Anti-Fog Lens Market Size

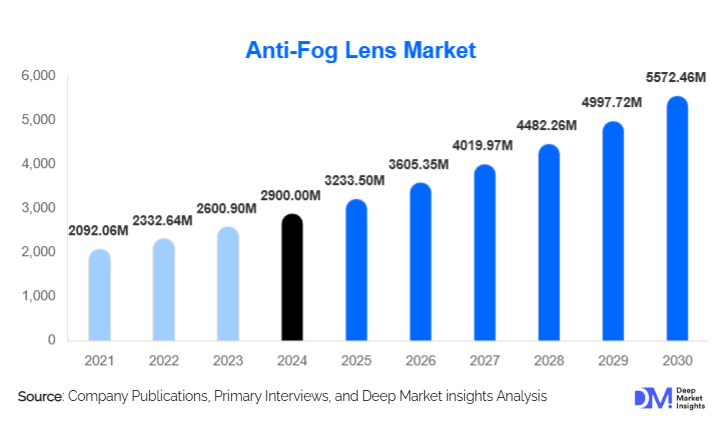

According to Deep Market Insights, the global anti-fog lens market size was valued at USD 2,900 million in 2025 and is projected to grow from USD 3,233.50 million in 2026 to reach USD 5,572.46 million by 2031, expanding at a CAGR of 11.5% during the forecast period (2026–2031). The market growth is primarily driven by increasing adoption of protective eyewear in healthcare, manufacturing, sports, and military sectors, along with rising demand for permanent anti-fog coating technologies in smart eyewear, helmets, and AR/VR devices.

Key Market Insights

- Healthcare and industrial safety are the largest demand drivers, supported by rising regulatory compliance and PPE adoption.

- Hydrophilic and nanotechnology-based anti-fog coatings are gaining traction due to superior durability and clarity.

- Polycarbonate lenses dominate due to impact resistance and compatibility with advanced coatings.

- Asia-Pacific is the fastest-growing region, driven by expanding manufacturing, smart wearables, and export-led production.

- B2B institutional procurement accounts for over 40% of market revenue, led by hospitals, defense, and industrial sectors.

- Integration with AR/VR smart eyewear is emerging as a major growth opportunity, especially in medical training, manufacturing, and defense simulations.

What are the latest trends in the Anti-Fog Lens Market?

Permanent Nanotechnology-Based Coatings Replacing Temporary Solutions

Manufacturers are shifting from temporary anti-fog sprays and wipes to permanent nano-engineered coatings that chemically bond to the lens surface. These coatings improve durability, scratch resistance, clarity, and fog prevention even in extreme humidity and temperature change scenarios. The nanostructured layers minimize micro-condensation by controlling how water molecules spread across the lens, preventing droplets from forming and distorting vision. This shift is particularly seen in healthcare, automotive, and smart eyewear sectors where long-term clarity and performance are critical, and where users cannot repeatedly reapply sprays during operations. OEMs are increasingly integrating permanent anti-fog coatings directly into production lines rather than offering them as aftermarket add-ons, which improves quality consistency and reduces maintenance needs. In addition, manufacturers are developing hybrid coatings that combine anti-fog with anti-scratch, anti-reflective, and UV-protective properties in a single multilayer stack, enabling premium positioning and higher margins. As certification bodies and large institutional buyers begin to prefer permanently coated lenses over temporary solutions in tenders, this trend is steadily becoming an industry baseline rather than a differentiating feature.

