Bamboo Fabric Market Size

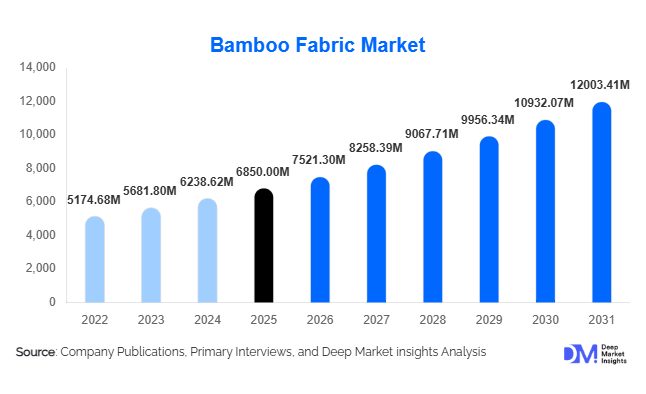

According to Deep Market Insights, the global bamboo fabric market size was valued at USD 6,850 million in 2025 and is projected to grow from USD 7,521.30 million in 2026 to reach USD 12,003.41 million by 2031, expanding at a CAGR of 9.8% during the forecast period (2026–2031). The bamboo fabric market growth is primarily driven by rising demand for sustainable textiles, increasing adoption in apparel and home furnishing applications, and advancements in eco-friendly fiber processing technologies.

Key Market Insights

- Bamboo fabric demand is rapidly increasing due to sustainability concerns, as consumers shift toward biodegradable and eco-friendly textile alternatives.

- Apparel remains the dominant application segment, driven by growing demand for breathable, antibacterial, and moisture-wicking fabrics.

- Asia-Pacific dominates production, led by China and India, due to abundant raw material availability and strong textile manufacturing infrastructure.

- Healthcare and hygiene applications are the fastest-growing segments, supported by the antimicrobial properties of bamboo fibers.

- Technological advancements in bamboo lyocell processing are enabling closed-loop production systems, improving environmental sustainability.

- Growing export demand from North America and Europe is driving production expansion in Asia-based manufacturing hubs.

What are the latest trends in the bamboo fabric market?

Shift Toward Sustainable and Circular Textiles

The bamboo fabric market is witnessing a strong shift toward circular and sustainable textile ecosystems. Manufacturers are increasingly adopting eco-friendly production techniques such as closed-loop processing to reduce environmental impact. Certifications related to sustainability and ethical sourcing are becoming critical for market competitiveness. Brands are incorporating bamboo-based fabrics into their product portfolios to meet consumer expectations for environmentally responsible fashion. This trend is particularly prominent in premium apparel and home textiles, where sustainability is a key differentiator.

Rising Adoption in Activewear and Performance Textiles

Bamboo fabric is gaining traction in activewear due to its superior moisture-wicking, breathability, and odor-resistant properties. The global shift toward athleisure and comfort-focused fashion is driving demand for bamboo-based textiles in sportswear and innerwear. Innovations in blending bamboo with synthetic fibers such as spandex are further enhancing performance characteristics, making it suitable for high-performance applications. This trend is expanding the scope of bamboo fabric beyond traditional uses into high-growth segments.

What are the key drivers in the bamboo fabric market?

Growing Demand for Eco-Friendly Fabrics

Increasing awareness of environmental issues such as water pollution and carbon emissions is driving the adoption of sustainable fabrics. Bamboo requires significantly less water and pesticides compared to cotton, making it an attractive alternative. Consumers and brands alike are prioritizing eco-friendly materials, positioning bamboo fabric as a preferred choice in the textile industry.

Expansion of the Global Apparel Industry

The rapid growth of the global apparel and fashion industry is a key driver for bamboo fabric demand. With increasing consumer preference for comfortable and functional clothing, bamboo fabric is being widely used in innerwear, casual wear, and baby clothing. The rise of fast fashion and athleisure trends is further accelerating market growth.

What are the restraints for the global market?

High Processing Costs for Sustainable Production

Eco-friendly processing methods, such as mechanical and closed-loop systems, require significant capital investment, making them less accessible for small manufacturers. This cost barrier limits the widespread adoption of truly sustainable bamboo fabric variants and impacts overall market scalability.

Lack of Standardization and Mislabeling

The market faces challenges related to inconsistent labeling practices, where chemically processed bamboo viscose is marketed as eco-friendly. This creates consumer skepticism and regulatory scrutiny, potentially hindering market growth unless transparency and certification standards improve.

