Bamboo Pulp Market Size

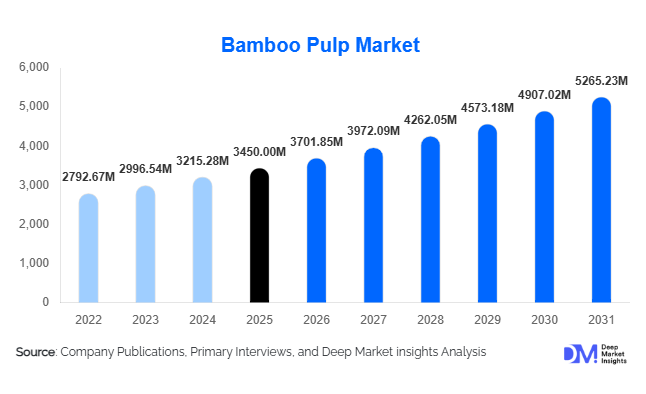

According to Deep Market Insights, the global bamboo pulp market size was valued at USD 3,450 million in 2025 and is projected to grow from USD 3,701.85 million in 2026 to reach USD 5,265.23 million by 2031, expanding at a CAGR of 7.3% during the forecast period (2026–2031). The growth of the bamboo pulp market is primarily driven by increasing demand for sustainable raw materials, the rising substitution of wood pulp, and expanding applications in packaging, textiles, and hygiene products.

Key Market Insights

- Bamboo pulp is emerging as a key sustainable alternative to wood pulp, supported by its fast renewability and lower environmental footprint.

- Packaging applications dominate global demand, driven by regulatory pressure to reduce plastic usage and adopt biodegradable materials.

- Asia-Pacific dominates the global market, led by China and India, due to abundant raw material availability and strong manufacturing capacity.

- Textile-grade bamboo pulp is the fastest-growing segment, fueled by increasing demand for eco-friendly fibers such as viscose rayon.

- Technological advancements in pulping processes are improving yield efficiency and expanding industrial applications.

- Export-driven demand from Europe and North America is accelerating global trade flows, particularly from Asian producers.

What are the latest trends in the bamboo pulp market?

Shift Toward Sustainable Packaging Materials

The global transition toward sustainable packaging is significantly influencing bamboo pulp demand. Companies across the food, retail, and e-commerce sectors are adopting biodegradable materials to comply with environmental regulations and meet consumer expectations. Bamboo pulp-based packaging offers strength, flexibility, and compostability, making it suitable for applications such as corrugated boxes, food containers, and molded packaging. This trend is further supported by bans on single-use plastics in several countries, pushing manufacturers to invest in bamboo pulp as a renewable alternative. Additionally, innovations in barrier coatings and moisture resistance are enhancing the performance of bamboo-based packaging solutions, enabling broader adoption across industries.

Expansion of Bamboo-Based Textile Fibers

The textile industry is witnessing a rapid shift toward sustainable fibers, with bamboo pulp playing a crucial role in viscose rayon production. Bamboo-derived fibers are valued for their softness, breathability, and antibacterial properties, making them ideal for apparel and home textiles. Global fashion brands are increasingly integrating bamboo fibers into their product lines to meet sustainability commitments. This trend is particularly prominent in the Asia-Pacific region, where textile manufacturing hubs are investing in bamboo pulp processing technologies. The rise of eco-conscious consumers and regulatory pressure on synthetic fibers is further accelerating the adoption of bamboo-based textiles.

What are the key drivers in the bamboo pulp market?

Rising Demand for Eco-Friendly Raw Materials

Environmental concerns related to deforestation and carbon emissions are driving the adoption of bamboo pulp as a sustainable alternative to wood pulp. Bamboo’s rapid growth cycle and high yield per hectare make it an environmentally viable option. Governments and corporations are increasingly prioritizing renewable resources, boosting demand for bamboo pulp across multiple industries.

Growth of E-commerce and Packaging Industry

The expansion of e-commerce has significantly increased demand for packaging materials, particularly sustainable options. Bamboo pulp-based packaging provides durability and biodegradability, making it a preferred choice for logistics and retail sectors. The growing volume of online shipments is directly contributing to increased consumption of bamboo pulp globally.

