Bamboo Fiber Tableware and Kitchenware Market Size

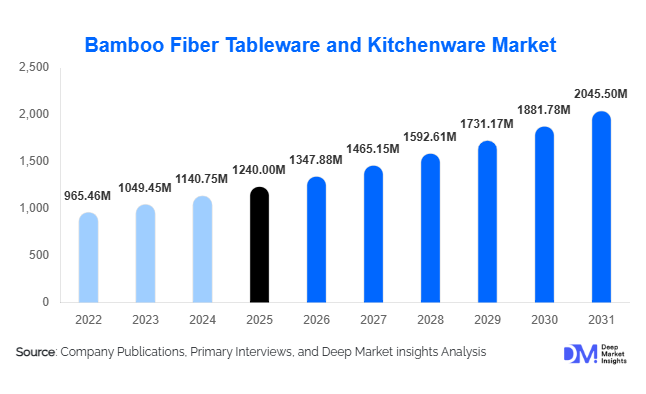

According to Deep Market Insights, the global bamboo fiber tableware and kitchenware market size was valued at USD 1,240 million in 2025 and is projected to grow from USD 1,347.88 million in 2026 to reach USD 2,045.50 million by 2031, expanding at a CAGR of 8.7% during the forecast period (2026–2031). Market growth is primarily driven by rising global restrictions on single-use plastics, increasing consumer preference for biodegradable and reusable alternatives, and expanding adoption of sustainable products across household and HoReCa (Hotels, Restaurants, Cafés) sectors.

Key Market Insights

- Plastic substitution policies across Europe, North America, and Asia are accelerating the transition toward compostable and bamboo-based tableware solutions.

- Mid-range sustainable lifestyle products dominate demand, balancing affordability with eco-certification and durability.

- Asia-Pacific leads global production, supported by abundant bamboo cultivation and export-oriented manufacturing infrastructure.

- Household residential applications account for over 60% of demand, driven by eco-conscious urban consumers.

- Online retail channels are growing at double-digit rates, reshaping distribution and brand visibility.

- Technological improvements in bio-resin blending and compression molding are enhancing durability, dishwasher resistance, and product aesthetics.

What are the latest trends in the bamboo fiber tableware and kitchenware market?

Shift Toward Premium Reusable Eco-Tableware

The market is transitioning from disposable bamboo products toward premium reusable formats. Consumers are increasingly demanding dishwasher-safe, BPA-free certified products with enhanced durability. Manufacturers are integrating plant-based bio-resins such as PLA to improve product lifespan while maintaining compostability. Designer finishes, matte textures, and minimalist Scandinavian-inspired aesthetics are expanding bamboo tableware’s presence in urban households. This premiumization trend is especially strong in Europe, Japan, Australia, and metropolitan North America, where consumers are willing to pay 15–30% more for sustainable homeware products.

Expansion of Sustainable HoReCa Procurement

Hotels, cafés, and institutional catering providers are embedding sustainability metrics into procurement decisions. Large hospitality chains are shifting to bamboo-based serving trays, bowls, and cutlery to align with ESG reporting requirements. Event catering and outdoor dining segments are increasingly adopting bamboo fiber alternatives to comply with local plastic bans. Bulk purchasing contracts are expanding, particularly in Germany, the United States, the UAE, and Australia. Institutional buyers are prioritizing certified compostable products that meet food-contact regulations, driving innovation in material testing and compliance standards.

What are the key drivers in the bamboo fiber tableware and kitchenware market?

Government Bans on Single-Use Plastics

Regulatory action remains the strongest market driver. The European Union’s Single-Use Plastics Directive, India’s nationwide plastic ban, and multiple U.S. state-level restrictions have accelerated substitution demand. These policies are compelling retailers and institutional buyers to replace plastic plates, bowls, and cutlery with biodegradable alternatives such as bamboo fiber. Compliance requirements are encouraging long-term supply contracts, strengthening revenue visibility for manufacturers.

Rising Eco-Conscious Consumer Behavior

Millennials and Gen Z consumers are prioritizing environmentally responsible purchasing. Over 60% of urban households in developed economies report willingness to pay a sustainability premium for kitchenware products. Social media influence, sustainability labeling, and eco-certification are reinforcing purchasing decisions. Bamboo fiber’s renewable sourcing and lower carbon footprint compared to petroleum-based plastics position it favorably among environmentally conscious consumers.

What are the restraints for the global market?

Raw Material Price Volatility

Bamboo pulp and bio-resin costs fluctuate due to climate variability, export controls, and global commodity price shifts. This volatility affects production costs and compresses manufacturer margins, particularly for small and mid-sized players. Rising freight and energy costs further amplify pricing pressure.