AR/VR-Integrated Smart Goggles and Protective Eyewear

Anti-fog lenses are increasingly being incorporated into AR/VR headsets used for industrial training, remote surgeries, smart manufacturing, and defense applications. Fogging poses significant hindrances when using head-mounted displays, especially in enclosed or mask-based environments where temperature and humidity rapidly fluctuate. The integration of anti-fog lens coatings with digital overlays, sensors, and HUDs is now a core focus for smart eyewear manufacturers, creating new technology partnerships and market opportunities. Vendors are designing coatings that maintain optical clarity without interfering with microdisplays, waveguides, or eye-tracking cameras embedded in the headset. This includes ensuring minimal light scattering, stable refractive index, and compatibility with infrared-based tracking systems. In industrial settings, fog-free AR goggles are being deployed on factory floors and in warehousing, where workers rely on real-time instructions and safety alerts displayed on lenses. In healthcare, surgeons and clinicians are adopting AR-assisted visualization tools that require crystal-clear lenses for long procedures under bright operating room lights. Defense and aerospace applications are also adopting anti-fog HUD visors for pilots and soldiers, where any visual obstruction can compromise mission safety. As AR/VR adoption scales, anti-fog functionality is becoming a core specification in smart headset procurement, not a secondary feature.

What are the key drivers in the Anti-Fog Lens Market?

Rising Adoption of PPE in Healthcare and Industrial Safety

The need for protective eyewear in hospitals, pharmaceuticals, chemical labs, and heavy industry has dramatically increased. Fogging impairs visibility and safety, especially for workers using masks and respirators, where warm exhaled air consistently contacts colder lens surfaces. Regulatory standards by OSHA, ISO, and regional safety authorities are pushing mandatory usage of anti-fog certified eyewear, boosting large-scale institutional demand. Post-pandemic infection control protocols have normalized routine use of goggles and face shields in many clinical and laboratory environments, which in turn has raised user expectations around comfort and uninterrupted visibility. In industrial segments such as mining, construction, metal fabrication, and chemical processing, safety managers are specifying fog-resistant eyewear in tenders to reduce accident risk and productivity losses caused by workers removing goggles to wipe lenses. This driver is reinforced by corporate ESG and safety performance targets, where reduced incident rates and improved compliance with PPE policies directly support broader sustainability and governance goals. As a result, anti-fog functionality is increasingly embedded in safety standards, rather than being treated as an optional upgrade.

Growth of Smart Eyewear and AR-Based Applications

Anti-fog lenses are becoming integral to AR-assisted helmets, HUD visors, and industrial smart glasses. These advanced applications require fog-free visual clarity for augmented displays, remote instruction, and precision automation. Any haze or droplet formation can distort overlay graphics, reduce legibility of critical data, and induce eye fatigue over prolonged use. The adoption of AR smart goggles in manufacturing, logistics, field service, and utilities is accelerating demand for high-quality anti-fog lens materials that maintain clarity during physically demanding and thermally variable tasks. In aviation and defense, AR/HUD-enabled visors are being deployed for navigation, targeting, and situational awareness, where visual reliability is non-negotiable. Similarly, in medical settings, AR-based visualization tools for minimally invasive surgery and telemedicine depend on lenses that remain clear under surgical lighting, sterility constraints, and mask usage. These trends are encouraging closer collaboration between lens material suppliers, coating specialists, and AR device OEMs to co-develop integrated optical stacks optimized for both display performance and fog resistance. As AR adoption moves from pilot projects to scaled deployments, demand for specialized anti-fog lenses embedded in these platforms is expected to rise steadily.

Focus on Durability and High-Performance Lens Materials

Polycarbonate and Trivex anti-fog lenses are increasingly favored for their lightweight, impact-resistant, and coating-friendly nature. These materials offer enhanced scratch resistance, UV protection, and clarity, particularly appealing to premium sports, defense, and eyewear manufacturers that require both safety and comfort. Their mechanical strength enables thinner designs without compromising impact resistance, which is important for extended wear and compatibility with helmets or headsets. From a manufacturing perspective, polycarbonate and Trivex substrates accept advanced hydrophilic and nanostructured coatings more reliably than many legacy plastics or glass, delivering longer service life in harsh environments. This focus on material quality also supports multi-functional lens designs combining anti-fog, anti-reflective, blue light filtering, and photochromic capabilities. For end-users, durable anti-fog lenses reduce replacement frequency and total cost of ownership, particularly in institutional settings where equipment is used by multiple shifts and exposed to frequent cleaning. As buyers increasingly evaluate lifecycle cost and performance rather than upfront price alone, high-performance materials are becoming a central driver of product selection.