Technological Advancements in Pulp Processing

Innovations in chemical and mechanical pulping techniques are enhancing production efficiency and reducing costs. Improved fiber quality and consistency are expanding the applicability of bamboo pulp in high-performance products. These advancements are making bamboo pulp more competitive with traditional wood pulp.

What are the restraints for the global market?

Limited Global Supply Chain Infrastructure

Despite abundant bamboo resources in Asia, the global supply chain for bamboo pulp remains underdeveloped in other regions. Limited processing facilities and logistical challenges restrict market expansion in North America and Europe, creating dependency on imports.

High Initial Investment and Cost Volatility

The establishment of bamboo pulp processing facilities requires significant capital investment. Additionally, fluctuations in raw material availability and energy costs can impact pricing stability, posing challenges for market participants.

What are the key opportunities in the bamboo pulp industry?

Growth in Sustainable Packaging Solutions

The increasing global focus on reducing plastic waste presents significant opportunities for bamboo pulp manufacturers. Companies can capitalize on this trend by developing innovative packaging solutions tailored to the food, retail, and e-commerce industries. Government regulations promoting biodegradable materials further enhance this opportunity.

Expansion in Textile Applications

The rising demand for eco-friendly textiles is creating new growth avenues for bamboo pulp in viscose fiber production. Manufacturers investing in textile-grade pulp can tap into the growing sustainable fashion market, particularly in Asia and Europe.

Government Support and Policy Initiatives

Government initiatives promoting bamboo cultivation and sustainable forestry are strengthening the supply chain and encouraging investments. Policies aimed at rural development and carbon reduction are creating a favorable environment for market expansion.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3450 Million |

| Market Size in 2026 | USD 3701.85 Million |

| Market Size in 2031 | USD 5265.23 Million |

| CAGR | 7.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Bleached bamboo pulp dominates the global market, accounting for approximately 48% of the total market share in 2025. This leadership position is primarily driven by its superior brightness, higher purity levels, and enhanced fiber consistency, making it highly suitable for premium applications such as printing & writing paper, tissue products, and hygiene-grade materials. The increasing global demand for high-quality, eco-friendly paper products, particularly in developed markets, continues to reinforce the dominance of bleached pulp. Additionally, advancements in environmentally friendly bleaching technologies (such as elemental chlorine-free processes) are further supporting adoption. Meanwhile, unbleached and semi-bleached bamboo pulp are gaining traction, particularly in cost-sensitive and sustainability-focused applications like packaging and industrial paper. These variants benefit from lower processing costs and reduced chemical usage, aligning well with the growing demand for low-impact manufacturing solutions.

Application Insights

Paper and paperboard applications lead the bamboo pulp market, accounting for approximately 52% of the total market share in 2025. This dominance is largely driven by the rapid expansion of sustainable packaging solutions across various industries, including e-commerce, food & beverage, and consumer goods. Bamboo pulp offers high strength and biodegradability, making it an ideal substitute for conventional wood pulp in packaging materials. Tissue and hygiene products form a significant sub-segment within this category, supported by increasing consumer preference for eco-friendly and chemical-free personal care products. Additionally, the textile segment is emerging as the fastest-growing application, driven by rising demand for bamboo-based viscose fibers. The global shift toward sustainable fashion, coupled with the superior softness, breathability, and antibacterial properties of bamboo fibers, is accelerating adoption in the apparel and home textile industries.

Distribution Channel Insights

Direct B2B sales dominate the bamboo pulp market, accounting for over 65% of total distribution in 2025. This dominance is driven by the need for consistent quality, bulk procurement, and long-term pricing stability among large-scale manufacturers in the packaging, paper, and textile industries. Direct contracts between pulp producers and end-use manufacturers enable better supply chain integration, reduced procurement costs, and assured raw material availability. This model is particularly prevalent in the Asia-Pacific region, where vertically integrated supply chains are common. Distributors and traders play a complementary role, especially in regions such as Europe and North America, where local production is limited, and reliance on imports is high. These intermediaries facilitate market access, manage logistics, and support smaller buyers who lack direct procurement capabilities.