Regulatory Scrutiny on Composite Materials

Some blended bamboo products have faced scrutiny regarding food-contact safety, especially in European markets. Stricter testing standards and certification requirements increase compliance costs and may restrict certain formulations. Manufacturers must invest in quality control and third-party certifications to maintain market access.

What are the key opportunities in the bamboo fiber tableware and kitchenware industry?

Export-Led Manufacturing Expansion

China, Vietnam, and India are expanding bamboo processing infrastructure to serve export markets in Europe and North America. Automation in compression molding and resin integration is improving economies of scale. Export-driven demand offers significant growth opportunities, especially as Western retailers seek diversified, sustainable sourcing options.

Institutional and Corporate Catering Adoption

Corporate campuses, universities, and event organizers are increasingly transitioning to compostable tableware solutions. Large-scale procurement contracts present stable revenue streams for suppliers. Sustainability-linked procurement mandates in public institutions create additional long-term opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1240 Million |

| Market Size in 2026 | USD 1347.88 Million |

| Market Size in 2031 | USD 2045.50 Million |

| CAGR | 8.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Tableware continues to dominate the global bamboo fiber tableware and kitchenware market, accounting for approximately 54% of total revenue in 2025. The leadership of this segment is primarily driven by accelerated replacement of single-use plastic and melamine-based plates, bowls, and cutlery across both household and food service environments. Regulatory bans on plastic tableware in Europe, India, and multiple U.S. states have directly benefited bamboo-based dining products, making tableware the first point of substitution. Plates and bowls represent the largest sub-segment within tableware, supported by high purchase frequency, bundling in retail formats, and strong visibility in supermarkets and online marketplaces.

The dominance of tableware is also reinforced by consumer perception; dining products are highly visible lifestyle items, allowing consumers to express sustainability choices more prominently. Meanwhile, kitchenware products such as cutting boards, spatulas, mixing bowls, and storage containers are witnessing steady growth as eco-conscious households expand bamboo adoption beyond dining. On-the-go and compostable event tableware formats are gaining traction in catering, outdoor events, and quick-service restaurants, particularly in regions with strict plastic usage regulations. However, these segments remain smaller compared to reusable residential tableware, which continues to anchor global revenue.

Material Composition Insights

Bamboo fiber blended with plant-based bio-resins holds nearly 46% market share in 2025, making it the leading material category. The primary growth driver for this segment is enhanced product durability and improved mechanical strength, allowing dishwasher-safe and heat-resistant performance that pure bamboo fiber products sometimes lack. The integration of PLA and other biodegradable binders enhances lifecycle performance, making these products more suitable for mid-range and premium markets. This durability factor has significantly improved consumer confidence, especially in Europe and North America, where performance standards are stringent.

Pure bamboo molded products maintain strong appeal in eco-sensitive markets due to their minimal processing and high renewable content. However, they face limitations in high-temperature and repeated wash applications. Composite blends combining bamboo with plant starch or bagasse are gaining moderate traction, particularly in disposable and event-based applications where cost-efficiency and compostability are prioritized. Regulatory scrutiny in the EU regarding food-contact compliance is also encouraging manufacturers to invest in safer resin technologies, further accelerating innovation within the blended materials segment.

Distribution Channel Insights

Offline retail channels account for approximately 57% of global sales, maintaining leadership due to strong consumer preference for physically evaluating home and kitchen products prior to purchase. Supermarkets, hypermarkets, and home improvement chains remain dominant, particularly in Europe and North America, where shelf visibility and sustainability labeling influence purchase decisions. Retail chains are also expanding private-label bamboo collections to capitalize on growing demand.

However, online retail is the fastest-growing channel, expanding at over 12% CAGR. Direct-to-consumer (D2C) eco-brands, marketplace platforms, and sustainability-focused e-commerce stores are reshaping purchasing behavior. Digital channels enable detailed storytelling around sustainability credentials, certifications, and carbon footprint, which are key decision factors for younger consumers. Subscription-based models and bulk purchasing portals for institutional buyers are also emerging within the online ecosystem, increasing overall channel diversification.

End-Use Insights

Household residential applications represent nearly 62% of global demand in 2025, making it the largest end-use segment. Growth is driven by rising disposable incomes, urban sustainability trends, and growing awareness regarding plastic pollution. Residential demand is particularly strong in Germany, the United States, Japan, and Australia, where eco-friendly home upgrades are becoming mainstream lifestyle choices.

