Artificial Grass Market Size

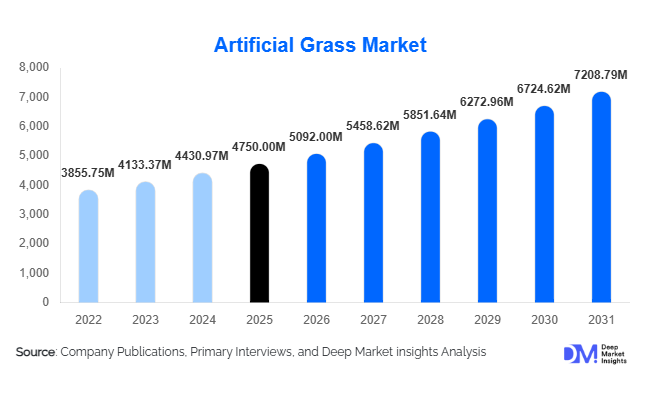

According to Deep Market Insights, the global artificial grass market size was valued at USD 4,750 million in 2025 and is projected to grow from USD 5,092.00 million in 2026 to reach USD 7,208.79 million by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). The artificial grass market growth is primarily driven by increasing investments in sports infrastructure, rising water conservation initiatives, and the growing preference for low-maintenance landscaping solutions across residential and commercial sectors.

Key Market Insights

- Sports turf applications account for nearly 58% of total demand, supported by football, rugby, hockey, and multi-sport field installations globally.

- Polyethylene (PE) dominates material consumption with over 52% share, due to its softness, durability, and natural grass-like aesthetics.

- North America leads the market with approximately 34% share in 2025, driven by sports modernization and drought-related landscaping policies.

- Asia-Pacific is the fastest-growing region, expanding at over 8.5% CAGR due to rising urbanization and sports infrastructure investments.

- Sustainability-focused turf systems, including recyclable backing and PFAS-free infill, are reshaping product development strategies.

- Direct B2B project sales dominate distribution channels, accounting for nearly 70% of installations globally.

What are the latest trends in the artificial grass market?

Sustainable and Recyclable Turf Systems

Environmental regulations in Europe and North America are accelerating the development of recyclable artificial turf systems. Manufacturers are increasingly adopting thermoplastic backings, bio-based infills, and closed-loop recycling programs to address concerns around microplastic shedding and landfill waste. The shift toward sustainable solutions is also driven by public procurement requirements and green building certifications such as LEED and BREEAM. Companies offering take-back programs and recyclable mono-material turf systems are gaining a competitive advantage, particularly in municipal and educational infrastructure projects.

Advanced Fiber Technology and Performance Enhancement

Technological innovation in fiber extrusion and yarn engineering is enhancing durability, UV stability, and shock absorption. Monofilament fibers, accounting for nearly 48% of market share, are gaining traction due to their improved resilience and realistic appearance. Hybrid turf systems combining synthetic grass with organic infill are also emerging, especially in professional sports fields seeking performance optimization. Additionally, smart underlayment systems with enhanced drainage and temperature control capabilities are being integrated to improve player safety and longevity.

What are the key drivers in the artificial grass market?

Water Conservation and Climate Adaptation

Water scarcity regulations across regions such as California, Australia, Spain, and the Middle East are encouraging the adoption of non-irrigated landscaping solutions. Artificial grass significantly reduces annual water consumption compared to natural turf, making it an attractive alternative in drought-prone areas. Municipal rebate programs and urban heat mitigation initiatives are further strengthening demand in residential and public landscaping.

Sports Infrastructure Modernization

Artificial turf allows up to 3,000 playing hours annually compared to 600–800 hours for natural grass. This durability advantage makes it a preferred choice for schools, sports academies, and professional clubs. Increasing investments in football and multi-sport facilities across Asia-Pacific and the Middle East are contributing substantially to market expansion.

What are the restraints for the global market?

Environmental and Microplastic Concerns

Regulatory scrutiny regarding crumb rubber infill and synthetic microplastics is creating compliance challenges. Proposed restrictions in parts of Europe may increase product development and certification costs, potentially impacting pricing structures.

High Initial Installation Costs

Artificial grass installation costs remain 2–4 times higher than natural sod, creating adoption barriers in price-sensitive markets. While lifecycle costs are lower, upfront capital expenditure remains a limiting factor for small-scale buyers.

