Art Insurance Market Size

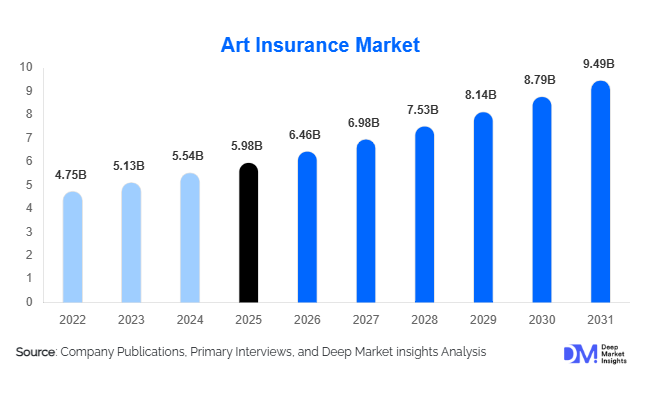

According to Deep Market Insights, the global art insurance market size was valued at USD 5.98 billion in 2025 and is projected to grow from USD 6.46 billion in 2026 to reach USD 9.49 billion by 2031, expanding at a CAGR of 8.0% during the forecast period (2026–2031). The art insurance market growth is primarily driven by the increasing financialization of fine art assets, rising global wealth among high-net-worth individuals, and expanding international trade of artworks through auctions, galleries, and online marketplaces. Growing awareness regarding risk mitigation for high-value collections, alongside increasing investments in museums, luxury hospitality, and cultural infrastructure, is further strengthening market demand globally.

Key Market Insights

- Fine art insurance remains the largest segment, driven by increasing investments in paintings, sculptures, rare collectibles, and museum-grade artworks.

- North America dominates the global art insurance market, supported by the strong presence of auction houses, private collectors, and institutional art investors.

- Asia-Pacific is emerging as the fastest-growing regional market, fueled by expanding wealth creation in China, India, Singapore, and Hong Kong.

- Blockchain-enabled provenance tracking and AI-based valuation systems are transforming underwriting accuracy and fraud prevention across the industry.

- Climate-related insurance coverage is gaining momentum, particularly among museums and galleries exposed to wildfire, flood, and extreme weather risks.

- Digital art and NFT-linked asset protection are creating new opportunities for insurers offering cyber-risk and tokenized asset coverage solutions.

Art Insurance Market Trends

Technology-Driven Underwriting and Authentication

The integration of advanced technologies is rapidly reshaping the global art insurance market. Insurers are increasingly adopting artificial intelligence for artwork valuation, risk modeling, and claims management. AI-powered platforms analyze auction histories, artist performance trends, restoration records, and market volatility to improve pricing accuracy and reduce underwriting risks. Blockchain technology is also gaining traction for provenance verification and ownership authentication, helping insurers mitigate fraud and title disputes associated with high-value artworks. In addition, IoT-enabled environmental monitoring systems installed in museums, galleries, and storage facilities allow real-time tracking of temperature, humidity, and lighting conditions, reducing the probability of damage-related claims. These technological advancements are enhancing transparency, operational efficiency, and customer trust across the art insurance ecosystem.

Growing Demand for Climate and Catastrophe Coverage

Climate-related risks are becoming a major focus area within the art insurance market. Increasing occurrences of floods, hurricanes, wildfires, and extreme weather events are threatening museums, galleries, and private collections globally. As a result, insurers are expanding catastrophe-focused coverage solutions and introducing climate resilience consulting services for art institutions and collectors. Museums and galleries are increasingly investing in disaster preparedness infrastructure, climate-controlled storage, and preventive conservation systems to minimize exposure. Insurance providers are also incorporating environmental risk assessments into underwriting models, particularly for collections located in vulnerable regions. This growing emphasis on climate resilience is expected to significantly influence premium structures and policy customization over the coming years.

Art Insurance Market Drivers

Rising Investments in Fine Art as an Alternative Asset

Fine art is increasingly being treated as an investment-grade alternative asset class alongside luxury watches, rare wines, and collectibles. Wealthy investors, family offices, and institutional buyers are diversifying portfolios through acquisitions of high-value artworks due to their long-term value appreciation potential. Growing participation in international auctions and private sales has elevated the need for specialized insurance solutions covering transit, storage, restoration, and title protection. The increasing monetization of art collections through lending and asset-backed financing is also encouraging collectors to adopt comprehensive insurance coverage to protect portfolio value.

