Art Toy Market Size

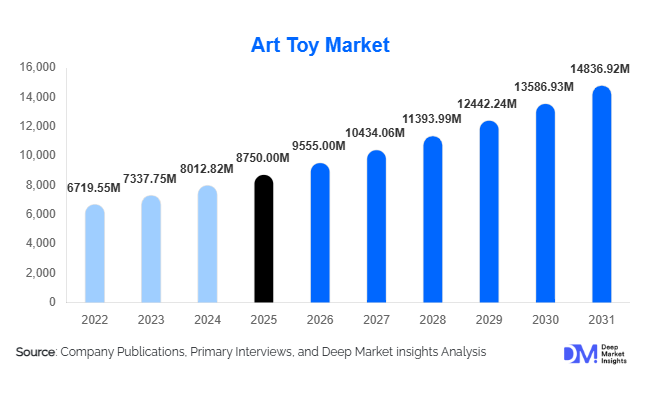

According to Deep Market Insights, the global art toy market size was valued at USD 8,750 million in 2025 and is projected to grow from USD 9,555.00 million in 2026 to reach USD 14,836.92 million by 2031, expanding at a CAGR of 9.2% during the forecast period (2026–2031). The art toy market growth is primarily driven by the increasing convergence of pop culture, designer art, and collectibles, alongside rising demand for limited-edition merchandise and licensed intellectual property (IP) collaborations. The emergence of digital ecosystems, including NFTs and phygital collectibles, is further accelerating market expansion by enhancing consumer engagement and creating new monetization channels.

Key Market Insights

- Licensed IP-based art toys dominate global demand, accounting for over half of market revenue due to strong fan engagement across entertainment and gaming ecosystems.

- Asia-Pacific leads the global market, driven by strong production capabilities and high consumer demand, particularly in China and Japan.

- Online marketplaces and direct-to-consumer channels are reshaping distribution, enabling global accessibility and drop-based sales models.

- Mid-tier collectibles (USD 51–200) represent the largest price segment, balancing affordability with exclusivity.

- Blind box and mystery box formats are gaining significant traction, particularly among younger consumers who seek surprise-driven purchases.

- Phygital integration, combining physical toys with digital assets, is emerging as a key differentiator in the market.

What are the latest trends in the art toy market?

Rise of Blind Box and Drop Culture

The blind box format has revolutionized purchasing behavior in the art toy market, creating excitement through uncertainty and collectability. Consumers are increasingly drawn to limited-edition drops, where scarcity drives urgency and resale value. This trend is particularly strong in the Asia-Pacific but is rapidly expanding into North America and Europe. The drop culture model, often executed through timed online releases, enhances brand loyalty and drives repeat purchases. Secondary markets have also flourished, where rare items can command multiples of their original price, reinforcing art toys as both collectibles and investment assets.

Integration of Digital and Physical Collectibles

The emergence of phygital collectibles is transforming the art toy ecosystem. Brands are increasingly pairing physical toys with NFTs or digital twins, offering enhanced ownership experiences such as exclusive digital content, virtual display options, and resale authentication. Blockchain technology is being adopted to ensure authenticity and traceability, addressing concerns around counterfeiting. This integration is particularly appealing to tech-savvy consumers and collectors who value both physical and digital ownership, expanding the overall addressable market.

What are the key drivers in the art toy market?

Expansion of Global Pop Culture Ecosystems

The rapid growth of anime, gaming, and streaming content has significantly boosted demand for licensed collectibles. Art toys serve as premium extensions of popular franchises, enabling fans to engage with their favorite characters beyond digital platforms. This has led to strong growth in licensed IP collaborations, which now dominate the market.

Growth of E-commerce and Direct Sales Channels

Digital platforms have democratized access to art toys, allowing independent artists and brands to reach global audiences without traditional retail constraints. Direct-to-consumer models enable better margin control, personalized marketing, and faster product launches, driving overall market expansion.

Increasing Investment Appeal of Collectibles

Art toys are increasingly viewed as alternative investment assets, particularly limited-edition releases. Collectors and investors are drawn to the potential for price appreciation, supported by active secondary markets and auction platforms. This trend is driving demand in the high-end and ultra-premium segments.

What are the restraints for the global market?

High Pricing and Limited Accessibility

Premium pricing remains a barrier to entry for many consumers, particularly in emerging markets. While demand exists, affordability constraints limit the widespread adoption of high-end and ultra-premium collectibles, especially.

Counterfeit Products and IP Challenges

The proliferation of counterfeit art toys poses a significant challenge to market growth. Weak enforcement of intellectual property rights in certain regions undermines brand value and erodes consumer trust, necessitating investments in authentication technologies.

