Appliance Rentals Market Size

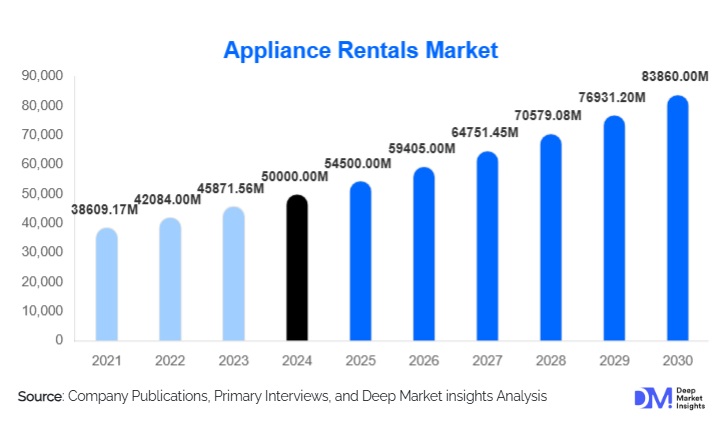

According to Deep Market Insights, the global appliance rentals market size was valued at USD 50,000 million in 2025 and is projected to grow to USD 54,500 million in 2026 and further reach USD 83,860 million by 2031, expanding at a CAGR of 9.0% during the forecast period (2026–2031). The appliance rentals market growth is primarily driven by rising urban migration, increasing adoption of flexible living arrangements, and the growing preference for subscription-based and circular-economy consumption models. Demand is further enhanced by housing mobility, student migration, and the rising cost of appliance ownership across major global economies.

Key Market Insights

- Rapid urbanization and increased rental housing penetration continue to fuel demand for household and major appliances on a subscription or rental basis.

- Online rental platforms and app-driven services are becoming the dominant distribution channels, offering convenience, transparent pricing, and fast delivery.

- Asia-Pacific leads global growth due to high population mobility, a young demographic profile, and expanding middle-class consumer bases.

- Residential consumers account for the largest share of appliance rental demand, driven by temporary housing, co-living spaces, and student accommodations.

- IoT-enabled and smart appliances are emerging as a premium rental category, with increasing demand among tech-savvy urban customers.

- Circular economy initiatives and sustainability-focused consumption are encouraging manufacturers and rental firms to offer refurbished appliances.

What are the latest trends in the Appliance Rentals Market?

Subscription-Based and Circular-Economy Models Gain Momentum

Subscription-based rental models are becoming a core trend in the appliance rentals market. Consumers are shifting from ownership to “usership,” preferring flexible, low-commitment monthly payments over large upfront purchases. Rental firms are integrating circular-economy frameworks, including refurbishment, redeployment, and extended appliance lifecycle management. This not only reduces waste but also lowers costs for providers and consumers. Manufacturers are increasingly entering the rental ecosystem by offering direct rental programs, allowing them to stabilize revenue streams and reduce reliance on annual sales cycles.

Technology-Driven Rental Platforms and Smart Appliance Integration

Digital transformation is reshaping the appliance rentals market. Online platforms and mobile apps enable customers to browse inventory, choose rental durations, schedule deliveries, and manage subscriptions seamlessly. Smart appliances, such as IoT-enabled refrigerators, connected washing machines, and smart HVAC units, are emerging as high-value rental offerings. Predictive maintenance, remote diagnostics, energy monitoring, and app-based controls enhance user experience and reduce operational downtime for rental providers. Technology integration is expected to become a decisive competitive differentiator for rental companies through 2031.

What are the key drivers in the Appliance Rentals Market?

Urbanization and Increased Housing Mobility

Global urban migration is accelerating demand for flexible living solutions. A rising share of the population rents apartments, relocates for work, or lives temporarily in student or shared housing, creating sustained demand for rented apartments. Long-term rental contracts (>6 months) are the most popular, accounting for over 60% of global demand in 2025. Rapid development of urban centers in Asia-Pacific, the Middle East & Africa, and Latin America further amplifies this trend.

Growing Preference for Affordability and Flexible Consumption

High upfront purchase costs for major appliances such as refrigerators, washing machines, and HVAC systems make renting an attractive alternative, especially for young professionals, students, and migrant workers. Rental models reduce financial burden and offer flexibility to upgrade or replace appliances without additional capital. Inflation, economic uncertainty, and shrinking household savings have further enhanced acceptance of rental and subscription alternatives.

Rise of Eco-Friendly and Sharing-Economy Lifestyles

Consumers are increasingly adopting sustainable lifestyles that prioritize access over ownership. Renting reduces e-waste, extends appliance lifecycles, and aligns with global sustainability goals. Governments promoting circular-economy initiatives are indirectly supporting the appliance rental sector. The combination of environmental awareness, resource conservation, and cost efficiency is a strong long-term driver of market expansion.

What are the restraints for the global market?

Maintenance, Hygiene, and Quality Concerns

Consumer hesitation toward used or refurbished appliances remains a major challenge. Perceived risks associated with reliability, hygiene, and potential breakdowns reduce adoption among quality-conscious customers. Ensuring rapid maintenance, reliable service networks, and high refurbishment standards increases operating costs for rental providers, affecting profitability.

High Logistics, Compliance, and Import Dependencies

Large appliances are expensive to transport, install, and service. In many regions, rental firms rely on imported appliances, making them vulnerable to trade tariffs, shipping delays, and regulatory restrictions. Differences in appliance safety standards, warranty liabilities, and energy-efficiency regulations further complicate cross-border operations and slow market expansion.

What are the key opportunities in the Appliance Rentals Industry?