What are the restraints for the global market?

High Cost of Permanent Nano-Coating Technologies

Advanced anti-fog coatings require precision manufacturing, high-grade substrates, and specialized curing processes, raising overall production costs compared with standard optical lenses or temporary anti-fog treatments. The need for cleanroom environments, plasma treatment, UV curing, or vacuum deposition systems adds capital expenditure and operating complexity for lens manufacturers. This limits adoption in cost-sensitive regions and among budget eyewear providers that compete primarily on price. For many smaller manufacturers and local brands, investing in the equipment and process know-how required for consistent permanent coatings can be prohibitively expensive, pushing them to continue offering simpler, lower-performance solutions. Additionally, the integration of multi-layer coatings that combine anti-fog with anti-scratch and anti-reflective properties can further increase per-unit cost, leading some institutional buyers to restrict such features to critical-use cases only. Until economies of scale, process optimization, and broader technology diffusion reduce costs, price sensitivity will remain a meaningful restraint in the lower and mid-tier segments.

Limited Consumer Awareness and Preference for Low-Cost Solutions

Many consumers still rely on cheap anti-fog sprays and wipes rather than permanent solutions, largely because they are more familiar, easy to purchase, and require lower initial expenditure. In mass-market retail channels, the differentiation between standard lenses and permanently coated anti-fog lenses is not always clearly communicated, resulting in limited willingness to pay a premium. Educating lower-tier markets about long-term performance advantages, reduced maintenance, and safety benefits remains a challenge for premium manufacturers and optical retailers. In addition, some users underestimate the risks associated with fogging in everyday activities such as driving, commuting, or recreational sports, perceiving anti-fog functionality as a convenience rather than a safety feature. In the absence of strong consumer pull, many retailers prioritize fast-moving, lower-priced products, which slows the penetration of advanced anti-fog lenses outside professional and industrial applications. Overcoming this restraint requires targeted awareness campaigns, clearer labeling, and demonstration of tangible benefits in real-world scenarios.

What are the key opportunities in the Anti-Fog Lens Market?

Integration into AR/VR and Smart Vision Applications

The rapid growth of augmented and virtual reality in medical training, manufacturing, aerospace, and defense creates significant opportunities for anti-fog lenses specifically designed for smart displays, sensor overlays, and dynamic interfaces. Fog-free clarity enhances user experience, enabling precision and safety when users rely on real-time visual data for instructions, diagnostics, or mission-critical decisions. As AR/VR devices are increasingly used in high-humidity, high-activity, or PPE-dependent environments, OEMs are actively seeking lens partners who can deliver coatings optimized for both optical performance and environmental robustness. This includes solutions that maintain consistent transmission, minimal distortion, and compatibility with eye-tracking and gesture-recognition systems. Anti-fog lens specialists have the opportunity to position themselves as core technology enablers within AR/VR ecosystems, co-developing reference designs and standards with hardware manufacturers. Long-term device replacement cycles, subscription-based AR service models, and enterprise-wide deployments further strengthen the revenue potential associated with this opportunity.

Regulatory Incentives and Compliance-Driven Growth

Governments worldwide are making anti-fog protective eyewear mandatory for healthcare and hazardous work environments, either directly through regulations or indirectly via safety guidelines and accreditation requirements. This creates major institutional procurement opportunities for certified anti-fog lens suppliers that can meet specific performance benchmarks and certification standards. Public-sector investments in hospital infrastructure, pharmaceutical manufacturing, and industrial modernization often include budget allocations for PPE, including fog-resistant goggles and face shields. As inspection bodies and insurance providers link safety compliance to reduced liability and premium benefits, companies are incentivized to upgrade to certified anti-fog eyewear. Emerging economies that are formalizing occupational safety frameworks represent additional growth potential, as they transition from ad hoc usage of basic eyewear to standardized, regulation-driven procurement. Suppliers that align their product portfolios with evolving standards and offer documentation, testing data, and compliance support stand to gain from multi-year contracts and framework agreements.

