Basketball Market Size

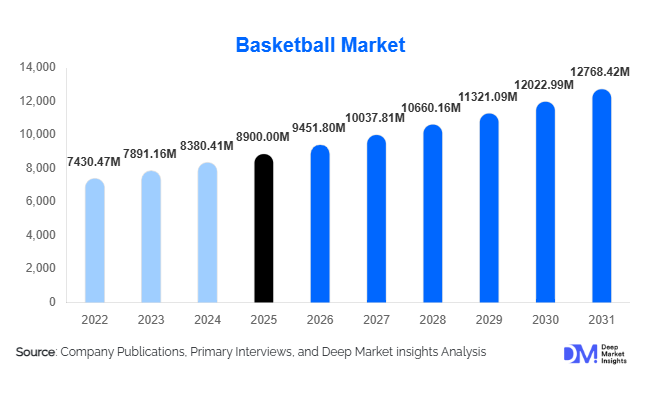

According to Deep Market Insights, the global basketball market size was valued at USD 8,900 million in 2025 and is projected to grow from USD 9,451.80 million in 2026 to reach USD 12,768.42 million by 2031, expanding at a CAGR of 6.2% during the forecast period (2026–2031). The basketball market growth is primarily driven by increasing global participation in sports, the rising popularity of professional leagues, and the expanding influence of basketball-inspired lifestyle apparel and footwear. The integration of e-commerce platforms and growing investments in sports infrastructure across emerging economies are further accelerating market expansion.

Key Market Insights

- Basketball is transitioning into a hybrid sports-lifestyle market, with footwear and apparel driving significant revenue growth beyond performance use.

- North America dominates the global market, supported by a strong sports culture, high consumer spending, and established professional leagues.

- Asia-Pacific is the fastest-growing region, fueled by youth participation, urbanization, and rising disposable income.

- Mid-range products account for the largest share, balancing affordability and quality for mass adoption.

- E-commerce channels are rapidly expanding, offering wider product accessibility and competitive pricing.

- Technological innovations, including smart basketballs and performance tracking tools, are reshaping training and engagement.

What are the latest trends in the basketball market?

Rise of Athleisure and Lifestyle Integration

Basketball products, particularly footwear and apparel, are increasingly being adopted as lifestyle fashion. Influencer collaborations, celebrity endorsements, and limited-edition product launches are driving demand beyond traditional sports usage. Consumers, especially in urban markets, are prioritizing style alongside performance, contributing to premiumization. This trend is significantly expanding the total addressable market by attracting non-athlete consumers and increasing repeat purchases. The blending of streetwear culture with basketball branding has also strengthened brand loyalty and elevated pricing power for leading manufacturers.

Adoption of Smart and Connected Equipment

The integration of technology into basketball equipment is gaining momentum. Smart basketballs equipped with sensors, mobile apps for performance tracking, and AI-driven coaching tools are enhancing training efficiency. These innovations are particularly appealing to younger and tech-savvy consumers who seek data-driven insights into their performance. Additionally, digital platforms offering virtual coaching and analytics are expanding the ecosystem around basketball, creating new revenue streams for companies investing in sports technology.

What are the key drivers in the basketball market?

Increasing Global Sports Participation

The growing emphasis on health and fitness has significantly increased participation in sports activities, including basketball. Educational institutions and community programs are incorporating basketball into their sports curricula, driving consistent demand for equipment and apparel. This trend is particularly strong in emerging economies, where governments are promoting sports as part of public health initiatives.

Influence of Professional Leagues and Media Exposure

The global reach of professional basketball leagues and tournaments has enhanced the sport’s visibility and popularity. Broadcasting rights, digital streaming, and social media engagement have expanded audience reach, influencing consumer purchasing behavior. Aspiring players and fans are increasingly adopting branded products, driving demand across premium and mid-range segments.

What are the restraints for the global market?

