B2B Hygienic Paper Market Size

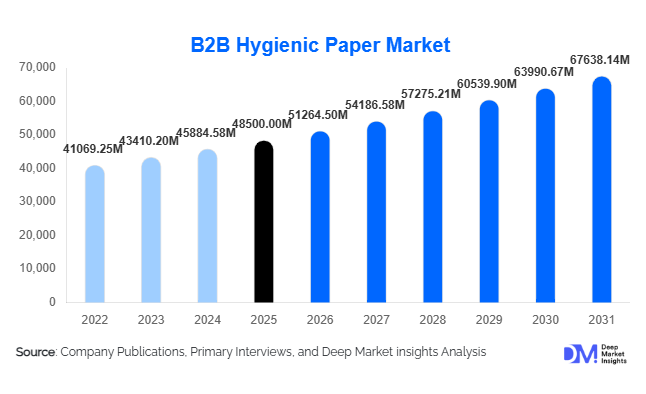

According to Deep Market Insights, the global B2B hygienic paper market size was valued at USD 48,500 million in 2025 and is projected to grow from USD 51,264.50 million in 2026 to reach USD 67,638.14 million by 2031, expanding at a CAGR of 5.7% during the forecast period (2026–2031). The market growth is primarily driven by the institutionalization of hygiene standards across industries, the expansion of commercial infrastructure, and the rising demand from the healthcare and hospitality sectors. Increasing adoption of sustainable and recycled hygienic paper products, along with the integration of automated dispensing systems, is further transforming the market from a commodity-driven space into a value-added ecosystem.

Key Market Insights

- Institutional hygiene standards have permanently increased consumption across healthcare, hospitality, and corporate sectors post-pandemic.

- Asia-Pacific dominates the global market, driven by rapid urbanization and infrastructure development in China and India.

- Sustainability trends are reshaping procurement decisions, with rising demand for recycled and alternative fiber-based products.

- Direct institutional contracts account for a major share, supported by long-term agreements with large enterprises.

- Jumbo roll formats are widely adopted in high-traffic facilities due to cost efficiency and operational convenience.

- Technology integration through smart dispensers is enhancing efficiency and enabling subscription-based supply models.

What are the latest trends in the B2B hygienic paper market?

Shift Toward Sustainable and Alternative Fiber Products

The market is witnessing a strong shift toward sustainable hygienic paper solutions, driven by corporate ESG goals and regulatory pressures. Manufacturers are increasingly investing in recycled fiber production as well as alternative raw materials such as bamboo, bagasse, and wheat straw. These materials reduce dependency on virgin pulp and lower environmental impact. Large institutional buyers, particularly in Europe and North America, are prioritizing eco-certified products, creating a premium segment within the market. Companies are also focusing on reducing water and energy consumption during production, further aligning with sustainability mandates.

Adoption of Smart Dispensing and Automation

Technological advancements are reshaping the B2B hygienic paper market through the adoption of IoT-enabled dispensers and automated hygiene systems. These systems monitor real-time usage, optimize replenishment cycles, and reduce wastage. Facility management companies are increasingly adopting such solutions to improve operational efficiency and reduce costs. Integration with digital procurement platforms is also enabling predictive supply chain management, ensuring uninterrupted availability in high-demand environments such as airports, hospitals, and commercial complexes.

What are the key drivers in the B2B hygienic paper market?

Expansion of Commercial Infrastructure

Rapid urbanization and the expansion of commercial infrastructure, such as office complexes, shopping malls, airports, and public sanitation facilities, are significantly driving demand. Emerging economies, particularly in the Asia-Pacific region, are witnessing large-scale infrastructure investments, resulting in increased consumption of hygienic paper products across multiple sectors.

Growth in Healthcare and Hygiene Awareness

The healthcare sector continues to be a major growth driver, supported by rising investments in hospital infrastructure and stricter hygiene protocols. Increased awareness regarding infection control and sanitation has led to higher consumption of hygienic paper products in hospitals, clinics, and laboratories. This trend has extended to other industries, reinforcing long-term demand.

What are the restraints for the global market?

Volatility in Raw Material Prices

Fluctuations in wood pulp prices remain a significant challenge for manufacturers. As pulp constitutes a major portion of production costs, price volatility directly impacts profit margins and pricing strategies. This creates uncertainty for both manufacturers and institutional buyers.

Environmental Compliance Costs

Stringent environmental regulations and sustainability requirements are increasing operational costs for manufacturers. Investments in eco-friendly production processes, certifications, and waste management systems are essential but can be capital-intensive, particularly for smaller players.