What are the key opportunities in the artificial grass industry?

Emerging Market Infrastructure Development

Rapid urbanization in India, Southeast Asia, and parts of Africa is driving investments in public parks, sports academies, and recreational infrastructure. Government-backed programs and public-private partnerships offer long-term, recurring demand opportunities for manufacturers.

Urban Rooftop and Smart City Landscaping

Increasing vertical construction and rooftop landscaping projects in densely populated cities are expanding artificial grass applications beyond sports. Smart city initiatives emphasizing low-maintenance green spaces create new commercial and residential demand segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4750 Million |

| Market Size in 2026 | USD 5092 Million |

| Market Size in 2031 | USD 7208.79 Million |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Material Type Insights

Polyethylene (PE) dominates the global artificial grass market with approximately 52% revenue share in 2025, driven by its superior softness, flexibility, UV resistance, and realistic grass-like appearance. PE fibers are widely preferred for both sports turf and landscaping applications due to their ability to balance durability with player comfort and aesthetic appeal. Technological advancements in extrusion processes have further improved PE’s resilience and color stability, making it the primary material choice for high-performance football fields and premium residential lawns. Growing demand for FIFA-certified sports fields and high-end landscaping projects continues to reinforce PE’s leadership position.

Polypropylene (PP) serves primarily cost-sensitive applications and holds a strong position in decorative landscaping, balconies, exhibitions, and low-traffic installations. Its lower cost structure makes it attractive in price-sensitive emerging markets. However, PP’s relatively lower durability compared to PE limits its penetration in high-impact sports fields. Nylon (Polyamide), while more expensive, is preferred in high-durability and high-temperature environments due to its superior resilience and shape retention. It is commonly used in hockey pitches and multi-sport complexes requiring exceptional wear resistance. Hybrid blends (PE + PP or PE + Nylon) are gaining traction in professional sports installations, as they optimize performance characteristics such as shock absorption, durability, and recovery rate. Increasing innovation in fiber engineering and sustainability requirements are expected to drive gradual growth in hybrid systems.

Application Insights

Sports turf remains the largest application segment, accounting for nearly 58% of total global market share in 2025. The dominance of this segment is driven by rising investments in football stadiums, school athletic facilities, rugby fields, and multi-sport complexes. Artificial turf enables 3–5 times higher usage hours compared to natural grass, significantly improving return on infrastructure investment. Government-backed sports modernization programs, particularly in Asia-Pacific and the Middle East, continue to accelerate installations.

Landscaping applications represent approximately 34% of market demand and are among the fastest-growing segments. Increasing water scarcity regulations, urban residential development, and commercial real estate landscaping projects are major drivers. Artificial grass is increasingly adopted in residential lawns, hospitality properties, corporate campuses, and public parks to reduce irrigation costs and maintenance labor. Non-sport installations, including playgrounds, rooftop gardens, pet areas, and indoor décor applications, are expanding steadily. Urban vertical construction, child-safety standards in playgrounds, and pet-friendly residential communities are contributing to consistent growth in this segment.

Installation Type Insights

New installations account for approximately 65% of total demand in 2025, reflecting ongoing infrastructure development in emerging economies and modernization programs in developed regions. Expansion of sports academies, municipal recreational projects, and commercial landscaping developments are primary contributors to new installations.

Replacement and refurbishment projects represent the remaining 35% share and are gaining importance in mature markets such as North America and Western Europe. First-generation artificial turf systems installed between 2005 and 2015 are reaching end-of-life cycles, creating a recurring demand stream for upgraded, recyclable, and performance-enhanced systems. Sustainability-driven retrofits are also contributing to replacement growth.

Distribution Channel Insights

Direct B2B sales dominate the global market with nearly 70% share, particularly for large-scale sports infrastructure, municipal projects, and commercial landscaping contracts. These projects typically involve long procurement cycles, tender-based contracts, and technical compliance certifications, favoring established manufacturers with global execution capabilities.

Dealer and distributor networks serve regional contractors and mid-scale landscaping firms, especially in developing markets. Online retail and DIY channels are emerging within the residential segment, particularly in North America and Europe. E-commerce platforms offering modular turf systems and installation kits are expanding accessibility for small-scale consumers, though their revenue contribution remains comparatively smaller.

