Arcade Machines Market Size

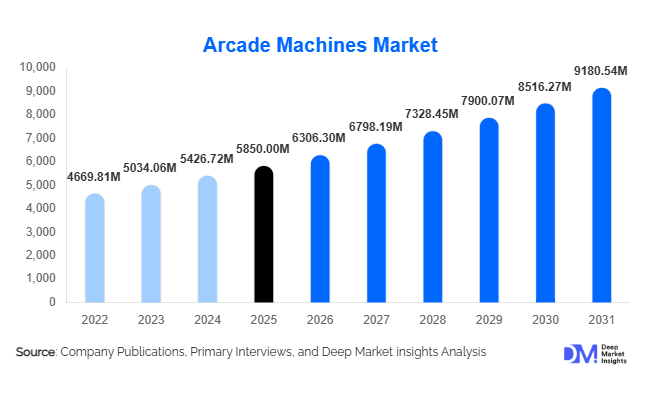

According to Deep Market Insights, the global arcade machines market size was valued at USD 5,850 million in 2025 and is projected to grow from USD 6,306.30 million in 2026 to reach USD 9,180.54 million by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). The arcade machines market growth is primarily driven by the increasing popularity of location-based entertainment, rising adoption of immersive VR and AR gaming technologies, and the resurgence of retro gaming culture, creating opportunities for both traditional and high-tech arcade systems across global entertainment centers.

Key Market Insights

- Arcade machines are increasingly integrating immersive technologies, such as VR, AR, and motion-based gaming, enhancing user engagement and providing experiences that cannot be replicated in home gaming.

- Family entertainment centers and theme parks dominate installations, offering high footfall and multi-attraction setups where arcade machines act as revenue-generating anchors.

- Asia-Pacific leads global demand, with countries like China, Japan, South Korea, and India driving growth due to rising disposable incomes and urban entertainment infrastructure expansion.

- North America remains a mature market, particularly the United States, where retro arcades, immersive FECs, and bar-arcade hybrids contribute to high consumer engagement.

- Connected and cashless arcade systems are transforming revenue models, enabling subscription-based play, loyalty programs, and detailed analytics for operators.

- Technological adoption and digital transformation are reshaping the arcade industry, with cloud-based systems, IoT integration, and AI-driven game optimization becoming standard for competitive operators.

What are the latest trends in the arcade machines market?

Immersive and Connected Gaming Experiences

Arcade operators are increasingly incorporating VR, AR, and motion-based technologies to offer fully immersive experiences. Multiplayer VR simulators, augmented reality shooters, and interactive rhythm games are redefining arcade entertainment, encouraging repeat visits and higher engagement. Connected systems, including cloud-based gameplay and card or RFID payment integration, allow operators to track usage patterns, optimize game placement, and introduce subscription models. The trend appeals to younger, tech-savvy audiences seeking social and interactive gaming experiences outside the home, while also enabling operators to monetize premium content effectively.

Retro Gaming Revival

Nostalgia-driven demand is fueling a resurgence of classic video arcade machines, pinball, and redemption games. Operators are refurbishing and retrofitting classic cabinets with modern display and connectivity features, attracting collectors, families, and older demographics who grew up with these games. Combining retro gameplay with new technologies, such as leaderboard integration and online score sharing, creates a hybrid experience that caters to multiple audience segments simultaneously. The trend is particularly strong in North America and Europe, where bar-arcade hybrids and retro FECs have become social hubs.

What are the key drivers in the arcade machines market?

Rising Demand for Location-Based Entertainment (LBE)

Urban populations are increasingly seeking social and experiential entertainment outside the home. Arcades, particularly those in malls, theme parks, and family entertainment centers, provide a communal environment where players of all ages can engage. LBE facilities benefit from high footfall, extended dwell time, and cross-attraction spending, making arcade machines a core revenue driver. This trend is expected to continue as operators diversify offerings and integrate immersive attractions to enhance customer experiences.

Technological Innovation in Gaming Hardware

Advances in display technology, motion sensors, VR, AR, and cloud connectivity have transformed arcade machines into high-tech, engaging platforms. Premium systems provide immersive experiences that cannot be replicated by consoles or mobile gaming, giving arcades a competitive advantage. Innovation also supports monetization through higher pricing tiers, subscription models, and loyalty programs. Continuous R&D by major manufacturers ensures a steady pipeline of novel games and interactive hardware, attracting both new and repeat players.

Revival of Retro Gaming Culture

Classic arcade machines and themed FECs are experiencing renewed popularity among older demographics and gaming enthusiasts. Operators are refurbishing or licensing retro games with updated hardware, appealing to nostalgia while incorporating digital connectivity for enhanced engagement. The dual demand for retro and modern experiences allows arcade operators to maximize revenue and cater to multiple consumer segments simultaneously.

What are the restraints for the global market?

