Baby Electronic Toy Market Size

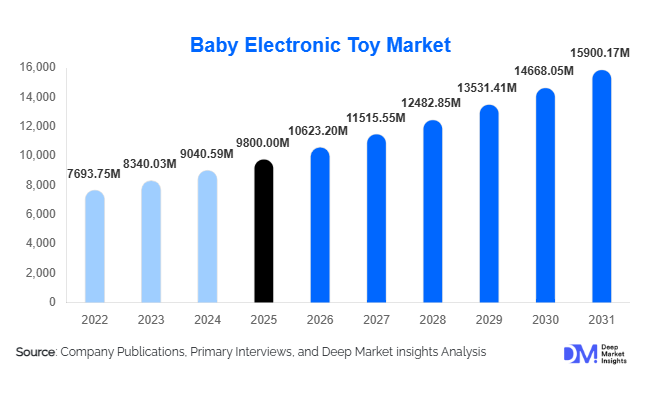

According to Deep Market Insights, the global baby electronic toy market size was valued at USD 9,800 million in 2025 and is projected to grow from USD 10,623.20 million in 2026 to reach USD 15,900.17 million by 2031, expanding at a CAGR of 8.4% during the forecast period (2026–2031). The market growth is primarily driven by rising parental awareness of early childhood development, increasing adoption of interactive learning tools, and the integration of smart technologies such as AI and IoT into infant toys. Growing disposable incomes, particularly in emerging economies, and the rapid expansion of e-commerce platforms are further accelerating demand for technologically advanced baby toys.

Key Market Insights

- Interactive learning toys dominate the market, accounting for nearly 34% of total revenue due to increasing focus on early cognitive development.

- Mid-range priced products (USD 20–50) lead adoption, capturing over 40% share as they balance affordability and advanced features.

- North America remains the largest regional market, contributing approximately 32% of global demand.

- Asia-Pacific is the fastest-growing region, driven by rising middle-class income and high birth rates in China and India.

- Offline retail channels still dominate, but online platforms are rapidly expanding due to convenience and product variety.

- Technological innovation, including AI-enabled and app-connected toys, is transforming product offerings and driving premiumization.

What are the latest trends in the baby electronic toy market?

Smart and AI-Integrated Toys Gaining Popularity

One of the most prominent trends in the baby electronic toy market is the increasing integration of artificial intelligence and smart technologies. Manufacturers are developing toys that can respond to a baby’s actions, adapt learning content, and provide personalized developmental support. These toys often connect to mobile applications, allowing parents to track progress and engage more actively in their child’s learning journey. Voice recognition, motion sensors, and adaptive learning algorithms are becoming standard features in premium product categories. This trend is particularly strong in developed markets where consumers are willing to pay higher prices for technologically advanced and educationally beneficial products.

Growing Demand for Eco-Friendly and Safe Materials

Parents are increasingly prioritizing sustainability and safety when purchasing baby products. As a result, manufacturers are focusing on non-toxic materials, eco-friendly plastics, and energy-efficient electronic components. Regulatory compliance and certifications are becoming key differentiators in the market. Brands that emphasize sustainability are gaining a competitive edge, particularly in Europe and North America. Additionally, there is a growing trend toward rechargeable batteries and reduced electronic waste, aligning with broader environmental goals and consumer preferences for responsible consumption.

What are the key drivers in the baby electronic toy market?

Rising Focus on Early Childhood Development

Increasing awareness among parents regarding the importance of early cognitive and sensory development is a major driver for the market. Electronic toys designed to enhance motor skills, language development, and problem-solving abilities are gaining widespread adoption. Educational institutions and pediatric experts are also endorsing interactive toys as effective tools for early learning, further boosting demand.

Technological Advancements in Toy Manufacturing

Rapid advancements in electronics and digital technologies have significantly enhanced the functionality of baby toys. Features such as touch sensors, sound recognition, and connectivity with smart devices are improving user engagement. These innovations not only enhance the play experience but also allow manufacturers to introduce premium products with higher profit margins, thereby contributing to overall market growth.

What are the restraints for the global market?