The HoReCa segment is the fastest-growing end-use category, expanding at close to 10% CAGR. Hotels, cafés, and quick-service restaurants are increasingly aligning procurement strategies with ESG commitments and plastic reduction policies. Institutional catering, corporate dining facilities, educational campuses, and event organizers are also adopting bamboo fiber tableware to meet sustainability benchmarks. Export-driven demand from Europe and North America significantly supports Asia-Pacific production hubs, strengthening cross-border supply chains and volume growth.

Explore more data points, trends and opportunities Download Free Sample Report

Bamboo Fiber Tableware and Kitchenware Market Segmentations

By Product Type

- Tableware

- Kitchenware

- On-the-Go & Compostable Event Tableware

By Material Composition

- 100% Bamboo Fiber Molded Products

- Bamboo Fiber with Bio-Resins

- Bamboo Composite

By Distribution Channel

- Online Retail

- Supermarkets & Hypermarkets

- Specialty Eco & Home Stores

- Home Improvement & Retail Chains

- B2B & Institutional Sales

By End Use

- Household Residential

- HoReCa (Hotels, Restaurants, Cafés)

- Corporate & Institutional Catering

- Events & Outdoor Catering

Regional Insights

Asia-Pacific

Asia-Pacific holds approximately 38% of the global market share in 2025, making it the largest regional market. The region’s leadership is driven by its dual role as both the largest production base and a rapidly expanding consumer market. China dominates manufacturing due to abundant bamboo resources, established pulp processing infrastructure, and cost-effective labor. Export-driven production to Europe and North America remains a major growth driver.

India is the fastest-growing country in the region, with an estimated CAGR of around 12%, supported by nationwide plastic ban enforcement, government-backed bamboo cultivation programs, and initiatives promoting domestic manufacturing. Japan and Australia lead premium adoption trends, driven by high environmental awareness, strong retail penetration of sustainable homeware, and demand for aesthetically refined products. Rapid urbanization and middle-class expansion across Southeast Asia are further contributing to regional momentum.

Europe

Europe accounts for approximately 27% of global demand, supported by stringent environmental regulations and strong consumer awareness regarding sustainability. The European Union’s Single-Use Plastics Directive continues to serve as a primary regional growth driver. Germany alone contributes roughly 6% of global consumption, benefiting from advanced recycling systems, eco-labeling culture, and high household spending on sustainable goods.

France, the UK, Italy, and Spain are also significant contributors, driven by the hospitality sector's transitions toward compostable alternatives. Strict food-contact regulations have pushed innovation in bio-resin formulations, further strengthening the region’s role as a premium consumption hub. The combination of regulatory enforcement, institutional procurement mandates, and sustainability-conscious consumers ensures steady long-term growth.

North America

North America captures about 23% market share, with the United States contributing nearly 19% of global demand. Regional growth is primarily driven by state-level plastic restrictions, corporate ESG commitments, and strong adoption within institutional catering and food service sectors. Major retail chains are expanding sustainable private-label offerings, increasing product visibility and affordability.

Canada supports steady growth through environmental policy alignment and rising consumer awareness. The region also benefits from robust e-commerce penetration, allowing D2C bamboo brands to scale rapidly. Premiumization trends and growing demand for reusable, dishwasher-safe products are further reinforcing market expansion.

Latin America

Brazil and Mexico lead regional adoption, accounting for nearly 6% combined global share. Growth drivers include gradual regulatory evolution, urban sustainability awareness, and expansion of modern retail channels. While adoption remains moderate compared to Europe and North America, increasing environmental advocacy and hospitality sector modernization are expected to support steady long-term demand.

Middle East & Africa

The Middle East & Africa region holds approximately 6% of the global share, with the UAE and Saudi Arabia leading demand. Growth is largely driven by premium hospitality expansion, luxury hotel chains, and sustainability initiatives aligned with national vision programs. Large-scale events, tourism-driven catering demand, and high per-capita disposable income in Gulf countries support the adoption of bamboo-based serving ware.

In Africa, adoption remains nascent but growing, supported by urban retail development and increasing environmental awareness. Government diversification strategies focused on tourism and hospitality infrastructure are expected to indirectly boost demand for sustainable tableware solutions.

Key Players in the Bamboo Fiber Tableware and Kitchenware Market

- Bambu Home

- Ekobo

- Zuperzozial

- Bamboo Studio

- Guangxi Longsheng Bamboo

- Anji Zhengyuan Bamboo

- Bambaw

- Chuk

- Bamboo Village Company

- Vegware

- Natural Tableware

- Pappco Greenware

- EcoSouLife

- Bamboozy

- Biobu