Atomic Clocks Market Size

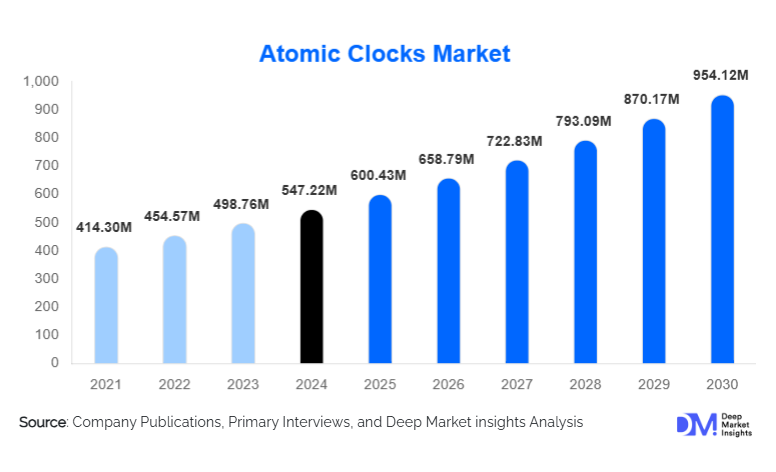

According to Deep Market Insights, the global atomic clocks market size was valued at USD 547.22 million in 2025 and is projected to grow from USD 600.43 million in 2026 to reach USD 954.12 million by 2031, expanding at a CAGR of 9.72% during the forecast period (2026–2031). The atomic clocks market growth is primarily driven by the rising deployment of satellite navigation systems, increasing demand for high-precision time synchronization in telecommunications and defense, and continuous technological advancements in miniaturized and optical atomic clocks.

Key Market Insights

- Cesium atomic clocks remain the dominant technology, serving as primary frequency standards for GNSS and national timekeeping laboratories.

- Aerospace and defense applications account for the largest revenue share, supported by sustained military modernization and space exploration programs.

- North America leads the global market, driven by strong defense spending, space agency investments, and private space companies.

- Asia-Pacific is the fastest-growing region, fueled by sovereign GNSS programs and rising investments in satellite manufacturing.

- Miniaturization trends, particularly chip-scale atomic clocks (CSACs), are expanding commercial adoption beyond traditional sectors.

- Optical atomic clocks are emerging as a high-value niche, supported by quantum research and next-generation space missions.

What are the latest trends in the atomic clocks market?

Miniaturization and Chip-Scale Atomic Clocks Adoption

The atomic clocks market is witnessing a strong shift toward miniaturization, led by the rapid development of chip-scale atomic clocks. These compact devices deliver high precision while consuming significantly less power and space, making them suitable for telecom base stations, industrial IoT, autonomous systems, and secure financial networks. As fabrication techniques mature and costs gradually decline, CSACs are transitioning from defense-led deployments to broader commercial applications. This trend is reshaping market accessibility and opening new revenue streams for manufacturers focused on scalable production.

Growing Role of Optical Atomic Clocks

Optical atomic clocks represent a transformative trend due to their exceptional accuracy, surpassing traditional microwave-based clocks. Although currently limited to research institutions and space agencies, increased funding for quantum technologies and deep-space navigation is accelerating their development. Optical clocks are increasingly tested for gravitational measurements, relativistic physics, and next-generation navigation systems, positioning them as a future cornerstone of ultra-high-precision timekeeping.

What are the key drivers in the atomic clocks market?

Expansion of Satellite Navigation and Space Programs

The rapid growth of global navigation satellite systems (GNSS) and satellite constellations is a primary driver of the atomic clocks market. Atomic clocks are critical for maintaining positional accuracy and synchronization in space-based systems. Government-backed GNSS modernization programs and the rise of private satellite operators are generating sustained demand for space-qualified atomic clocks, particularly cesium and hydrogen maser variants.

Rising Demand for Network Synchronization

Telecommunications networks, especially 5G and future 6G infrastructure, require ultra-precise time synchronization to manage latency, data throughput, and network reliability. Atomic clocks are increasingly deployed at network cores and critical nodes to ensure stable and secure operations. This driver is particularly strong in regions investing heavily in digital infrastructure and smart cities.

What are the restraints for the global market?

High Cost and Technical Complexity

Atomic clocks involve complex manufacturing processes, specialized materials, and rigorous calibration, resulting in high upfront costs. This limits adoption among cost-sensitive commercial sectors and restricts market participation to well-capitalized players. Maintenance and long qualification cycles further add to the total cost of ownership.

Lengthy Certification and Deployment Timelines

Applications in defense, aerospace, and space missions require extensive testing and certification, often spanning several years. These long development timelines can delay commercialization and slow revenue realization for manufacturers, acting as a restraint on rapid market expansion.