What are the key opportunities in the art toy industry?

Expansion into Emerging Markets

Regions such as Southeast Asia, India, and Latin America present significant growth opportunities due to rising disposable incomes and increasing exposure to global pop culture. Localized product offerings and culturally relevant designs can help brands penetrate these underdeveloped markets.

Phygital and NFT-Backed Collectibles

The integration of blockchain technology and NFTs with physical art toys offers new revenue streams and enhanced consumer engagement. Companies investing in digital ecosystems can benefit from recurring revenue through digital upgrades, royalties, and resale tracking.

Brand Collaborations and Corporate Merchandising

Collaborations between artists, brands, and entertainment franchises are creating high-demand collectible products. Corporate merchandising is also emerging as a key growth area, with companies using art toys for brand promotion and customer engagement.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8750 Million |

| Market Size in 2026 | USD 9555 Million |

| Market Size in 2031 | USD 14836.92 Million |

| CAGR | 9.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Designer vinyl toys dominate the global art toy market, accounting for approximately 38% of total revenue in 2025. This leadership is primarily driven by their scalability in mass production, superior durability, and cost efficiency compared to other materials. Vinyl enables manufacturers to produce high-quality collectibles at relatively lower costs while maintaining design precision, making it the preferred medium for both independent artists and large-scale licensed collaborations. Additionally, vinyl toys are highly adaptable for customization, enabling brands to launch multiple variants and limited editions, which further fuels repeat purchases and collector engagement.

Resin art toys occupy the premium segment, catering to high-end collectors who prioritize craftsmanship, exclusivity, and artistic detailing. These products are typically produced in limited quantities, often handcrafted, resulting in higher price points and margins. Plush art toys are gaining traction among younger consumers and casual collectors due to their affordability, emotional appeal, and crossover with lifestyle merchandise. Meanwhile, blind box toys represent one of the fastest-growing sub-segments, driven by gamification, surprise elements, and strong appeal among Gen Z consumers. Custom and commissioned art toys, although niche, deliver high margins and are driven by personalized demand, artist branding, and one-of-a-kind creations that enhance their perceived investment value.

Application Insights

Licensed IP-based art toys represent the largest application segment, contributing over 52% of global market revenue in 2025. The dominance of this segment is driven by strong consumer affinity for globally recognized characters from movies, anime, gaming, and music. Established fan bases significantly reduce marketing costs and ensure immediate demand upon product launches. Furthermore, licensing agreements allow brands to scale production and expand into global markets rapidly, making this segment the primary revenue driver.

Original IP art toys are gaining momentum as collectors increasingly seek uniqueness, artistic authenticity, and exclusivity. Independent artists and boutique studios are leveraging social media platforms to build dedicated communities and drive direct-to-consumer sales. Collaborative releases between brands and artists are another high-growth area, combining mainstream appeal with creative differentiation. These collaborations often result in limited-edition drops that command premium pricing and generate strong resale value. Institutional applications, including galleries, museums, and exhibitions, are expanding steadily as art toys gain recognition as legitimate art forms, further bridging the gap between commercial collectibles and fine art.

Distribution Channel Insights

Online marketplaces lead the distribution landscape, accounting for approximately 41% of total market share in 2025. Their dominance is driven by global accessibility, ease of product discovery, and the growing popularity of drop-based sales models. Digital platforms enable brands to reach a wider audience, facilitate international transactions, and create hype-driven launches through limited-time releases. The integration of social media and e-commerce has further strengthened this channel by enabling real-time engagement and community building.

Direct-to-consumer (D2C) channels are the fastest-growing segment, as brands and independent artists increasingly prioritize control over pricing, branding, and customer relationships. D2C models also improve profit margins by eliminating intermediaries. Specialty retail stores continue to provide curated, experiential shopping environments, particularly for premium and high-end collectibles. Art galleries and exhibitions cater to institutional buyers and high-net-worth collectors, positioning art toys as artistic investments. Additionally, comic conventions and pop culture events remain critical for product launches, brand visibility, and direct consumer interaction, reinforcing community-driven demand.

Consumer Type Insights

Individual collectors dominate the art toy market, accounting for approximately 68% of total demand in 2025. This segment’s leadership is driven by strong emotional engagement, community participation, and the growing perception of art toys as investment assets. Collectors are increasingly influenced by limited editions, artist reputation, and resale value, which encourages repeat purchases and long-term brand loyalty.