Untapped Demand in Emerging Urban Centers

High population growth, rapid urban development, and increasing rental housing in emerging markets offer significant opportunities for rental firms. Tier-2 and Tier-3 cities across India, Southeast Asia, and Africa represent underserved markets where appliance ownership remains low but mobility is high. Strategic expansion into these regions can accelerate market adoption and increase long-term contract penetration.

Smart Appliance Rental Ecosystems

Rental providers can differentiate by offering IoT-enabled appliances with energy monitoring, remote diagnostics, and app-based control. These smart devices appeal to tech-savvy consumers and enable predictive maintenance, cutting service costs and reducing downtime. Smart appliance rentals also support subscription-based upgrade cycles, increasing customer lifetime value.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 50000 Million |

| Market Size in 2026 | USD 54500 Million |

| Market Size in 2031 | USD 83860 Million |

| CAGR | 9.0% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Major appliances dominate the market, contributing approximately 65–70% of global rental revenue in 2025. Refrigerators, washing machines, air conditioners, and large kitchen appliances are essential household items with high replacement costs, making them ideal rental products. Small appliances—such as vacuum cleaners, microwave ovens, and coffee machines—are expanding due to increasing demand from students, shared accommodations, and co-living spaces. Premium and smart appliances form a high-growth niche as consumers seek energy-efficient and technology-driven rental options.

Application Insights

Residential applications account for the largest share, driven by rental housing and young urban populations. Student housing and co-living spaces are rapidly expanding, supported by rising education mobility. Corporate housing and serviced apartments are increasingly adopting rental appliances to reduce CapEx and improve flexibility. Workforce housing projects, particularly in emerging markets, are generating additional rental volumes for mid-range and durable appliances. Temporary housing used for disaster relief and public housing programs also represents an emerging application segment.

Distribution Channel Insights

Online rental platforms lead global distribution, contributing 40–45% of bookings in 2025. Digital platforms allow real-time inventory visibility, subscription management, doorstep delivery, and maintenance scheduling. Offline rental stores maintain relevance in developing regions with low digital penetration, while OEM-driven rental programs are gaining traction as appliance manufacturers explore subscription-based business models. Mobile apps and influencer-led awareness campaigns are accelerating adoption among younger demographics.

Customer Type Insights

Residential consumers represent the dominant customer segment, accounting for 55–60% of the market. Students and young professionals drive short- and medium-term rentals, while families prefer long-term packages. Corporate clients—including serviced apartments and employee housing—are increasingly adopting rental models for essential appliances. Institutional customers, such as public housing authorities and NGOs, represent a smaller but growing segment, especially in regions undergoing rapid urban expansion or migration flows.

Explore more data points, trends and opportunities Download Free Sample Report

Appliance Rentals Market Segmentations

By Appliance Type

- Major Appliances (Refrigerators, Washing Machines, ACs, Dishwashers)

- Kitchen Appliances (Microwaves, Ovens, Cookers)

- Small Home Appliances (Vacuum Cleaners, Coffee Makers, Fans, Purifiers)

- Smart/IoT-Enabled Appliances

By Rental Duration

- Short-Term Rentals (<3 Months)

- Medium-Term Rentals (3–6 Months)

- Long-Term Rentals (>6 Months)

- Subscription/Lease-to-Own Models

By Customer Type

- Residential Consumers

- Student Housing & Shared Living

- Corporate & Serviced Apartments

- Migrant & Workforce Housing

- Institutional/Government

By Distribution Channel

- Online Rental Platforms

- Mobile App-Based Rentals

- Offline Rental Stores

- Direct OEM Rental Programs

Regional Insights

North America

North America accounts for 20–25% of global revenue, supported by high rental housing penetration and mature rental providers. U.S. consumers increasingly prefer flexible subscription models, while demand from corporate housing and student accommodations remains strong. Continued digital transformation of rental platforms and OEM-driven leasing programs contribute to market stability.

Europe

Europe holds a similar 20–25% share, driven by sustainability-focused consumers and circular-economy regulations. Western Europe, particularly the U.K., Germany, France, and the Netherlands, shows high adoption of rental appliances due to environmental awareness and the popularity of shared-living spaces. EU energy-efficiency standards also encourage the replacement of older appliances with modern rented alternatives.

Asia-Pacific

Asia-Pacific is the fastest-growing and largest region, representing 30–35% of global market share. Rising urban migration, a young population base, and corporatization of rental housing drive strong demand. India, China, Indonesia, and Vietnam are key high-growth markets, while Japan and South Korea show rising adoption of premium rental appliances. APAC’s rapid digitization further accelerates online rental volumes.

Latin America

Latin America accounts for 5–8% of the global market, with growth concentrated in Brazil, Mexico, and Colombia. Urban renters increasingly prefer mid-range rental appliances due to economic uncertainty and rising household mobility. Budget-conscious consumers are also driving demand for refurbished appliances in subscription-based models.

Middle East & Africa

MEA contributes 5–8% and demonstrates strong potential in the GCC and South Africa. High expatriate populations, workforce mobility, and expanding rental housing developments drive demand. African urban centers such as Nairobi, Lagos, and Johannesburg show emerging interest in rental appliances among growing middle-class households. Public housing initiatives and infrastructure investments support long-term growth prospects.

Key Players in the Appliance Rentals Market

- Prog Holdings, Inc.

- Aaron’s, Inc.

- Rent-A-Center

- Renta Centre

- GetFurnished

- Guarented

- EZ Rentals

- T & T Appliances

- FlexiRent (parent company only)

- Rentickle

- Furlenco (appliance division)

- Feather

- Lively

- CasaOne