Artificial Turf Market Size

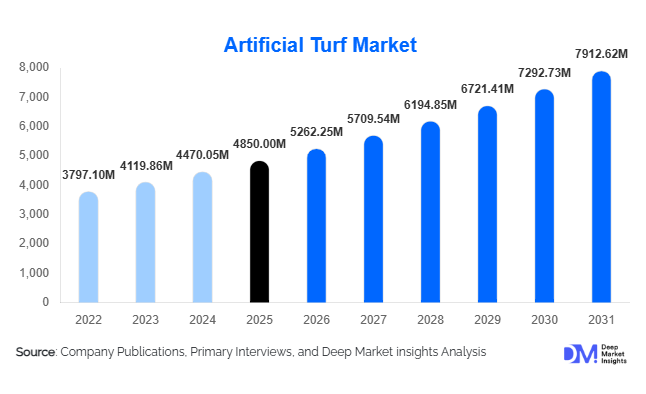

According to Deep Market Insights, the global artificial turf market size was valued at USD 4,850 million in 2025 and is projected to grow from USD 5,262.25 million in 2026 to reach USD 7,912.62 million by 2031, expanding at a CAGR of 8.5% during the forecast period (2026–2031). The artificial turf market growth is primarily driven by increasing water conservation needs, rising demand for low-maintenance landscaping solutions, and expanding investments in global sports infrastructure.

Key Market Insights

- Artificial turf adoption is accelerating due to water scarcity and sustainability concerns, especially in urban and arid regions.

- Sports infrastructure development continues to dominate demand, particularly for football, hockey, and multi-sport fields.

- North America leads the global market, supported by strong adoption in residential landscaping and sports facilities.

- Asia-Pacific is the fastest-growing region, driven by rapid urbanization and infrastructure investments.

- Eco-friendly infill materials and recyclable turf systems are gaining traction, addressing environmental concerns.

- Technological advancements, including heat-reduction coatings and enhanced durability fibers, are reshaping product innovation.

What are the latest trends in the artificial turf market?

Sustainable and Recyclable Turf Systems

Manufacturers are increasingly focusing on developing sustainable artificial turf solutions, including recyclable backing materials and organic infill options such as cork and coconut fibers. This shift is largely driven by regulatory pressure in Europe and growing environmental awareness among consumers. Companies are investing in circular economy models where old turf can be recycled into new installations, reducing landfill waste. Additionally, innovations in biodegradable components and reduced microplastic emissions are positioning sustainable turf as a premium segment within the market.

Technological Advancements in Turf Performance

Technological innovation is transforming artificial turf performance, with advancements in yarn engineering, shock absorption, and cooling technologies. Heat-reduction coatings are being introduced to address concerns about surface temperatures, particularly in hot climates. Enhanced drainage systems and antimicrobial properties are improving hygiene and usability across sports and residential applications. Smart turf systems integrated with sensors for performance monitoring are also emerging in professional sports environments, offering real-time data on field conditions and player impact.

What are the key drivers in the artificial turf market?

Growing Demand for Low-Maintenance Landscaping

The increasing preference for low-maintenance landscaping solutions is a major driver of artificial turf adoption. Unlike natural grass, artificial turf eliminates the need for watering, mowing, and fertilization, significantly reducing operational costs. This is particularly beneficial for commercial real estate, municipal parks, and residential developments where maintenance budgets are a key concern.

Expansion of Sports Infrastructure

Global investments in sports infrastructure are driving demand for artificial turf, especially in football, hockey, and multi-sport facilities. Artificial turf provides durability, consistent playing conditions, and the ability to withstand high usage intensity, making it a preferred choice for stadiums, schools, and training facilities worldwide.

Water Conservation Regulations

Increasing water scarcity and regulatory restrictions on irrigation are accelerating the adoption of artificial turf. Governments in regions such as North America and the Middle East are promoting water-efficient landscaping solutions, making artificial turf an attractive alternative to natural grass.

What are the restraints for the global market?

Environmental Concerns and Microplastic Issues

Artificial turf systems, particularly those using rubber infill, are facing scrutiny due to potential environmental impacts such as microplastic pollution. Regulatory challenges in Europe and other regions are pushing manufacturers to innovate and adopt eco-friendly materials.

High Initial Installation Costs

The upfront cost of artificial turf installation remains significantly higher than natural grass, which can limit adoption in price-sensitive markets. Although lifecycle costs are lower, the initial investment continues to be a barrier for some end users.

What are the key opportunities in the artificial turf industry?

Water Scarcity-Driven Adoption

Regions facing severe water shortages, including the Middle East, parts of the United States, and Australia, present significant growth opportunities. Government policies restricting water usage for landscaping are encouraging the adoption of artificial turf as a sustainable alternative.

Eco-Friendly Product Innovation

The development of organic infill materials and recyclable turf systems is creating new opportunities for manufacturers. Companies investing in sustainable technologies are gaining a competitive edge, particularly in environmentally regulated markets such as Europe.