High Capital and Maintenance Costs

Advanced arcade machines, particularly VR, motion-based simulators, and large-scale setups, require significant initial investments and ongoing maintenance. Smaller operators may find the capital expenditure prohibitive, limiting market penetration in emerging regions. Maintenance challenges include hardware wear, software updates, and high repair costs for complex systems, which can reduce profitability.

Competition from Home and Mobile Gaming

The rise of high-quality console, PC, and mobile gaming limits footfall in traditional arcades. To remain competitive, operators must differentiate through immersive, social, and location-based experiences. Failure to innovate can result in declining engagement and revenue, especially among younger audiences who have access to convenient, home-based alternatives.

What are the key opportunities in the arcade machines industry?

Emerging Markets Expansion

Asia-Pacific, the Middle East, and Latin America are experiencing rapid growth in arcade demand. Urbanization, rising disposable incomes, and government investments in entertainment infrastructure are driving the establishment of malls, FECs, and theme parks. India, the UAE, and Brazil are emerging as high-growth markets for both retro and high-tech arcade machines. Localized game content and cultural customization present additional opportunities for operators and manufacturers to capture these markets.

Integration of Immersive Technologies

The adoption of VR, AR, and motion-based systems presents high-margin opportunities for operators. Immersive arcade zones attract premium pricing and extended dwell time, enhancing profitability. New entrants can leverage modular VR/AR platforms to scale operations efficiently while offering differentiated experiences that cannot be replicated at home.

Digital and Cashless Revenue Models

Transitioning to cashless and subscription-based gaming systems enables operators to track player engagement, optimize machine placement, and personalize experiences. Loyalty programs, cloud-connected analytics, and in-game digital purchases create new monetization channels. This approach also facilitates targeted marketing and enhances customer retention.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5850 Million |

| Market Size in 2026 | USD 6306.30 Million |

| Market Size in 2031 | USD 9180.54 Million |

| CAGR | 7.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Video arcade machines dominate the market, accounting for approximately 32% of global share in 2025, driven by their versatility, scalability, and ability to cater to a broad demographic base. These machines integrate advanced graphics, multiplayer capabilities, and immersive gameplay, making them highly adaptable across locations such as malls, FECs, and standalone arcades. The leading driver behind this segment’s dominance is the continuous evolution of gaming content and hardware, enabling operators to refresh user experiences frequently and maintain high engagement levels.

Redemption machines and electromechanical systems follow, particularly popular among families and casual players due to their simple gameplay mechanics and reward-based incentives. These machines drive repeat visits and longer dwell times, especially in family entertainment centers. Meanwhile, VR/AR arcade machines are the fastest-growing segment, supported by increasing demand for immersive, location-based gaming experiences that cannot be replicated at home. Their growth is particularly strong in high-income regions where consumers are willing to pay premium prices. Pinball, rhythm, and kiddie ride machines continue to hold niche but stable demand, supported by nostalgia-driven consumers and younger audiences.

Application Insights

Family entertainment centers (FECs), theme parks, and shopping malls remain the dominant application areas, collectively accounting for over 55% of arcade machine installations. FECs lead this segment, supported by the growing trend of multi-attraction indoor entertainment complexes that combine gaming, dining, and social experiences. The primary growth driver for this segment is the increasing consumer preference for experiential entertainment, particularly among urban populations seeking social and group-based activities.

Emerging applications include cinemas, hotels, resorts, and airports, where arcade machines are used to enhance customer engagement and diversify revenue streams. Cinemas are increasingly integrating arcade zones to increase pre- and post-movie dwell time, while hotels and resorts are leveraging arcade setups to improve guest experiences. Airports and transit hubs are also adopting arcade machines to engage travelers during waiting periods, representing a growing niche segment. The continued expansion of retail and entertainment infrastructure globally is expected to further drive application growth.

Distribution Channel Insights

Direct sales dominate the market with approximately 45% share, as large-scale operators and entertainment chains prefer customized arcade machines along with long-term service agreements and technical support. The key driver for this dominance is the need for tailored solutions that align with specific themes, layouts, and customer demographics of large venues.

Leasing and rental models are gaining traction, particularly in emerging markets, as they reduce upfront capital expenditure and allow operators to upgrade machines more frequently. This model is especially attractive for small and mid-sized businesses aiming to enter the arcade market with limited investment. Distributor channels continue to play a critical role in serving regional operators by offering bundled solutions, installation services, and after-sales support. Additionally, digital platforms are becoming increasingly important, enabling manufacturers to showcase product portfolios, facilitate cross-border transactions, and expand their global reach efficiently.

Traveler Type / End-User Insights

Group players in family entertainment centers and themed arcades represent the largest segment, driven by the social and interactive nature of arcade gaming. Multiplayer experiences, competitive gaming formats, and group-based rewards systems encourage higher participation rates and repeat visits. The leading driver for this segment is the growing demand for shared entertainment experiences, particularly among younger consumers and families.

Individual players, especially teenagers and young adults, are driving demand for immersive and skill-based gaming experiences, including VR, AR, and competitive arcade systems. Families represent a stable and high-value segment, favoring mixed-audience machines and redemption-based games that appeal to all age groups. Additionally, bar-arcade and retro gaming enthusiasts form a niche but influential segment in North America and Europe, where nostalgia-driven entertainment and social gaming environments are gaining popularity.