Stringent Safety Regulations

The baby electronic toy market is subject to strict safety standards related to materials, electronic components, and product design. Compliance with these regulations increases production costs and can delay product launches. Smaller manufacturers may face challenges in meeting these standards, limiting their ability to compete effectively in the global market.

Price Sensitivity in Emerging Markets

Despite growing demand, affordability remains a key concern in developing regions. Many consumers prefer low-cost alternatives, which restricts the penetration of advanced electronic toys. Companies must balance innovation with cost efficiency to cater to price-sensitive segments while maintaining profitability.

What are the key opportunities in the baby electronic toy industry?

Expansion in Emerging Markets

Emerging economies such as India, China, and Brazil present significant growth opportunities due to rising disposable incomes, urbanization, and increasing awareness of early childhood education. Government initiatives promoting domestic manufacturing are also encouraging local production and reducing dependency on imports. Companies that establish strong distribution networks in these regions can tap into a rapidly expanding consumer base.

Integration with Health and Wellness Features

The convergence of baby toys with health monitoring and wellness features is creating new growth avenues. Products that incorporate sleep tracking, soothing mechanisms, and sensory therapy are gaining popularity among parents. Collaboration with healthcare professionals and early childhood experts can further enhance product credibility and expand market reach.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9800 Million |

| Market Size in 2026 | USD 10623.20 Million |

| Market Size in 2031 | USD 15900.17 Million |

| CAGR | 8.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Interactive learning toys represent the largest segment in the baby electronic toy market, accounting for approximately 34% of the total market share in 2025. The dominance of this segment is primarily driven by the growing emphasis on early childhood cognitive development and the increasing preference among parents for toys that combine entertainment with structured learning outcomes. These toys integrate features such as voice interaction, adaptive learning, and sensory stimulation, making them highly effective in developing language, memory, and problem-solving skills at an early age. The rising influence of pediatric recommendations and early education frameworks has further strengthened demand for these products globally.

Musical and sound toys continue to hold a significant share, supported by their role in enhancing auditory development and sensory engagement, particularly among infants aged 0–12 months. Motion and activity toys are gaining traction due to their ability to support physical growth, coordination, and motor skills development, especially in the 6–24 months age group. Additionally, STEM-based toys for toddlers are emerging as a high-growth category, reflecting a broader shift toward early exposure to logical thinking, creativity, and foundational technical skills. This segment is expected to expand rapidly as parents increasingly invest in future-oriented learning tools.

Application Insights

Household usage dominates the baby electronic toy market, contributing over 85% of total demand in 2025. This dominance is largely driven by increasing parental spending on premium and technologically advanced toys designed to support at-home learning and engagement. The growing trend of nuclear families, coupled with higher disposable incomes, has led to a greater focus on providing high-quality developmental tools within the home environment. Additionally, the influence of digital parenting communities and product recommendations has accelerated the adoption of innovative toys among households.

Institutional applications, including daycare centers, preschools, and early learning facilities, are emerging as a fast-growing segment. This growth is fueled by the increasing global enrollment in early childhood education programs and the integration of interactive learning tools into structured curricula. Institutions are increasingly adopting electronic toys to enhance engagement, improve learning outcomes, and support group-based activities. This segment is expected to grow at a higher pace compared to household usage, supported by rising investments in early education infrastructure worldwide.

Distribution Channel Insights

Offline retail channels, including specialty toy stores, supermarkets, and baby product outlets, account for approximately 58% of total sales in 2025. The continued dominance of offline channels is driven by consumer preference for physically evaluating product quality, safety, and usability before purchase, particularly important for baby products. Retail stores also provide opportunities for demonstrations and personalized recommendations, which enhance consumer confidence.

However, online retail is the fastest-growing distribution channel, driven by increasing internet penetration, smartphone usage, and the convenience of home delivery. E-commerce platforms offer a wide range of products, competitive pricing, and access to customer reviews, making them highly attractive to modern consumers. Additionally, direct-to-consumer (D2C) strategies adopted by brands are enabling them to build stronger relationships with customers and expand their reach into previously untapped markets. The shift toward omnichannel retailing is expected to further accelerate market growth.