What are the key opportunities in the atomic clocks industry?

Sovereign Timing and GNSS Independence

Governments worldwide are investing in sovereign timing infrastructure to reduce reliance on foreign navigation systems. National timekeeping laboratories, terrestrial backup timing networks, and indigenous GNSS programs present long-term procurement opportunities for atomic clock manufacturers, particularly in the Asia-Pacific and the Middle East.

Integration with Quantum and Secure Communication Systems

The convergence of atomic clocks with quantum sensing, secure communications, and advanced defense systems presents a high-value opportunity. Atomic clocks play a critical role in quantum networks and encrypted communication systems, creating new demand from research institutions and defense agencies focused on next-generation security technologies.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 547.22 Million |

| Market Size in 2026 | USD 600.43 Million |

| Market Size in 2031 | USD 954.12 Million |

| CAGR | 9.72% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Clock Type Insights

Cesium atomic clocks dominate the market, accounting for approximately 38% of the 2025 market share due to their role as primary frequency standards. Rubidium atomic clocks follow, driven by widespread use in telecom and industrial applications. Hydrogen maser clocks hold a strong position in space and deep-space missions, while optical atomic clocks represent a rapidly emerging segment with strong long-term growth potential despite their currently limited commercial deployment.

Application Insights

Navigation and positioning applications lead the market, contributing nearly 34% of global revenue in 2025, supported by GNSS deployments and defense navigation systems. Telecommunications and network synchronization represent the fastest-growing application segment, while scientific research and metrology continue to drive demand for ultra-high-precision clocks. Financial trading, power grid synchronization, and deep-space exploration are emerging applications contributing incremental growth.

End-Use Industry Insights

Aerospace and defense remain the largest end-use industries, accounting for around 41% of total market revenue, driven by high-value contracts and long-term programs. Telecom operators are the fastest-growing end users due to 5G network rollouts. Government laboratories, space agencies, and research institutions continue to represent stable demand, while energy utilities and financial institutions are emerging as niche but high-growth end users.

Explore more data points, trends and opportunities Download Free Sample Report

Atomic Clocks Market Segmentations

By Clock Type

- Cesium Atomic Clocks

- Rubidium Atomic Clocks

- Hydrogen Maser Atomic Clocks

- Optical Atomic Clocks

By Accuracy & Stability Class

- Primary Frequency Standards

- Secondary Frequency Standards

- Compact Precision Atomic Clocks

- Ultra-High Precision Research Clocks

By Form Factor

- Laboratory-Based Atomic Clocks

- Rack-Mounted / Industrial Atomic Clocks

- Chip-Scale Atomic Clocks (CSAC)

- Space-Qualified Atomic Clocks

By Application

- Navigation & Positioning (GNSS, PNT)

- Telecommunications & Network Synchronization

- Defense & Aerospace Systems

- Scientific Research & Metrology

- Financial Trading & Time-Stamping

- Power Grid Synchronization

- Space Exploration & Deep-Space Missions

By End-Use Industry

- Aerospace & Defense

- Telecom Operators & Network Providers

- Government & National Laboratories

- Space Agencies & Satellite OEMs

- Financial Institutions

- Energy & Utilities

- Academic & Research Institutions

Regional Insights

North America

North America accounts for approximately 37% of the global atomic clocks market, led by the United States. Strong defense spending, extensive space programs, and the presence of leading manufacturers support regional dominance. Investments in resilient timing infrastructure and private space missions further reinforce demand.

Europe

Europe holds nearly 26% market share, driven by GNSS programs such as Galileo, strong research funding, and defense modernization. Countries including Germany, France, the U.K., and Switzerland represent major demand centers for both research-grade and commercial atomic clocks.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR exceeding 12%. China, Japan, and India are investing heavily in sovereign GNSS systems, satellite manufacturing, and defense infrastructure, driving rapid adoption of atomic clocks across space and telecom applications.

Latin America

Latin America represents a smaller but growing market, supported by expanding telecom networks and research collaborations. Brazil and Mexico are the primary contributors, with increasing imports of atomic clocks for academic and industrial use.

Middle East & Africa

The Middle East is emerging as a growth hub due to rising defense spending and satellite investments in countries such as the UAE and Saudi Arabia. Africa’s demand is primarily research- and telecom-driven, supported by international collaborations and infrastructure development.

Key Players in the Atomic Clocks Market

- Microchip Technology

- Safran Group

- Oscilloquartz (ADVA)

- Frequency Electronics Inc.

- AccuBeat Ltd.

- Stanford Research Systems

- Leonardo S.p.A.

- Thales Group

- Chengdu Spaceon Electronics

- Spectratime

- Muquans

- Jackson Labs Technologies

- IQD Frequency Products

- KVG Quartz Crystal Technology

- VREMYA-CH JSC