Institutional buyers, including galleries, museums, and art investment funds, are contributing to the premiumization of the market. Their participation validates art toys as a legitimate art category and supports higher pricing benchmarks. Corporate buyers represent an emerging segment, using art toys for brand promotion, merchandising, and customer engagement initiatives. This segment is expected to grow steadily as companies leverage collectibles to strengthen brand identity and connect with younger audiences, thereby diversifying demand beyond traditional collectors.

Explore more data points, trends and opportunities Download Free Sample Report

Art Toy Market Segmentations

By Product Type

- Designer Vinyl Toys

- Resin Art Toys

- Plush Art Toys

- Blind Box / Mystery Toys

- Custom & Commissioned Art Toys

- Limited Edition Collectibles

By Application

- Licensed IP Collectibles

- Original Artist IP Collectibles

- Brand Collaborations & Co-Creations

- Institutional & Exhibition Use

By Distribution Channel

- Online Marketplaces

- Direct-to-Consumer (D2C)

- Specialty Retail Stores

- Art Galleries & Exhibitions

- Comic Cons & Pop Culture Events

By Consumer Type

- Individual Collectors

- Institutional Buyers

- Corporate Buyers

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global art toy market, accounting for approximately 46% of total revenue in 2025, making it the leading regional market. China alone contributes around 28% of global demand, driven by a well-established manufacturing ecosystem, strong domestic consumption, and the widespread popularity of blind box formats. The presence of large-scale players and efficient supply chains further strengthens the region’s dominance. Japan remains a mature and influential market, supported by its deep-rooted anime and manga culture, which continuously fuels demand for licensed collectibles.

Key growth drivers in the region include a large youth population, high digital engagement, and strong integration of art toys with pop culture and entertainment ecosystems. Southeast Asia, particularly Indonesia, Thailand, and Vietnam, is emerging as the fastest-growing sub-region, with growth rates exceeding 12% CAGR. This growth is driven by rising disposable incomes, increasing urbanization, and the rapid adoption of e-commerce platforms. Additionally, social media-driven collector communities are playing a crucial role in expanding market penetration across the region.

North America

North America holds approximately 27% of the global art toy market, with the United States accounting for nearly 24% share. The region is characterized by high disposable incomes, a mature collector base, and strong demand for premium and limited-edition collectibles. The presence of major entertainment franchises and licensing ecosystems significantly boosts demand for branded art toys.

Growth in North America is driven by the increasing popularity of pop culture conventions, a well-established resale market, and rising interest in collectibles as alternative investments. The region also benefits from advanced e-commerce infrastructure and strong adoption of direct-to-consumer sales models. Additionally, collaborations between global brands and local artists are expanding the market, particularly in the premium and high-end segments.

Europe

Europe accounts for approximately 16% of the global market, with key contributions from the United Kingdom, Germany, and France. The region is characterized by a strong appreciation for design, art, and craftsmanship, which aligns well with the artistic nature of art toys. European consumers tend to prioritize originality and sustainability, driving demand for independent artist creations and eco-friendly materials.

Key growth drivers include increasing participation in art exhibitions, rising interest in collectible art, and expanding e-commerce penetration. The region is also witnessing a shift toward sustainable production practices, with brands exploring biodegradable materials and ethical sourcing. Additionally, collaborations between European designers and global brands are enhancing product diversity and driving market expansion.

Latin America

Latin America represents an emerging market with growing potential, driven by increasing exposure to global pop culture and digital platforms. Brazil and Mexico are the primary contributors, supported by expanding middle-class populations and rising interest in collectibles among younger consumers. Growth in the region is fueled by social media influence, increasing availability of international products through e-commerce, and the gradual development of local artist communities. While the market is still in its early stages, improving economic conditions and growing cultural engagement are expected to drive steady demand over the forecast period.

Middle East & Africa

The Middle East and Africa collectively account for approximately 11% of the global market, with the UAE emerging as a key hub for premium art toy consumption. The region’s growth is primarily driven by high disposable incomes, strong luxury consumption patterns, and expanding retail infrastructure. In the Middle East, increasing interest in pop culture, gaming, and entertainment is boosting demand for licensed collectibles. The presence of high-end retail outlets and international exhibitions further supports market growth. In Africa, the market is at a nascent stage but shows potential due to a growing youth population and increasing digital connectivity. Overall, rising urbanization, cultural diversification, and investments in retail and entertainment infrastructure are expected to drive long-term growth in the region.

Key Players in the Art Toy Market

- Pop Mart International

- Medicom Toy Corporation

- Kidrobot

- Mighty Jaxx

- Funko

- Superplastic

- Kaws Studio

- Threezero

- Hot Toys

- Good Smile Company

- Bandai Namco

- Hasbro

- LEGO

- Toy2R

- Bearbrick