What are the key opportunities in the bamboo fabric industry?

Expansion into Healthcare and Hygiene Applications

The antibacterial and hypoallergenic properties of bamboo fabric present significant opportunities in healthcare and hygiene applications. Increasing investments in healthcare infrastructure and rising hygiene awareness are driving demand for bamboo-based medical textiles, including hospital linens and surgical fabrics.

Growth in Emerging Markets

Emerging economies in Asia, Latin America, and Africa offer substantial growth opportunities due to rising disposable incomes and increasing awareness of sustainable products. Government initiatives promoting domestic textile manufacturing and exports are further supporting market expansion in these regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6850 Million |

| Market Size in 2026 | USD 7521.30 Million |

| Market Size in 2031 | USD 12003.41 Million |

| CAGR | 9.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Bamboo viscose continues to dominate the global bamboo fabric market, accounting for approximately 62% of the total share in 2025. Its leadership is primarily driven by cost efficiency, scalability, and established manufacturing infrastructure, particularly in Asia-Pacific. The chemical processing method used for viscose allows mass production at competitive prices, making it the preferred choice for large apparel manufacturers. Additionally, its soft texture and versatility across applications such as clothing, home textiles, and hygiene products further strengthen its dominance.

Bamboo lyocell is emerging as the fastest-growing product segment, supported by increasing demand for sustainable and closed-loop production systems. Unlike viscose, lyocell processing significantly reduces chemical waste and water usage, aligning with global environmental regulations and brand sustainability goals. Premium apparel brands are increasingly adopting bamboo lyocell, positioning it as a high-value segment with strong margin potential. Bamboo modal and bamboo linen cater to niche and premium segments, particularly in luxury textiles and specialty applications. Bamboo linen, produced through mechanical processing, is gaining attention among eco-conscious consumers despite its higher cost, while modal blends are preferred for enhanced softness and durability in high-end apparel.

Application Insights

The apparel segment leads the bamboo fabric market with nearly 48% share in 2025, driven by rising global demand for sustainable fashion, athleisure, and comfort-based clothing. Bamboo fabric’s natural properties, such as breathability, moisture-wicking, and antibacterial characteristics, make it highly suitable for innerwear, sportswear, and baby clothing. The increasing shift of global fashion brands toward eco-friendly materials is further reinforcing the segment’s leadership. Home textiles represent a significant and stable segment, valued at over USD 1,800 million, with strong demand in bedding, towels, and upholstery products. Growth in this segment is supported by increasing consumer preference for soft, hypoallergenic, and durable fabrics, particularly in premium household products.

Healthcare and industrial applications are witnessing accelerated growth due to bamboo fabric’s antimicrobial, biodegradable, and skin-friendly properties. In healthcare, applications such as surgical gowns, bandages, and hospital linens are expanding rapidly, while industrial uses include filtration fabrics and eco-friendly packaging materials. These segments are expected to gain higher market share over the forecast period due to increasing regulatory emphasis on hygiene and sustainability.

Distribution Channel Insights

Direct B2B sales dominate the bamboo fabric market, accounting for approximately 60% share, as manufacturers primarily supply raw and processed fabrics directly to apparel brands, textile manufacturers, and industrial buyers. This dominance is driven by the bulk procurement nature of the textile industry, long-term supplier relationships, and cost advantages associated with large-volume transactions.

Online retail is emerging as a high-growth distribution channel, particularly for finished bamboo-based products such as apparel, home textiles, and personal care items. The rapid expansion of e-commerce platforms, coupled with increasing consumer preference for convenience and transparency, is driving this shift. Digital platforms also allow brands to communicate sustainability credentials effectively, influencing purchasing decisions among environmentally conscious consumers. Specialty stores and sustainable fashion outlets are also gaining traction, particularly in developed markets, as consumers increasingly seek curated, eco-friendly product offerings.

End-Use Industry Insights

The fashion and apparel industry accounts for approximately 50% of the bamboo fabric market, driven by the global shift toward sustainable and ethical fashion practices. Increasing consumer awareness, coupled with brand commitments to reduce environmental impact, is significantly boosting demand in this segment. The integration of bamboo fabric into mainstream and premium apparel collections is further accelerating growth.