Premium Sportswear, Helmet Visors, and Tactical Eyewear

Growing demand for high-performance eyewear for cycling, skiing, scuba diving, aviation helmets, and military goggles presents a lucrative opportunity for permanent anti-fog solutions that offer clarity, durability, and impact resistance. Athletes and outdoor enthusiasts increasingly expect equipment that performs reliably across rapidly changing temperatures, such as moving from cold outdoor air to warmer indoor environments or operating in high-exertion conditions where sweat and breath increase humidity. In motorsports and two-wheeler commuting, fog-free helmet visors are becoming a key safety differentiator, particularly in markets with rising helmet adoption and stricter traffic regulations. Military and law-enforcement units also require tactical eyewear that remains clear in combat, training, and riot-control situations, where users often wear masks, gas filters, or respirators. This segment supports premium pricing and brand differentiation, as users are willing to pay more for verified performance and comfort. Co-branding opportunities between lens manufacturers and sports, helmet, or tactical gear brands further strengthen the commercial appeal of this opportunity.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2900 Million |

| Market Size in 2026 | USD 3233.50 Million |

| Market Size in 2031 | USD 5572.46 Million |

| CAGR | 11.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Material Type Insights

Polycarbonate lenses lead the market, holding a 38% share in 2025, due to their superior impact resistance, lightweight properties, and ideal compatibility with both hydrophilic and nanoparticle-based anti-fog coatings. Their dominance is particularly strong in sports eyewear, industrial goggles, and defense applications where impact protection and wearer comfort are critical. Polycarbonate’s ability to be molded into thin yet robust designs enables manufacturers to create ergonomic frames and large-coverage shields without adding significant weight. This is especially important in environments where eyewear is worn for long periods, such as manufacturing shifts, medical procedures, or prolonged training sessions. Additionally, polycarbonate’s thermal stability and surface characteristics support uniform coating adhesion, which reduces defects and enhances the long-term performance of anti

Explore more data points, trends and opportunities Download Free Sample Report

Anti-Fog Lens Market Segmentations

By Material Type

- Polycarbonate Lenses

- Glass Lenses

- CR-39 Plastic Lenses

- Trivex Lenses

- Acrylic Lenses

By Coating Technology

- Hydrophilic Anti-Fog Coatings

- Hydrophobic Anti-Fog Coatings

- Nanotechnology-Based Coatings

- UV-Curable Anti-Fog Coatings

- Permanent Anti-Fog Surface Treatments

By Application

- Healthcare & Medical Eyewear

- Industrial Safety Goggles

- Sports & Outdoor Eyewear

- Automotive Helmet Visors

- Optical Eyeglasses & Prescription Lenses

- Military & Tactical Eyewear

- AR/VR Smart Goggles & Smart Glasses

By Distribution Channel

- B2B Institutional Supply

- Offline Retail (Optical & Safety Stores)

- Online E-commerce

- Direct-to-Customer Manufacturer Platforms

By End-User Industry

- Healthcare

- Automotive

- Consumer Eyewear

- Defense & Aerospace

- Manufacturing & Construction

- Sports & Adventure Tourism

- Electronics & Smart Wearables

Regional Insights

North America

North America leads the market due to high institutional procurement in healthcare, manufacturing, aviation, and defense sectors. The U.S. is the largest market in the region, with robust adoption of permanent anti-fog technologies in protective optics and AR/VR defense equipment, supported by sizeable defense budgets and advanced industrial operations. Hospitals and integrated healthcare networks are key buyers of premium anti-fog goggles and face shields, driven by strict occupational safety laws and infection prevention protocols. In addition, the presence of major eyewear and safety equipment brands headquartered or strongly represented in the region accelerates innovation and product commercialization. Canada contributes through demand in mining, oil & gas, and heavy industry, where fog-free protective eyewear is critical for safety in harsh climates. High awareness of workplace safety, strong enforcement of OSHA-equivalent standards, and early adoption of smart eyewear solutions ensure that North America remains a technology-leading and value-rich regional market.

