Baker’s Yeast Market Size

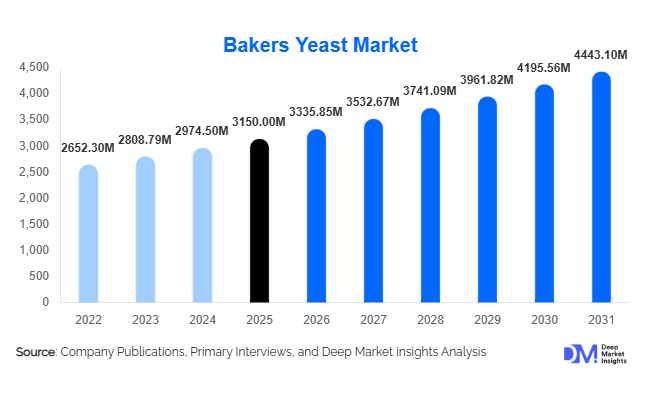

According to Deep Market Insights, the global baker’s yeast market size was valued at USD 3,150 million in 2025 and is projected to grow from USD 3,335.85 million in 2026 to reach USD 4,443.10 million by 2031, expanding at a CAGR of 5.9% during the forecast period (2026–2031). The baker’s yeast market growth is primarily driven by rising global consumption of bread and bakery products, increasing industrialization of bakeries, growing demand from quick-service restaurants (QSRs), and the shift toward natural fermentation and clean-label baking ingredients.

Key Market Insights

- Dry yeast dominates the global market due to its longer shelf life, ease of transportation, and suitability for industrial-scale baking.

- Industrial and commercial bakeries account for the largest share of yeast consumption, supported by automation and standardized production processes.

- Europe leads global demand, driven by high per-capita bread consumption in countries such as Germany, France, and Italy.

- Asia-Pacific is the fastest-growing region, fueled by urbanization, westernization of diets, and the rapid expansion of packaged bread markets in China and India.

- Clean-label and specialty yeast variants, including organic and osmotolerant yeast, are gaining strong traction among premium and artisanal bakers.

- Technological advancements in fermentation are improving yeast efficiency, dough stability, and flavor consistency across applications.

What are the latest trends in the baker’s yeast market?

Rising Adoption of Specialty and Clean-Label Yeast

Bakery manufacturers are increasingly shifting toward specialty yeast products that support clean-label formulations and enhanced functionality. Organic yeast, non-GMO yeast, and osmotolerant yeast designed for sugar-rich and frozen dough applications are witnessing strong demand. These products help bakers reduce reliance on chemical additives while improving dough performance, flavor development, and fermentation consistency. Premium bakery brands and artisanal bakeries are particularly driving this trend, with specialty yeast products commanding higher margins and reinforcing differentiation in competitive markets.

Technological Innovation in Yeast Fermentation

Advancements in biotechnology and fermentation control systems are reshaping yeast production and application. Manufacturers are developing application-specific yeast strains tailored for industrial bread, pizza dough, and frozen bakery products. Automation, AI-enabled fermentation monitoring, and improved drying technologies are enhancing yield efficiency, shelf life, and product consistency. These innovations are enabling large-scale bakeries to optimize production costs while maintaining uniform quality across geographies.

What are the key drivers in the baker’s yeast market?

Growing Global Consumption of Bakery Products

Bread and baked goods remain staple foods across developed and emerging economies. Rising urban populations, busy lifestyles, and demand for convenient packaged foods continue to drive consumption of industrial bread, buns, rolls, and pizza bases. This sustained growth directly translates into stable, volume-driven demand for baker’s yeast across regions.

Expansion of QSRs and Foodservice Chains

The rapid expansion of QSRs, pizza chains, and café-style bakeries is significantly boosting demand for instant and performance-stable yeast. These operators require consistent fermentation outcomes across standardized recipes, favoring commercially produced dry yeast solutions. The growth of global foodservice brands in Asia-Pacific, Latin America, and the Middle East is a major catalyst for yeast market expansion.

What are the restraints for the global market?

Raw Material Price Volatility

Baker’s yeast production relies heavily on molasses and sugar derivatives, which are subject to agricultural price fluctuations. Volatility in these raw materials can impact production costs and compress profit margins, particularly for manufacturers operating in price-sensitive markets.

Logistics and Shelf-Life Constraints for Fresh Yeast

Fresh yeast requires cold-chain logistics and has a limited shelf life, increasing transportation and storage costs. These constraints limit its adoption in remote and emerging markets, where infrastructure gaps remain a challenge.

What are the key opportunities in the baker’s yeast industry?

Rapid Growth in Asia-Pacific and Emerging Markets

Asia-Pacific represents the most significant growth opportunity, driven by expanding middle-class populations, increasing consumption of western-style bakery products, and strong investment in food processing infrastructure. Localized yeast solutions tailored to regional flour quality and climate conditions offer strong potential for differentiation and market penetration.

Premiumization through Specialty Yeast

The growing focus on premium, functional, and health-oriented bakery products presents opportunities for manufacturers to expand specialty yeast portfolios. Yeast products that enhance flavor, texture, and nutritional profiles can unlock higher-value segments and improve profitability.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3150 Million |

| Market Size in 2026 | USD 3335.85 Million |

| Market Size in 2031 | USD 4443.10 Million |

| CAGR | 5.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Dry yeast accounts for approximately 58% of the global baker’s yeast market in 2025, making it the dominant product type across both developed and emerging regions. The leadership of dry yeast is primarily driven by its extended shelf life, superior storage stability, ease of transportation, and compatibility with automated industrial baking processes. These attributes make dry yeast the preferred choice for large-scale commercial bakeries, frozen dough manufacturers, and quick-service restaurant (QSR) chains that require consistent fermentation performance across high-volume production runs.