What are the key opportunities in the B2B hygienic paper industry?

Emerging Market Expansion

Developing regions such as Southeast Asia, India, and parts of Africa present significant growth opportunities due to rising investments in public infrastructure and commercial spaces. Increasing urbanization and improving hygiene awareness are driving demand for hygienic paper products in these markets, offering long-term growth potential for manufacturers.

Integration with Smart Facility Management Systems

The growing adoption of smart buildings and automated facility management systems is creating opportunities for integrated hygienic solutions. Manufacturers can collaborate with technology providers to offer bundled solutions, including dispensers and consumables, enabling recurring revenue streams and stronger customer retention.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 48500 Million |

| Market Size in 2026 | USD 51264.50 Million |

| Market Size in 2031 | USD 67638.14 Million |

| CAGR | 5.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Toilet paper continues to dominate the B2B hygienic paper market, accounting for approximately 34% of the total market share in 2025. Its leadership is driven by its universal applicability across all institutional environments, including healthcare facilities, hospitality establishments, commercial offices, and public infrastructure. The recurring and non-substitutable nature of toilet paper makes it the most stable and high-volume product category in the market. Large-format and jumbo roll variants further strengthen its dominance by offering cost efficiency and reduced maintenance frequency in high-traffic facilities.

Paper towels and napkins collectively represent the second-largest product group, primarily driven by demand in hospitality, food service, and commercial kitchens. The expansion of quick-service restaurants, catering services, and cloud kitchens has significantly increased the consumption of folded and roll-based paper towels. Industrial wiping paper is gaining traction in manufacturing, automotive, and food processing industries, where stringent workplace hygiene and contamination control protocols require disposable wiping solutions. Meanwhile, premium facial tissues are witnessing increased adoption in corporate environments, premium hospitality, and healthcare settings, where comfort, softness, and quality are prioritized as part of enhanced customer and patient experience strategies.

Application (End-use Industry) Insights

The hospitality sector leads the B2B hygienic paper market, accounting for nearly 27% market share in 2025. Hotels, restaurants, resorts, and catering services are among the highest consumers of hygienic paper products due to continuous guest turnover and stringent cleanliness expectations. Growth in global tourism, expansion of hotel chains, and increasing service standards are driving sustained demand in this segment. The healthcare industry is the fastest-growing end-use segment, supported by rising hospital infrastructure investments, expansion of private healthcare networks, and stricter infection prevention protocols. Hospitals, clinics, and diagnostic laboratories require hygienic paper products for sanitation, patient care, and clinical procedures, resulting in higher per-bed consumption compared to other sectors.

Commercial offices and IT parks represent a stable demand segment, driven by corporate hygiene policies and increasing employee wellness initiatives. As organizations return to full-scale office operations post-pandemic, demand for restroom and pantry hygiene consumables is rising. Industrial and manufacturing facilities are also increasing the adoption of hygienic paper products, particularly in regulated sectors such as pharmaceuticals, food processing, and electronics, where contamination control and safety compliance are critical operational requirements.

Distribution Channel Insights

Direct institutional contracts account for approximately 38% of the global market, making them the leading distribution channel. Large enterprises, hospital networks, hotel chains, and government organizations prefer long-term procurement agreements to ensure consistent supply, price stability, and standardized product quality across multiple locations. These contracts also allow manufacturers to secure predictable revenue streams and optimize production planning.

Wholesale distributors continue to play a crucial role in servicing small and medium enterprises, educational institutions, and independent hospitality establishments that do not have the purchasing scale to negotiate direct contracts. Meanwhile, e-procurement platforms and digital B2B marketplaces are rapidly gaining traction as organizations increasingly shift toward centralized and automated procurement systems. Facility management companies are emerging as influential intermediaries, consolidating demand across multiple client sites and standardizing hygienic paper specifications to streamline operations and reduce costs.

Material Type Insights

Virgin pulp-based hygienic paper products hold around 46% market share in 2025, primarily due to their superior softness, strength, and absorbency. These characteristics make virgin pulp products particularly suitable for premium applications in healthcare, hospitality, and corporate environments where user comfort and product performance are critical. However, recycled fiber-based hygienic paper products are gaining strong momentum as organizations adopt sustainability-focused procurement policies. Recycled products offer lower environmental impact and are increasingly supported by government regulations and green building certifications. As a result, they are becoming the preferred choice for public infrastructure, educational institutions, and environmentally conscious corporations.