Europe (28% Market Share)

Europe exhibits strong demand from medical equipment providers, automotive helmet manufacturers, and premium eyewear brands. Germany, France, and the UK lead the region, supported by stringent EU industrial safety regulations and rigorous enforcement of personal protective equipment directives. European healthcare systems emphasize high-quality PPE standards, driving uptake of certified anti-fog goggles and lenses in hospitals, clinics, and laboratories. The region’s established motorcycle and motorsport culture, particularly in countries like Italy, Germany, and Spain, fuels demand for fog-resistant helmet visors and performance eyewear. Premium optical brands based in Italy, Germany, and France are also integrating anti-fog features into high-end frames and sports eyewear targeted at both domestic and international customers. Additionally, Europe’s strong focus on sustainability and product longevity aligns well with permanent anti-fog solutions that reduce the need for disposable wipes and sprays, reinforcing regional adoption of advanced coatings.

Asia-Pacific (Fastest Growing, CAGR 14.3%)

APAC is witnessing rapid demand growth due to expanding manufacturing hubs, medical device exports, smart eyewear production, and rising motorcycle helmet safety compliance. China and South Korea are major manufacturing centers for safety goggles, helmet visors, and optical components, supplying both regional and global markets. Japan and South Korea are at the forefront of AR/VR and smart wearable development, integrating anti-fog capabilities into next-generation headsets and industrial smart glasses. India, Indonesia, and Vietnam are driving large-volume demand for helmet visors and industrial protective eyewear, propelled by tightening road safety laws and formalization of industrial safety practices. As regional healthcare infrastructure expands, particularly in India, China, and Southeast Asia, hospitals and clinics are increasing their use of PPE and fog-resistant lenses. Competitive manufacturing costs combined with rising domestic consumption and robust export activity make Asia-Pacific the fastest-growing and strategically critical region for anti-fog lens suppliers.

Latin America

Brazil and Mexico are key markets in Latin America, driven by growing industrial safety compliance, rising motorcycle helmet regulations, and increasing adoption of medical PPE eyewear. In Brazil, sectors such as mining, oil & gas, construction, and agribusiness create demand for durable fog-resistant safety goggles and shields. Mexico’s manufacturing and automotive industries, closely linked with North American supply chains, are adopting anti-fog protective eyewear as part of broader workplace safety upgrades. Although overall purchasing power is lower than in North America and Europe, targeted regulations around industrial safety and road traffic are gradually supporting steady adoption. Local distributors and regional safety equipment brands play an important role in aggregating demand and partnering with global lens manufacturers to localize product offerings and pricing structures.

Middle East & Africa

Strong demand is seen in Saudi Arabia, UAE, South Africa, and Kenya due to defense modernization, healthcare infrastructure expansion, and regional manufacturing upgrades. In the Gulf countries, investments in advanced healthcare facilities, petrochemical plants, and industrial projects create robust demand for high-specification anti-fog PPE. Defense and security agencies in the Middle East are adopting tactical eyewear and helmet visors with permanent anti-fog coatings, often bundled with ballistic and UV protection. In Africa, South Africa and Kenya are leading markets, supported by growing mining, construction, and healthcare sectors. While affordability remains a constraint in many African countries, donor-funded health programs, multinational industrial projects, and regional safety initiatives are gradually increasing the penetration of certified anti-fog eyewear. Over time, as local manufacturing and distribution networks strengthen, Middle East & Africa is expected to transition from a niche to a structurally important growth contributor.

Key Players in the Anti-Fog Lens Market

- EssilorLuxottica

- ZEISS Group

- Hoya Corporation

- 3M Company

- Honeywell International

- Gentex Corporation

- PPG Industries

- Bolle Safety

- Johnson & Johnson Vision

- Uvex Group

- Sabic Innovative Plastics

- Oakley Inc.

- Pyramex Safety

- Shamir Optical

- Polaroid Eyewear