Intense Price Competition

The basketball market faces significant competition from both global and regional players, particularly in the mid-range and economy segments. Price sensitivity among consumers limits margin expansion and creates challenges for smaller players to differentiate their offerings. Frequent discounting and promotional strategies further intensify competition, impacting overall profitability.

Volatility in Raw Material Costs

Fluctuations in the prices of rubber, synthetic leather, and other raw materials directly affect production costs. This volatility leads to pricing instability and margin pressures for manufacturers. Companies must continuously optimize supply chains and explore alternative materials to mitigate cost impacts and maintain competitiveness.

What are the key opportunities in the basketball industry?

Expansion in Emerging Markets

Emerging economies such as China, India, and African nations present significant growth opportunities due to increasing youth participation and government investments in sports infrastructure. Urbanization and rising disposable incomes are further supporting demand for basketball products. Companies can capitalize on this opportunity by offering affordable and localized products tailored to regional preferences.

Technological Integration in Sports Equipment

The development of smart basketballs, wearable devices, and digital training platforms offers substantial growth potential. These technologies enable players to track performance metrics and improve skills, creating demand for premium, tech-enabled products. Partnerships with technology firms and investments in R&D can help companies gain a competitive edge in this segment.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8900 Million |

| Market Size in 2026 | USD 9451.80 Million |

| Market Size in 2031 | USD 12768.42 Million |

| CAGR | 6.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Basketballs remain the leading product segment in the global basketball market, accounting for approximately 30% of total market share in 2025. The dominance of this segment is primarily driven by high replacement cycles, as basketballs experience regular wear and tear across both indoor and outdoor usage. Institutional procurement from schools, colleges, and sports academies further sustains recurring demand. Additionally, the expansion of grassroots programs and recreational leagues globally continues to drive volume sales, particularly in emerging markets where affordability and accessibility are key. The increasing adoption of durable synthetic and composite leather basketballs has also enhanced product lifespan, balancing replacement demand with performance expectations.

Basketball footwear and apparel collectively represent a significant and rapidly evolving segment, supported by their strong crossover into lifestyle and athleisure markets. Premium basketball sneakers, often endorsed by professional athletes and influencers, are witnessing high demand not only among players but also among fashion-conscious consumers. This segment benefits from higher margins and frequent product launches, including limited-edition collections that drive repeat purchases. Apparel, including jerseys, shorts, and compression wear, continues to gain traction due to its dual utility in sports and casual wear. Basketball equipment, including hoops, backboards, rims, and accessories, is experiencing steady growth driven by increasing investments in sports infrastructure and home-based recreational setups. The rising popularity of portable and adjustable basketball systems, particularly in residential settings, is a key growth driver. Accessories such as pumps, protective gear, and training aids further contribute to incremental revenue, supported by growing consumer awareness around performance optimization and injury prevention.

Application Insights

The recreational and amateur segment leads the basketball market, accounting for nearly 40% of total demand in 2025. This dominance is driven by widespread participation at community levels, urban recreational activities, and increasing interest in fitness-oriented sports. The accessibility of basketball, requiring minimal infrastructure compared to other sports, makes it highly popular across diverse demographics and geographies. The institutional segment, comprising schools, colleges, and training academies, represents a substantial share of the market. Growth in this segment is fueled by government-backed sports initiatives, curriculum integration, and rising investments in educational sports infrastructure. Bulk procurement of equipment and uniforms by institutions ensures stable demand and long-term contracts for manufacturers.

The professional segment, while smaller in volume, plays a critical role in driving premium product demand and brand visibility. High-performance basketballs, footwear, and apparel are designed specifically for professional use, commanding higher price points and margins. This segment also influences consumer preferences through endorsements and media exposure. The youth segment is the fastest-growing end-use category, with a projected CAGR exceeding 7%. Growth is driven by grassroots development programs, increasing sports participation among children, and rising parental awareness of physical fitness. Emerging applications such as basketball-based fitness training, rehabilitation programs, and sports therapy are further expanding the market scope and creating new demand avenues.