End-Use Industry Insights

Sports facilities, educational institutions, and municipal recreational centers remain the largest end-use segment, supported by global sports industry investments exceeding USD 600 billion annually. The push for year-round field utilization and reduced maintenance budgets is driving artificial turf adoption across schools and universities.

The commercial real estate and hospitality sector is among the fastest-growing end-use industries, expanding at nearly 8–9% CAGR. Hotels, resorts, shopping malls, and corporate campuses increasingly utilize artificial landscaping to enhance visual appeal while reducing water consumption and operational costs. Emerging end-use industries include pet care facilities, rooftop infrastructure in smart cities, indoor sports arenas, and event management spaces. Export-driven manufacturing hubs in China and Southeast Asia continue to supply North America and Europe, reinforcing international trade flows and supporting global capacity expansion.

Explore more data points, trends and opportunities Download Free Sample Report

Artificial Grass Market Segmentations

By Material Type

- Polyethylene (PE)

- Polypropylene (PP)

- Nylon (Polyamide)

- Hybrid Blends (PE + PP / PE + Nylon)

By Application

- Sports Turf

- Landscaping

- Playgrounds

- Rooftops & Balconies

- Pet Areas

- Indoor & Decorative Installations

By Installation Type

- New Installation

- Replacement & Refurbishment

By Distribution Channel

- Direct B2B / Project Sales

- Dealer & Distributor Network

- Online Retail / DIY Sales

By Backing Material

- Latex-Based Backing

- Polyurethane (PU) Backing

- Thermoplastic Backing Systems

Regional Insights

North America

North America accounts for approximately 34% of the global artificial grass market in 2025, with the United States contributing nearly 28% of global demand. The region’s dominance is driven by large-scale sports infrastructure upgrades, particularly in football, baseball, and multi-sport fields. Water conservation regulations in drought-prone states such as California, Arizona, and Texas are accelerating landscaping adoption. Rising labor costs for natural lawn maintenance and strong municipal funding for recreational facilities further strengthen regional demand. Replacement demand is also significant due to aging first-generation turf systems.

Europe

Europe holds approximately 27% market share, with strong demand from the UK, Germany, France, Spain, Italy, and the Netherlands. Growth drivers include regulatory pressure to reduce water usage, strict sustainability mandates, and strong participation in football and hockey. The European Union’s environmental regulations are accelerating innovation in recyclable turf systems and bio-based infills. Community sports programs and public infrastructure modernization are further sustaining regional growth. Western Europe leads in refurbishment demand, while Eastern Europe shows increasing new installation opportunities.

Asia-Pacific

Asia-Pacific represents nearly 24% of global demand and is the fastest-growing region, expanding at over 8.5% CAGR. China acts as both a major manufacturing hub and a rapidly growing domestic consumer market. Government investments in sports academies, Olympic training centers, and urban recreational parks are key growth drivers. India and Southeast Asia are witnessing rising installations in school-level sports infrastructure. Rapid urbanization, expanding middle-class housing projects, and growing awareness of water-efficient landscaping solutions are accelerating demand across the region.

Middle East & Africa

Holding about 9% share, the Middle East & Africa region benefits from climatic conditions that limit natural grass viability. High temperatures, water scarcity, and desert landscapes make artificial turf a practical alternative. Countries such as the UAE, Saudi Arabia, and Qatar are investing heavily in sports infrastructure, mega-events, and public recreational facilities. Vision-driven national development programs and tourism infrastructure expansion are supporting sustained artificial turf installations. In Africa, South Africa and Morocco are emerging markets driven by football infrastructure investments.

Latin America

Latin America accounts for approximately 6% of global demand, led by Brazil, Mexico, Argentina, and Chile. Football-centric infrastructure development remains the primary driver, with increasing adoption in community fields and private sports academies. Urban residential development and commercial real estate landscaping are gradually contributing to demand growth. Economic volatility may impact short-term investments, but long-term sports participation trends continue to provide steady expansion opportunities.

Key Players in the Artificial Grass Market

- TenCate Grass

- Shaw Sports Turf

- Tarkett Sports

- FieldTurf

- SIS Pitches

- Limonta Sport

- Polytan

- Act Global

- CCGrass

- CoCreation Grass

- Edel Grass

- Global Syn-Turf

- ForestGrass

- Nurteks

- Victoria PLC