End-Use Industry Insights

The packaging industry remains the largest end-use segment, contributing nearly 40% of total market demand in 2025. This leadership is driven by stringent global regulations aimed at reducing plastic waste, along with the exponential growth of e-commerce, requiring sustainable packaging materials. Bamboo pulp’s biodegradability and strength make it a preferred choice for corrugated packaging, molded fiber products, and food-grade containers. The textile industry is the fastest-growing segment, expanding at a CAGR exceeding 9%, fueled by increasing adoption of bamboo-based fibers in sustainable apparel and home textiles. The personal care and hygiene sector is also experiencing steady growth, supported by rising consumer awareness regarding eco-friendly tissue, wipes, and sanitary products. Furthermore, emerging applications in biodegradable composites, specialty papers, and industrial filtration materials are broadening the scope of bamboo pulp usage, contributing to long-term market expansion.

Explore more data points, trends and opportunities Download Free Sample Report

Bamboo Pulp Market Segmentations

By Product Type

- Bleached Bamboo Pulp

- Unbleached Bamboo Pulp

- Semi-Bleached Bamboo Pulp

By Application

- Paper & Paperboard

- Textile Fibers

- Tissue & Hygiene Products

- Specialty Applications

By Distribution Channel

- Direct B2B Sales

- Distributors & Traders

By End-Use Industry

- Packaging Industry

- Textile Industry

- Personal Care & Hygiene

- Printing & Publishing

- Industrial & Specialty Applications

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global bamboo pulp market, accounting for approximately 62% of the total market share in 2025. China leads the region, contributing over 40% of global production, driven by abundant bamboo resources, well-established processing infrastructure, and strong domestic demand across the packaging and textile industries. India is emerging as a high-growth market due to government initiatives promoting bamboo cultivation, such as national bamboo missions and rural development programs. Southeast Asian countries, including Indonesia and Vietnam, are also expanding production capacities. Key growth drivers in the region include low raw material costs, availability of skilled labor, strong export orientation, and increasing investments in sustainable manufacturing technologies.

Europe

Europe holds approximately 18% of the global market share, primarily driven by stringent environmental regulations and strong demand for sustainable and biodegradable materials. Countries such as Germany, France, and Sweden are major consumers, with significant reliance on imports from Asia due to limited domestic bamboo resources. The European Union’s policies on single-use plastics and carbon neutrality are accelerating the adoption of bamboo pulp in packaging and hygiene applications. Additionally, increasing consumer preference for eco-labeled products and corporate sustainability commitments are key drivers supporting regional market growth.

North America

North America accounts for around 12% of the global bamboo pulp market, with the United States leading regional demand. Growth in this region is driven by rising awareness of sustainable materials, increasing adoption in packaging and personal care products, and strong demand from environmentally conscious consumers. However, limited domestic bamboo cultivation and processing infrastructure result in high dependence on imports, primarily from Asia. The presence of large packaging and consumer goods companies adopting sustainability goals is a key driver, along with regulatory support for reducing plastic usage and promoting biodegradable alternatives.

Latin America

Latin America represents an emerging market for bamboo pulp, with countries such as Brazil and Mexico leading regional demand. Growth is supported by increasing industrialization, rising awareness of sustainable materials, and expanding packaging industries. The region also has favorable climatic conditions for bamboo cultivation, creating potential for future supply chain development. Government initiatives promoting sustainable forestry and renewable resources are expected to drive long-term growth, along with increasing investments in pulp processing infrastructure.

Middle East & Africa

The Middle East & Africa region is gradually adopting bamboo pulp, driven by increasing investments in sustainable materials and infrastructure development. Demand is primarily concentrated in packaging and industrial applications, particularly in countries such as the UAE, Saudi Arabia, and South Africa. Growth drivers include rising urbanization, expansion of retail and e-commerce sectors, and growing awareness of environmental sustainability. Although the region currently relies heavily on imports, increasing interest in sustainable alternatives and government-led diversification strategies are expected to create new growth opportunities in the coming years.

Key Players in the Bamboo Pulp Market

- Nine Dragons Paper Holdings

- Shandong Sun Paper Industry

- Sichuan Yongfeng Paper

- Yibin Paper Industry

- Lee & Man Paper Manufacturing

- Guangdong Dingfeng Paper

- Jiangxi Lianxing Paper

- Hunan Tiger Forest & Paper

- Guizhou Chitianhua Paper

- Guangxi Fenglin Wood Industry

- Xiamen C&D Paper & Pulp

- Asia Pulp & Paper

- Domtar Corporation

- Sappi Limited

- Stora Enso