italy, the United Kingdom, and France. European consumers prioritize design quality, sustainability, and premium craftsmanship. Many European manufacturers specialize in luxury bathroom furniture products made from high-quality wood, stone, and composite materials. Strong export activity from Italy and Germany further strengthens Europe’s position in the global market.

Asia-Pacific

Asia-Pacific represents about 27% of the global market and is the fastest-growing region. China leads regional demand due to its large construction sector and growing middle-class population. India is emerging as another high-growth market as urban housing projects and government-backed infrastructure initiatives expand. Rising disposable incomes and increasing interest in modern home interiors are supporting the adoption of premium bathroom furniture products across the region.

Latin America

Latin America holds roughly 6% of the global market share, with Brazil and Mexico representing the largest demand centers. Urbanization and residential development are gradually increasing the adoption of modern bathroom furniture products. Rising consumer interest in interior design and lifestyle improvements is expected to support long-term market growth in the region.

Middle East & Africa

The Middle East & Africa region accounts for approximately 7% of the global market. Countries such as Saudi Arabia and the United Arab Emirates are investing heavily in luxury real estate and hospitality infrastructure, creating demand for high-end bathroom furniture products. Tourism development projects and large-scale commercial construction initiatives are also contributing to regional market expansion.

Key Players in the Bathroom Furniture Market

- Kohler Co.

- TOTO Ltd.

- LIXIL Group Corporation

- Duravit AG

- Roca Sanitario S.A.

- American Woodmark Corporation

- IKEA

- Masco Corporation

- Geberit Group

- Ideal Standard International

- Scavolini S.p.A

- Porcelanosa Grupo

- Oppein Home Group

- Hettich Holding GmbH

- Godrej Interio