Alternative fiber-based products, including bamboo and bagasse, represent a niche but rapidly expanding segment. These products are attracting interest in regions facing wood pulp shortages or stringent deforestation regulations. Although currently limited by higher production costs and supply chain constraints, advancements in processing technology and growing environmental awareness are expected to support long-term growth in this segment.

Explore more data points, trends and opportunities Download Free Sample Report

B2B Hygienic Paper Market Segmentations

By Product Type

- Toilet Paper

- Paper Towels

- Napkins

- Facial Tissues

- Medical Wipes

- Industrial Wiping Paper

By End-use Industry

- Healthcare

- Hospitality

- Commercial Offices & IT Parks

- Industrial & Manufacturing

- Transportation Hubs

- Education Institutions

- Government & Public Infrastructure

By Distribution Channel

- Direct Institutional Contracts

- Facility Management Procurement Firms

- Wholesale Distributors

- E-Procurement Platforms

By Material Type

- Virgin Pulp

- Recycled Fiber

- Blended Fiber

- Alternative Fibers

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global B2B hygienic paper market with approximately 36% share in 2025, driven by rapid urbanization, expanding commercial infrastructure, and rising hygiene awareness. China leads the region with around 18% of global demand, supported by its large manufacturing base, extensive hospitality sector, and strong export-oriented production capabilities. Government investments in public sanitation and large-scale infrastructure projects have further strengthened demand.

India represents the fastest-growing market in the region, fueled by government-led sanitation initiatives, expansion of healthcare infrastructure, and growth in the organized retail and hospitality sectors. Programs aimed at improving public hygiene standards and urban infrastructure development are significantly increasing institutional consumption of hygienic paper products across transportation hubs, public facilities, and educational institutions.

North America

North America accounts for nearly 28% of the global market, led by the United States, which exhibits one of the highest per capita consumption levels of hygienic paper products globally. The region’s strong demand is driven by well-established hygiene standards, strict regulatory frameworks in healthcare and food service, and widespread adoption of advanced dispensing systems that encourage higher product usage.

The United States also benefits from a mature facility management industry and widespread corporate outsourcing of cleaning services, which standardizes procurement and increases consumption volumes. Canada contributes a stable demand supported by its strong healthcare infrastructure, commercial real estate sector, and emphasis on sustainable procurement practices.

Europe

Europe holds around 24% market share, with Germany, the United Kingdom, and France acting as key demand centers. The region’s market growth is strongly influenced by stringent environmental regulations, which are accelerating the transition toward recycled and eco-certified hygienic paper products. The presence of well-established hospitality and healthcare systems further supports steady demand. In Western Europe, high labor costs and strict workplace hygiene laws are encouraging the adoption of automated dispensing solutions, which in turn increases consumption efficiency and drives premium product demand. Eastern European countries are witnessing rising demand as commercial infrastructure expands and living standards improve.

Middle East & Africa

The Middle East is experiencing rapid growth in hygienic paper consumption, particularly in the United Arab Emirates and Saudi Arabia, where large-scale investments in tourism, hospitality, airports, and commercial real estate are driving institutional demand. Mega-events, international tourism campaigns, and luxury hotel development are increasing the consumption of premium hygienic paper products.

Africa represents an emerging long-term growth market, supported by gradual improvements in sanitation infrastructure, rising urbanization, and increasing awareness regarding hygiene practices. Countries such as South Africa, Nigeria, and Kenya are witnessing rising adoption of hygienic paper products across healthcare facilities, educational institutions, and urban commercial centers.

Latin America

Latin America, led by Brazil and Mexico, shows moderate but steady growth in the B2B hygienic paper market. Demand in the region is primarily driven by expanding hospitality industries, modernization of public infrastructure, and increasing investments in healthcare facilities. Brazil’s large urban population and strong food service industry contribute significantly to regional consumption.

Mexico benefits from its proximity to North American supply chains and the expansion of multinational hospitality and retail brands, which are introducing standardized hygiene practices and increasing demand for commercial tissue products. Economic recovery and urban infrastructure investments across the region are expected to support gradual market expansion in the coming years.

Key Players in the B2B Hygienic Paper Market

- Kimberly-Clark Corporation

- Essity AB

- Procter & Gamble

- Georgia-Pacific LLC

- Asia Pulp & Paper

- Suzano S.A.

- CMPC Tissue

- Metsä Tissue

- Sofidel Group

- WEPA Group

- Cascades Inc.

- Hengan International Group

- Vinda International Holdings

- Kruger Products

- Industrie Cartarie Tronchetti