In addition, the growing penetration of packaged bread and frozen bakery products has reinforced demand for instant and active dry yeast, as these formats reduce cold-chain dependency and minimize wastage. Fresh yeast continues to maintain strong relevance within artisanal and traditional bakeries, particularly in Europe, where bakers favor fresh yeast for its rapid fermentation and flavor development in handcrafted bread. However, its limited shelf life and cold storage requirements restrict broader adoption.

Application Insights

Bread remains the largest application segment in the baker’s yeast market, accounting for nearly 46% of total global demand in 2025. The segment’s dominance is supported by bread’s role as a staple food across regions, combined with the large-scale production of packaged and industrial bread varieties. Continuous demand from daily consumption patterns ensures stable volume growth for yeast manufacturers.

Growth in frozen dough, par-baked products, and ready-to-eat bakery items is reshaping yeast demand across applications. These formats require yeast strains with enhanced freeze-thaw stability and controlled fermentation behavior, increasing the adoption of advanced dry and specialty yeast products. Foodservice operators and retail bakeries are increasingly relying on these applications to improve operational efficiency and product consistency.

Distribution Channel Insights

Direct B2B supply dominates the baker’s yeast market, accounting for approximately 64% of global distribution in 2025. This channel is preferred by industrial and commercial bakeries due to the need for long-term supply agreements, consistent product quality, technical support, and customized yeast solutions. Direct sourcing also enables manufacturers to optimize pricing and logistics for high-volume customers.

Food ingredient distributors play a vital role in servicing small and mid-sized bakeries, particularly in fragmented and emerging markets where direct manufacturer access is limited. These distributors provide flexible order sizes, localized distribution networks, and value-added services such as formulation support. Retail and online channels support household and artisanal demand, benefiting from renewed interest in home baking and premium bread-making kits. E-commerce platforms are gradually expanding their reach, particularly for instant dry yeast and specialty yeast products targeted at small-scale and hobbyist bakers.

End-Use Insights

Industrial and commercial bakeries account for approximately 61% of total baker’s yeast consumption in 2025, making them the largest end-use segment globally. This dominance is driven by the rapid industrialization of bakery production, increasing automation, and growing demand for packaged bread, buns, and frozen bakery products. Large bakeries prioritize yeast products that deliver consistent fermentation performance, scalability, and cost efficiency.

Artisanal bakeries represent a steadily growing segment, supported by premiumization trends, consumer preference for handcrafted bread, and demand for clean-label and traditional baking methods. While volumes are lower than in industrial bakeries, artisanal producers often use higher-value fresh and specialty yeast products. The foodservice segment benefits from the global expansion of QSRs, cafés, and casual dining chains, particularly in pizza and sandwich categories. Household consumption, although smaller in share, continues to grow modestly, supported by e-commerce access and increased experimentation with baking at home.

Explore more data points, trends and opportunities Download Free Sample Report

Bakers Yeast Market Segmentations

By Product Type

- Dry Yeast

- Fresh Yeast

- Liquid Yeast

- Specialty Yeast

By Application

- Bread

- Pizza & Flatbreads

- Pastries, Cakes, Buns & Rolls

- Cookies & Biscuits

- Frozen Dough & Par-Baked Products

By End-Use

- Industrial / Commercial Bakeries

- Artisanal & Craft Bakeries

- Foodservice (QSRs, Cafés, Restaurants)

- Household / Retail

By Distribution Channel

- Direct B2B Supply

- Food Ingredient Distributors

- Retail & Online Channels

Regional Insights

Europe

Europe leads the global baker’s yeast market with an estimated 34% share in 2025. Demand is driven by high per-capita bread consumption, deeply rooted baking traditions, and a strong presence of both industrial and artisanal bakeries. Germany, France, Italy, and the U.K. are the primary demand centers, supported by established bakery infrastructure and consistent consumption of fresh and packaged bread. Additionally, Europe’s focus on clean-label, organic, and specialty bakery products is accelerating the adoption of premium yeast variants, reinforcing regional market leadership.

Asia-Pacific

Asia-Pacific holds approximately 29% market share and is the fastest-growing region, expanding at over 7% CAGR. Growth is driven by rapid urbanization, rising disposable incomes, and increasing adoption of Western-style bakery products in China, India, and Southeast Asia. Expansion of industrial bakeries, growth of QSR chains, and rising consumption of packaged bread and pizza are key regional growth drivers. Government investments in food processing infrastructure further support long-term demand for baker’s yeast.

North America

North America accounts for around 21% of global demand, supported by a mature industrial baking sector, widespread consumption of packaged bread, and strong frozen dough production. The U.S. leads regional demand due to large-scale bakery operations and foodservice penetration, while Canada contributes steady growth. Innovation in frozen and par-baked products, along with demand for consistent fermentation performance, continues to drive yeast consumption.

Latin America

Latin America represents roughly 9% of the global baker’s yeast market, with Brazil and Mexico as the primary contributors. Growth is driven by expanding urban populations, increasing consumption of packaged bakery products, and the modernization of bakery manufacturing facilities. Rising middle-class demand for affordable bread and buns supports stable yeast volumes across the region.

Middle East & Africa

The Middle East & Africa region holds about 7% market share, supported by growing packaged bread consumption, population growth, and increasing investments in bakery production, particularly in the GCC countries and South Africa. Dependence on imported bakery ingredients and rising demand for shelf-stable dry yeast are key drivers, while expansion of QSRs and modern retail formats is further boosting regional yeast demand.