Expansion of Global Wealth and Luxury Asset Ownership

The rapid rise in high-net-worth and ultra-high-net-worth individuals globally is significantly driving demand for art insurance services. Wealth creation across North America, Asia-Pacific, and the Middle East has accelerated purchases of fine art, luxury collectibles, and private museum collections. Corporate offices, luxury hotels, premium residential projects, and hospitality developments are increasingly integrating curated art collections into their branding strategies, further supporting market expansion. Rising affluence among younger collectors and increasing interest in contemporary art investments are also contributing to stronger premium growth globally.

Art Insurance Market Restraints

Complex Artwork Valuation and Pricing Volatility

One of the major restraints within the art insurance market is the complexity associated with artwork valuation. Pricing of artworks is highly subjective and often influenced by artist reputation, auction demand, historical significance, and market sentiment. Fluctuations in global auction prices create challenges for insurers attempting to determine accurate replacement values and underwriting premiums. Disputes related to restoration costs, authenticity, and title ownership further complicate claims settlement processes and increase operational risks for insurers.

Limited Insurance Penetration in Emerging Markets

Despite growing art markets in Asia, Latin America, and Africa, awareness regarding specialized art insurance remains relatively low among emerging collectors and smaller institutions. Many collectors in developing regions still perceive art insurance premiums as expensive or unnecessary, particularly for mid-value collections. Additionally, inconsistent regulatory frameworks and lack of standardized authentication systems in some countries create challenges for insurers seeking expansion into newer regional markets. These factors may restrict market penetration and limit premium growth potential over the forecast period.

Art Insurance Market Opportunities

Expansion of Digital Art and NFT Insurance Solutions

The rapid emergence of digital art ownership and NFT-linked assets is creating significant opportunities within the art insurance market. Although NFT transaction volumes have fluctuated in recent years, institutional interest in tokenized artwork ownership continues to increase globally. Insurers are beginning to develop specialized products covering cyber theft, smart contract vulnerabilities, digital wallet breaches, and authentication disputes. Hybrid policies combining physical artwork protection with digital asset coverage are also gaining traction among collectors. As regulatory clarity around digital ownership improves, insurers entering this segment early are expected to establish long-term competitive advantages.

Growth of Private Museums and Luxury Hospitality Collections

Rising investments in private museums, luxury hotels, premium commercial spaces, and branded residences are creating strong demand for customized art insurance policies. Hospitality groups and real estate developers increasingly use curated art collections to enhance customer experience and strengthen brand positioning. Countries such as the UAE, China, Singapore, and the United States are witnessing major investments in cultural infrastructure and luxury tourism projects incorporating museum-grade artworks. This trend is expected to create substantial opportunities for insurers specializing in collection management, transit insurance, and catastrophe protection solutions.

Insurance Type Insights

Fine art insurance dominates the global art insurance market, accounting for nearly 38% of total market share in 2025. Demand within this segment is driven by increasing acquisitions of paintings, sculptures, rare manuscripts, and contemporary artworks among private collectors and institutional buyers. Museum insurance is another major segment supported by growing investments in cultural infrastructure and international exhibitions. Exhibition and transit insurance is expanding rapidly due to rising cross-border movement of artworks between galleries, auction houses, and museums. Gallery and dealer insurance remains critical for protecting inventory, public liability, and event-related risks, while title and provenance insurance is witnessing growing adoption due to increasing concerns regarding authenticity verification and ownership disputes. Coverage for digital art and NFT-linked assets is also emerging as a niche but fast-growing category within the market.

Coverage Type Insights

All-risk coverage remains the leading coverage type within the art insurance market, accounting for approximately 42% of total market share in 2025. Collectors and institutions increasingly prefer comprehensive policies that combine theft, accidental damage, transit, and environmental protection under a single structure. Theft and burglary coverage continue to witness strong demand, particularly for private collections and galleries in urban centers. Climate and catastrophe coverage is emerging rapidly as museums and collectors seek protection against floods, hurricanes, and wildfire-related losses. Restoration and conservation insurance is also growing steadily due to rising restoration costs associated with aging collections and museum-grade artworks. Cyber and digital asset coverage is expected to gain stronger traction as tokenized art ownership expands globally.