Distribution Channel Insights

Offline retail channels continue to dominate the basketball market, accounting for approximately 60% of total sales in 2025. The leading position of offline channels is driven by consumer preference for physical product inspection, trial, and immediate availability, particularly for footwear and equipment. Sporting goods stores, specialty outlets, and large-format retail chains remain key distribution points, offering personalized customer service and brand experiences.

However, online retail is the fastest-growing distribution channel, supported by increasing internet penetration, smartphone usage, and the convenience of digital shopping. E-commerce platforms provide access to a wide range of products, competitive pricing, and customer reviews, influencing purchasing decisions. Brand-owned websites are also gaining traction as companies adopt direct-to-consumer (D2C) strategies to improve margins and customer engagement. The emergence of omnichannel retail strategies, integrating online and offline experiences, is reshaping distribution dynamics. Features such as click-and-collect, virtual product trials, and personalized recommendations are enhancing customer satisfaction and driving sales growth across both channels.

Explore more data points, trends and opportunities Download Free Sample Report

Basketball Market Segmentations

By Product Type

- Basketballs

- Basketball Footwear

- Basketball Apparel

- Basketball Equipment

- Accessories

By Application

- Professional Players & Leagues

- Institutional

- Recreational & Amateur Users

- Youth & Kids

By Distribution Channel

- Online Retail

- Sporting Goods Stores

- Specialty Stores

- Supermarkets & Hypermarkets

By Material Type

- Rubber

- Synthetic/Composite Leather

- Genuine Leather

- Polyurethane & Advanced Materials

By Price Segment

- Economy

- Mid-Range

- Premium

Regional Insights

North America

North America remains the largest regional market, accounting for approximately 35% of global revenue in 2025, with the United States as the dominant contributor. The region’s leadership is driven by a deep-rooted basketball culture, high participation rates, and the presence of established professional leagues. Strong consumer spending power and brand loyalty further support premium product adoption. Additionally, extensive school and collegiate sports programs create sustained demand for equipment and apparel. The growth of athleisure trends and the influence of sports celebrities continue to drive footwear and apparel sales, reinforcing the region’s dominance.

Asia-Pacific

Asia-Pacific accounts for approximately 28% of the global market and is the fastest-growing region, with a CAGR of around 7.5%. China leads the regional market, contributing nearly 40% of APAC demand, driven by large-scale youth participation, government sports initiatives, and increasing urbanization. India is the fastest-growing country, with an estimated growth rate of 8%, supported by rising sports awareness, expanding middle-class income, and investments in sports infrastructure. The region also benefits from its role as a manufacturing hub, enabling cost-effective production and export-driven growth.

Europe

Europe holds approximately 20% of the global basketball market, with countries such as Spain, France, and Germany leading demand. Growth in this region is driven by strong club-level participation, government funding for sports development, and the increasing popularity of organized leagues. The rising adoption of basketball-inspired lifestyle products, particularly footwear and apparel, is further boosting market expansion. Additionally, the region’s focus on health and fitness is encouraging greater participation in recreational sports, supporting steady demand growth.

Latin America

Latin America accounts for around 8% of the global market, with Brazil and Argentina as key contributors. Market growth is supported by urbanization, increasing youth engagement in sports, and the expansion of community-level recreational activities. Economic improvements in select countries are enabling higher spending on sports goods. Additionally, growing media exposure and international sports events are enhancing the popularity of basketball, contributing to increased demand for equipment and apparel.

Middle East & Africa

The Middle East & Africa region holds approximately 9% of the global market, with growth driven by government investments in sports infrastructure, rising urban development, and increasing focus on youth engagement. Countries such as the UAE and South Africa are leading markets, supported by improved facilities and international sporting events. In the Middle East, high disposable income and a preference for premium products are driving demand for branded footwear and apparel. In Africa, grassroots programs and international partnerships are promoting basketball participation, creating long-term growth opportunities for the market.