Urban Infrastructure and Smart City Projects

Rapid urbanization and the rise of smart city initiatives are driving demand for artificial turf in public spaces, rooftops, and commercial developments. These projects emphasize low-maintenance and aesthetically appealing landscaping solutions, boosting market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4850 Million |

| Market Size in 2026 | USD 5262.25 Million |

| Market Size in 2031 | USD 7912.62 Million |

| CAGR | 8.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Polyethylene (PE) turf dominates the market with approximately 52% share in 2025, driven by its superior durability, softness, UV resistance, and close resemblance to natural grass. Its widespread adoption across both sports and landscaping applications makes it the preferred material globally. Polypropylene (PP) turf holds a smaller share due to its lower cost and suitability for decorative and low-traffic areas, while nylon turf is used in specialized high-performance applications requiring enhanced resilience and load-bearing capacity. Hybrid blends, combining PE with PP or nylon, are gaining traction as they offer improved strength, aesthetic appeal, and longevity. These blended systems are particularly popular in professional sports installations where performance consistency and durability are critical.

Application Insights

Sports fields remain the largest application segment, accounting for approximately 45% of the global market in 2025. This dominance is supported by continuous investments in sports infrastructure, including football stadiums, hockey fields, and multi-purpose athletic complexes. Artificial turf enables year-round usage and reduced maintenance downtime, making it highly attractive for high-traffic sports environments. Landscaping applications, including residential lawns, commercial complexes, and public parks, are the fastest-growing segment, driven by rapid urbanization and increasing demand for aesthetically pleasing, low-maintenance green spaces. Emerging applications such as rooftop gardens, airport landscaping, and event flooring are further expanding the scope of artificial turf usage globally.

Distribution Channel Insights

Direct sales dominate the artificial turf market, particularly for large-scale B2B projects such as sports stadiums, educational institutions, and municipal installations. Manufacturers often engage directly with contractors, architects, and government bodies to secure bulk orders and long-term contracts. Distributors and specialized contractors play a significant role in regional markets, offering installation expertise and localized service support. Meanwhile, online retail channels are gradually emerging, especially in the residential segment, where DIY installations are becoming more common. Digital platforms are increasingly influencing purchasing decisions by providing product comparisons, virtual visualization tools, and cost estimation features, enhancing customer engagement and accessibility.

End-Use Insights

The sports and athletics segment leads the market with approximately 47% share, driven by global investments in professional and amateur sports infrastructure. Artificial turf’s durability, consistent performance, and lower lifecycle costs make it a preferred choice for sports authorities and institutions. Residential applications are the fastest-growing segment, supported by increasing urban housing developments and rising consumer preference for water-efficient and low-maintenance landscaping solutions. Commercial real estate, including office complexes, shopping centers, and hospitality establishments, is also contributing significantly to market growth by incorporating artificial turf for aesthetic enhancement and cost savings. Government and municipal projects, particularly in urban beautification and public parks, further support demand expansion.

Explore more data points, trends and opportunities Download Free Sample Report

Artificial Turf Market Segmentations

By Product Type

- Polyethylene (PE) Turf

- Polypropylene (PP) Turf

- Nylon Turf

- Hybrid Blended Turf

By Infill Type

- Rubber-based Infill

- Sand-based Infill

- Organic/Bio-based Infill

- Non-infill Systems

By Application

- Sports Fields

- Residential Landscaping

- Commercial Landscaping

- Leisure & Recreational Areas

- Others (Airports, Road Medians, Events)

By Distribution Channel

- Direct Sales (B2B Projects)

- Distributors & Contractors

- Online Retail

By End-Use Industry

- Sports & Athletics

- Residential

- Commercial Real Estate

- Government & Municipal

- Hospitality & Tourism

Regional Insights

North America

North America accounts for approximately 32% of the global market, with the United States representing the largest contributor. Demand is driven by extensive adoption in sports infrastructure, including schools, colleges, and professional stadiums, as well as increasing use in residential landscaping. Water conservation regulations in states such as California and Arizona are accelerating the shift toward artificial turf. High disposable income levels and strong awareness of sustainable landscaping practices further support regional growth.

Europe

Europe holds around 28% market share, led by countries such as Germany, the United Kingdom, and the Netherlands. The region is characterized by stringent environmental regulations, which are encouraging the adoption of recyclable turf systems and organic infill materials. Demand is particularly strong in sports applications, including football and hockey, as well as in urban landscaping projects. European consumers are increasingly prioritizing eco-friendly solutions, driving innovation in sustainable artificial turf technologies.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR exceeding 10%, fueled by rapid urbanization, infrastructure development, and rising disposable incomes. China dominates both production and consumption, accounting for a significant share of global supply. India and Southeast Asian countries are emerging as high-growth markets due to increasing investments in sports facilities, smart city projects, and residential developments. The region’s expanding middle class and growing awareness of water conservation are further boosting demand.

Latin America

Latin America accounts for approximately 7% of the global market, with Brazil and Mexico leading adoption. Growth in the region is driven by investments in sports infrastructure, particularly football, as well as increasing urban landscaping initiatives. The adoption of artificial turf is gradually expanding into residential and commercial applications as awareness of its long-term cost benefits increases.

Middle East & Africa

The Middle East & Africa region contributes around 8–10% of the market, with strong demand in countries such as the United Arab Emirates and Saudi Arabia. Extreme climatic conditions and water scarcity make artificial turf an essential solution for landscaping and sports applications. Government initiatives promoting sustainable urban development and green infrastructure are further supporting market growth. In Africa, demand is primarily driven by sports infrastructure development and increasing urbanization in key economies.

Key Players in the Artificial Turf Market

- Tarkett Group

- Shaw Industries Group

- TenCate Grass

- FieldTurf

- CCGrass

- SIS Pitches

- Act Global

- GreenFields

- Domo Sports Grass

- SportGroup Holding

- Limonta Sport

- ForestGrass

- Nurteks

- Taishan Turf

- Condor Grass