Customer Type Insights

Individual collectors represent the largest customer segment in the global art insurance market, contributing nearly 34% of overall market demand in 2025. Increasing wealth accumulation among high-net-worth and ultra-high-net-worth individuals is supporting strong growth within this category. Institutional buyers, including museums, universities, foundations, and government cultural bodies, remain major contributors to premium volumes due to the large-scale value of insured collections. Commercial entities such as galleries, auction houses, luxury hotels, and corporate offices are increasingly investing in customized policies covering public liability, transportation risks, and exhibition-related damage. Demand from hospitality and luxury real estate sectors is also accelerating as curated art collections become central to premium branding strategies.

Distribution Channel Insights

Brokers and specialty underwriters dominate the art insurance market, accounting for nearly 47% of global market share in 2025. The complexity of artwork valuation, provenance assessment, and claims management requires highly specialized underwriting expertise, making brokers the preferred channel for large-value collections. Direct insurance providers continue to expand their art-focused divisions through strategic partnerships with galleries, museums, and auction houses. Digital insurance platforms are gradually emerging for smaller collectors and online art buyers seeking simplified policy issuance and valuation services. Embedded insurance solutions integrated into online auction platforms and art marketplaces are also gaining traction as digital art transactions increase globally.

Technology Insights

Traditional valuation-based underwriting continues to dominate the market with approximately 62% share in 2025, primarily due to reliance on expert appraisals and auction-based pricing models. However, AI-driven risk assessment is rapidly gaining popularity among insurers seeking to improve pricing precision and reduce fraud exposure. Blockchain-enabled provenance verification systems are increasingly being adopted to address authenticity disputes and ownership transparency challenges. IoT-based environmental monitoring technologies are also expanding across museums and galleries, enabling real-time tracking of humidity, lighting, and storage conditions to reduce damage-related risks. These technological innovations are expected to significantly transform underwriting and claims management processes over the forecast period.

| By Coverage Type | By Artwork Type | By Customer Type | By Distribution Channel | By End Use |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounted for nearly 39% of the global art insurance market in 2025, making it the largest regional market worldwide. The United States dominates regional demand due to its concentration of auction houses, private collectors, museums, and institutional art investors. Cities such as New York, Los Angeles, and Miami remain global centers for fine art transactions and international exhibitions. Increasing investments in private museums and luxury hospitality projects are further strengthening demand for specialized insurance coverage. Canada also contributes steadily through museum expansion initiatives and growing adoption of high-value collectibles among affluent consumers.

Europe

Europe represented approximately 31% of global market share in 2025, supported by its strong cultural heritage infrastructure and established art trading ecosystem. The United Kingdom remains the largest European market due to London’s position as a global auction and gallery hub. France and Italy continue to witness strong demand driven by museum preservation projects and heritage art collections. Switzerland plays a major role in secure art storage and international art logistics through its advanced freeport infrastructure. Germany is also experiencing increasing demand from corporate offices and institutional collectors investing in curated art collections.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market and is projected to expand at a CAGR exceeding 10% through 2031. China leads regional demand due to rapid wealth creation, expansion of domestic auction markets, and increasing government support for cultural industries. Hong Kong remains a major international art trading hub, while Singapore is strengthening its role as a secure art storage and finance center. India is witnessing rising demand from luxury real estate developers, hospitality operators, and emerging private collectors. Japan and South Korea continue to maintain stable demand from museums, galleries, and institutional buyers.

Latin America

Latin America is gradually emerging within the global art insurance market, with Brazil and Mexico representing the largest regional contributors. Rising participation in international art fairs and increasing acquisitions among wealthy collectors are supporting regional market growth. Demand remains concentrated among urban collectors, galleries, and institutional buyers seeking transit and exhibition-related insurance solutions. Brazil continues to lead regional expansion due to its strong domestic art ecosystem and growing luxury collectibles market.

Middle East & Africa

The Middle East & Africa region is witnessing growing demand driven by significant investments in cultural tourism and museum infrastructure. The UAE, particularly Dubai and Abu Dhabi, is becoming a major center for luxury art exhibitions, hospitality collections, and private museums. Saudi Arabia’s cultural transformation initiatives are expected to further stimulate demand for art insurance solutions over the coming years. South Africa remains an important regional market due to its established gallery ecosystem and growing participation in international art exhibitions.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Art Insurance Market

- Chubb Limited

- AXA XL

- American International Group (AIG)

- Allianz Group

- Zurich Insurance Group

- Hiscox Ltd.

- Tokio Marine Holdings

- Liberty Mutual

- CNA Financial

- Travelers Companies

- Markel Corporation

- Sompo Holdings

- QBE Insurance Group

- Generali Group

- Ping An Insurance