The healthcare industry is the fastest-growing end-use segment, with a projected CAGR exceeding 11%, driven by rising demand for antimicrobial and hypoallergenic textiles. Increasing healthcare infrastructure investments and stricter hygiene standards are key factors supporting this growth. The home furnishing industry remains a stable and high-volume segment, benefiting from consistent demand for bedding and household textiles. Meanwhile, the sports and activewear industry is emerging as a high-growth segment, driven by increasing demand for performance fabrics that offer comfort, durability, and odor resistance. New applications in baby care, hygiene products, and eco-friendly packaging are also expanding the scope of bamboo fabric across industries.

Explore more data points, trends and opportunities Download Free Sample Report

Bamboo Fabric Market Segmentations

By Product Type

- Bamboo Viscose

- Bamboo Lyocell

- Bamboo Modal

- Bamboo Linen

By Application

- Apparel

- Home Textiles

- Medical & Healthcare Textiles

- Industrial Textiles

- Personal Care & Hygiene Products

By Distribution Channel

- Direct B2B Sales

- Online Retail

- Specialty Textile Stores

- Mass Retail/Department Stores

By End-Use Industry

- Fashion & Apparel Industry

- Home Furnishing Industry

- Healthcare Industry

- Hospitality Industry

- Baby Care & Hygiene Industry

- Sports & Activewear Industry

Regional Insights

Asia-Pacific

Asia-Pacific leads the global bamboo fabric market with approximately 46% share in 2025, driven by its strong position as both a production and export hub. China dominates the region due to abundant bamboo resources, low production costs, and well-established textile infrastructure. India is emerging as a high-growth market, supported by government initiatives promoting domestic textile manufacturing and exports, as well as increasing adoption of sustainable fabrics in the local apparel industry. Southeast Asian countries such as Vietnam and Indonesia are also expanding production capacities, driven by foreign investments and export-oriented manufacturing strategies. The region’s growth is further fueled by rising domestic consumption, favorable government policies, and increasing global demand for sustainable textiles.

North America

North America holds around 22% share of the global market, with the United States leading demand. Regional growth is driven by high consumer awareness of sustainability, strong demand for eco-friendly products, and increasing adoption of ethical fashion. The presence of established retail networks and growing e-commerce penetration further supports market expansion. Additionally, increasing demand for premium home textiles and performance apparel is boosting bamboo fabric adoption. Regulatory focus on sustainable sourcing and environmentally friendly materials is also encouraging brands to integrate bamboo-based textiles into their product lines.

Europe

Europe accounts for nearly 20% share of the bamboo fabric market, driven by stringent environmental regulations and strong consumer preference for sustainable products. Countries such as Germany, the UK, France, and Italy are leading demand due to their advanced fashion industries and high adoption of eco-friendly materials. The European Union’s policies on reducing textile waste and promoting circular economy practices are key growth drivers. Additionally, increasing demand for certified organic and biodegradable fabrics in apparel and home textiles is accelerating market expansion across the region.

Latin America

Latin America is experiencing moderate growth, led by Brazil and Mexico. The region’s growth is driven by expanding retail sectors, rising middle-class income levels, and increasing awareness of sustainable textiles. Although the market is still developing, the growing demand for eco-friendly apparel and home textiles is creating new opportunities. Import dependency on Asian manufacturers remains high, but local production capabilities are gradually improving.

Middle East & Africa

The Middle East & Africa region is gradually emerging as a potential market for bamboo fabric, driven by growth in the hospitality, tourism, and luxury retail sectors. Countries such as the UAE and Saudi Arabia are witnessing increased demand for premium and sustainable textiles, particularly in high-end hotels and residential projects. In Africa, rising investments in textile manufacturing and increasing awareness of eco-friendly products are supporting market growth. Additionally, infrastructure development and government initiatives aimed at diversifying economies are contributing to the gradual expansion of the bamboo fabric market in this region.

Key Players in the Bamboo Fabric Market

- Lenzing AG

- China Bambro Textile Co., Ltd.*

- Fujian Green Pine Co., Ltd.

- Tenbro Bamboo Textile Co., Ltd.

- Shanghai Tenbro Bamboo Textile Co.

- Hebei Jigao Chemical Fiber Co., Ltd.

- CFF GmbH & Co. KG

- Chengdu Grace Fiber Co., Ltd.

- Zhejiang Yixin Textile Co., Ltd.

- Qingdao Fab Mill Co., Ltd.

- Bamboo Textile Group

- EcoPlanet Bamboo Group

- Boody Pty Ltd.

- Cariloha Inc.

- Bambu Batu LLC