Age Group Insights

Teenagers and adults aged 12–40 years account for the largest share of arcade users, driven by their strong affinity for interactive, competitive, and technology-driven gaming experiences. This segment benefits from higher disposable income (in the case of adults) and strong engagement with gaming culture. The key driver is the increasing integration of digital and immersive technologies that resonate with this demographic.

Younger players (12–18 years) are major contributors to the adoption of rhythm-based, multiplayer, and digital arcade games, while adults (18–40 years) show a strong preference for VR/AR systems and competitive gaming environments. Children below 12 years are primarily engaged through kiddie rides and family-friendly redemption machines, which are essential for driving footfall in family-centric venues. Older demographics contribute to steady demand through retro and nostalgia-based arcade experiences, particularly in developed markets.

Explore more data points, trends and opportunities Download Free Sample Report

Arcade Machines Market Segmentations

By Product Type

- Video Arcade Machines

- Redemption Machines

- Electromechanical Arcade Machines

- VR/AR Arcade Machines

- Pinball Machines

- Dance & Rhythm Machines

- Kiddie Ride Machines

By Application

- Family Entertainment Centers (FECs)

- Theme Parks & Amusement Parks

- Shopping Malls

- Cinemas & Multiplexes

- Hotels & Resorts

- Airports & Transit Locations

- Standalone Arcades

By Distribution Channel

- Direct Sales

- Distributors/Dealers

- Leasing & Rental Models

- Online/Digital Platforms

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global arcade machines market with approximately 38% share in 2025, led by China, Japan, South Korea, and India. The region’s leadership is driven by rapid urbanization, increasing disposable incomes, and large-scale expansion of malls and family entertainment centers. China acts as both a major consumer and manufacturing hub, benefiting from strong domestic demand and export capabilities. Japan and South Korea are technologically advanced markets, focusing on high-end arcade systems and innovation in gameplay. India is the fastest-growing market in the region, supported by rising middle-class spending, expansion of organized retail, and increasing penetration of FECs in tier-1 and tier-2 cities. Key growth drivers include favorable demographics, a large youth population, and growing investments in indoor entertainment infrastructure. Additionally, government support for manufacturing and digital innovation further strengthens regional growth.

North America

North America holds approximately 27% market share, with the United States as the dominant contributor. The region benefits from a mature entertainment industry, high consumer spending, and strong adoption of innovative gaming technologies. Growth is driven by the resurgence of retro arcades, expansion of immersive family entertainment centers, and the popularity of bar-arcade hybrids that combine gaming with social experiences. Technological advancements, including VR integration and cashless payment systems, are key drivers enhancing operator profitability and customer convenience. Canada contributes to steady regional growth through increasing adoption of family-oriented entertainment venues and mall-based arcade installations.

Europe

Europe accounts for approximately 20% of the global market, with major demand coming from the UK, Germany, and France. The region is characterized by a strong preference for experiential and social entertainment, which supports the adoption of both retro and modern arcade machines. Growth is driven by increasing investments in leisure infrastructure, tourism, and urban entertainment hubs. Additionally, European consumers are highly receptive to innovative and sustainable entertainment formats, encouraging operators to integrate energy-efficient machines and digital payment systems. The expansion of themed entertainment centers and cultural gaming experiences further supports market growth in the region.

Middle East & Africa

The Middle East & Africa region is an emerging market, led by the UAE, Saudi Arabia, and Qatar, and is witnessing the fastest growth with a CAGR exceeding 10%. High-income populations, coupled with strong government investments in tourism and entertainment infrastructure, are primary growth drivers. Initiatives such as Saudi Vision 2031 and large-scale development of entertainment cities and malls are significantly boosting demand for arcade machines. The UAE serves as a regional hub for advanced entertainment technologies, while increasing urbanization and rising youth populations across Africa present long-term growth opportunities.

Latin America

Latin America holds approximately 7% market share, with Brazil and Mexico as key contributors. Market growth is driven by urbanization, rising disposable incomes, and increasing investments in shopping malls and family entertainment centers. The region shows strong demand for cost-effective, mid-range arcade machines that cater to family audiences. Additionally, expanding retail infrastructure and growing adoption of organized entertainment formats are supporting the gradual penetration of arcade machines. While economic volatility remains a challenge, increasing consumer spending on leisure activities and the expansion of FEC chains are expected to drive steady growth in the region.

Key Players in the Arcade Machines Market

- Bandai Namco Entertainment

- Sega Sammy Holdings

- Raw Thrills

- LAI Games

- UNIS Technology

- Wahlap Technology

- Adrenaline Amusements

- Taito Corporation

- Konami Amusement

- Andamiro

- ICE (Innovative Concepts in Entertainment)

- Elaut Group

- Bay Tek Games

- Polin Waterparks (arcade division)

- Panda Game Manufacturing