End-User Age Group Insights

The 12–24 months age group holds the largest market share at approximately 29% in 2025, driven by the critical developmental milestones achieved during this stage. Babies in this age group are highly responsive to interactive and sensory stimuli, making them ideal users of electronic toys that promote exploration, learning, and motor skill development. Products targeting this segment often include multifunctional features, such as lights, sounds, and motion sensors, which enhance engagement and developmental outcomes.

The 6–12 months segment also demonstrates strong demand, particularly for sensory and auditory toys that aid in early-stage development. Meanwhile, the 2–3 year age group is witnessing rapid growth, supported by increasing adoption of advanced electronic and STEM-based toys that introduce basic problem-solving and logical thinking concepts. This shift reflects a broader trend toward structured early learning and school readiness.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Electronic Toy Market Segmentations

By Product Type

- Interactive Learning Toys

- Musical & Sound Toys

- Motion & Activity Toys

- Remote-Control & Sensor-Based Toys

- Wearable & Soothing Electronic Devices

- STEM-Based Baby Toys

By Application

- Household Use

- Daycare Centers

- Early Learning & Preschool Institutions

By Distribution Channel

- Online Retail

- Specialty Toy Stores

- Supermarkets & Hypermarkets

- Baby Product Stores

- Direct-to-Consumer (D2C) Channels

By Age Group

- 0–6 Months

- 6–12 Months

- 12–24 Months

- 2–3 Years

By Technology Integration

- Basic Electronic Toys

- AI-Enabled Toys

- App-Connected Smart Toys

- IoT-Enabled Toys

Regional Insights

North America

North America leads the global baby electronic toy market, accounting for approximately 32% of the total market share in 2025. The United States is the dominant contributor, supported by high consumer spending power, strong demand for premium and technologically advanced toys, and widespread adoption of smart and AI-enabled products. The region’s growth is further driven by a well-established retail infrastructure, high awareness of early childhood education, and stringent safety standards that encourage the adoption of high-quality products. Canada complements regional growth with steady demand, driven by increasing focus on educational toys and strong regulatory frameworks that ensure product safety and quality.

Asia-Pacific

Asia-Pacific accounts for around 29% of the global market and is the fastest-growing region, with a CAGR exceeding 9–10%. China dominates both production and consumption due to its large manufacturing base and expanding middle-class population. India is emerging as a key growth market, driven by high birth rates, rising disposable incomes, and rapid urbanization. Growth in this region is also supported by expanding e-commerce penetration, increasing awareness of early childhood development, and government initiatives promoting domestic manufacturing. The shift toward modern parenting practices and growing demand for affordable yet feature-rich products are further accelerating market expansion.

Europe

Europe holds approximately 24% of the global market share, with major contributions from Germany, the United Kingdom, and France. Regional growth is driven by strong regulatory standards, high consumer awareness of child development, and increasing preference for eco-friendly and sustainable products. European consumers are particularly inclined toward toys that meet stringent safety certifications and environmental standards. Additionally, the region benefits from a well-developed retail network and increasing adoption of technologically advanced toys. The growing trend of sustainability and ethical consumption is expected to further drive demand in this market.

Latin America

Latin America contributes around 7% of global demand, with Brazil and Mexico as the leading markets. Growth in this region is supported by improving economic conditions, rising urbanization, and increasing awareness of the importance of early childhood education. The expansion of organized retail and e-commerce platforms is also enhancing product accessibility. However, price sensitivity remains a key challenge, influencing purchasing decisions and limiting the penetration of premium products. Despite this, gradual economic stability and rising middle-class populations are expected to support steady market growth.

Middle East & Africa

The Middle East & Africa region accounts for approximately 8% of the global market. Key markets such as the UAE and South Africa are driving growth due to increasing urbanization, expanding retail infrastructure, and rising disposable incomes. The region is witnessing a shift toward modern parenting practices, with greater emphasis on early childhood development and educational tools. Additionally, the growing presence of international brands and the expansion of online retail channels are improving product availability. Government initiatives to diversify economies and invest in retail and consumer sectors are further supporting market growth in this region.