Animal and Pet Food Market Size

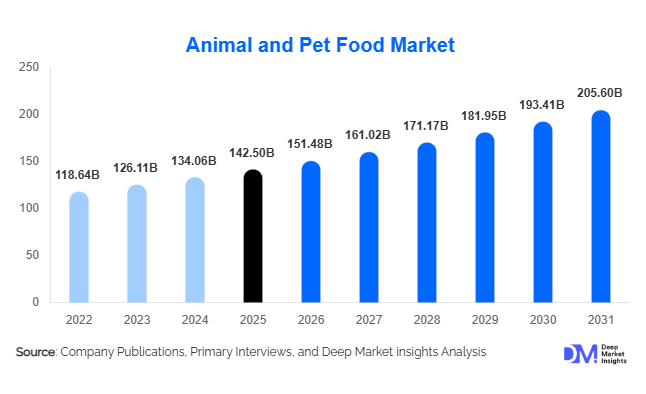

According to Deep Market Insights, the global animal and pet food market size was valued at USD 142.5 billion in 2025 and is projected to grow from USD 151.48 billion in 2026 to reach USD 205.60 billion by 2031, expanding at a CAGR of 6.3% during the forecast period (2026–2031). The growth of the animal and pet food market is primarily driven by increasing pet humanization, rising adoption rates of pets in urban regions, growing demand for premium and functional foods, and the expansion of e-commerce and subscription-based distribution channels globally.

Key Market Insights

- Dogs and cats dominate the market, accounting for the largest share of global consumption due to high ownership rates and greater nutritional requirements.

- Premium and functional pet foods are growing rapidly, as pet owners increasingly seek grain-free, organic, and health-enhancing diets for their pets.

- North America leads the market, with high spending per pet and strong adoption of e-commerce platforms for pet food purchases.

- Asia-Pacific is the fastest-growing region, driven by rising urban middle-class populations, increasing pet adoption, and premium product penetration in China and India.

- Sustainable and alternative protein sources, including insect-based and plant-based formulations, are creating new growth avenues for manufacturers.

- Technological adoption, such as personalized nutrition, automated production, and D2C subscription models, is reshaping consumer engagement and brand loyalty.

What are the latest trends in the animal and pet food market?

Premiumization and Functional Pet Nutrition

Pet owners increasingly perceive pets as family members, driving demand for premium, holistic, and functional foods. Products targeting digestive health, weight management, skin and coat improvement, and immunity are rapidly gaining market share. Grain-free, high-protein, and organic formulations have emerged as dominant trends in North America and Europe. Companies are investing in research to enhance nutritional profiles, develop veterinary prescription diets, and incorporate supplements such as probiotics, omega fatty acids, and vitamins. These innovations command higher price points and foster brand loyalty.

Sustainable and Alternative Protein Integration

Environmental concerns and ethical considerations are pushing manufacturers to explore insect-based, plant-based, and lab-grown proteins. Sustainability-driven consumers are increasingly favoring products with traceable, ethically sourced ingredients and environmentally friendly packaging. This trend is particularly evident in Europe and APAC, where regulatory support and consumer awareness are higher. Companies investing in alternative proteins are positioning themselves for long-term growth, appealing to environmentally conscious pet owners while differentiating from traditional competitors.

E-commerce and Direct-to-Consumer Growth

Online retail channels are transforming pet food distribution, offering convenience, a wide selection, and subscription-based models that ensure recurring sales. Consumers benefit from personalized recommendations and doorstep delivery, while brands collect valuable consumer data for targeted marketing. Subscription models and D2C platforms are particularly popular in the U.S., Europe, and APAC, where urban consumers prefer convenience and consistent product availability. Digital adoption has enabled niche and premium brands to reach untapped markets quickly, fueling growth across all segments.

What are the key drivers in the animal and pet food market?

Rising Pet Humanization

The trend of treating pets as family members has significantly increased spending on high-quality food, supplements, and health-oriented products. This has led to the rapid expansion of premium and functional pet food segments globally. Urban pet owners, particularly millennials and Gen Z, are willing to invest in specialty diets that promote long-term health, thereby driving growth in premium, organic, and veterinary diet categories.

Growth in Pet Ownership

Global pet adoption rates have surged, particularly in urban areas and emerging markets. Countries like China, India, and Brazil are witnessing unprecedented adoption, while North America and Europe maintain high ownership per household. This growth directly translates into rising food consumption and demand for variety, supporting market expansion and innovation in nutritional formulations.

Technological Advancements and E-commerce Penetration

Technological innovation, including automated production, digital subscription models, and personalized nutrition solutions, has enabled brands to improve efficiency and consumer engagement. E-commerce penetration has transformed distribution, allowing brands to reach a wider customer base while providing convenience and repeat purchase opportunities. Advanced analytics also help brands track preferences and optimize supply chains.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuating prices of meat, grains, fish, and other ingredients can significantly impact production costs and profit margins. Pet food manufacturers need to manage sourcing carefully to maintain profitability, especially in premium segments where ingredient quality is critical.

Regulatory Compliance and Quality Standards

Stringent regulations regarding ingredient sourcing, labeling, and safety pose challenges for manufacturers, particularly new entrants. Compliance with veterinary standards, organic certifications, and regional food safety laws adds operational complexity and can increase costs.

What are the key opportunities in the animal and pet food industry?

Emerging Market Expansion

Rapid urbanization and rising middle-class populations in Asia-Pacific and Latin America offer significant growth potential. Countries such as India, China, and Brazil remain underpenetrated, providing opportunities for new entrants and existing players to capture demand with localized, affordable, and premium offerings. Companies can leverage partnerships, tailored pricing, and culturally relevant marketing to accelerate adoption.

Functional and Health-Focused Pet Foods

Growing awareness of pet health is driving demand for functional foods targeting immunity, digestive health, joint care, and aging support. Premium veterinary diets and nutraceutical-enriched formulations are emerging as high-margin growth segments, particularly in North America and Europe. Investment in R&D for specialized diets is creating differentiation opportunities for manufacturers.

Sustainability and Alternative Ingredients

Brands adopting sustainable practices, including insect-based proteins, plant-based alternatives, and eco-friendly packaging, are better positioned to attract environmentally conscious consumers. These innovations are supported by regulatory initiatives and consumer trends, offering long-term differentiation and market growth potential.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 142.5 Billion |

| Market Size in 2026 | USD 151.48 Billion |

| Market Size in 2031 | USD 205.60 Billion |

| CAGR | 6.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Dry pet food continues to dominate the global animal and pet food market, accounting for approximately 42% of total market share in 2025. Its leadership is primarily driven by factors such as extended shelf life, ease of storage, cost efficiency, and convenience in bulk purchasing. Dry food also aligns well with the needs of multi-pet households and large dog owners, where affordability and portion control are critical. Additionally, advancements in extrusion technology have improved the nutritional quality and palatability of dry food, further reinforcing its dominance. Wet pet food is witnessing steady growth, particularly in premium and super-premium segments, as pet owners increasingly prioritize taste, hydration benefits, and high meat content. Treats and snacks are emerging as a high-margin category, driven by increased pet humanization and the trend of using treats for training, bonding, and functional benefits such as dental care.

Veterinary and prescription diets are among the fastest-growing categories, expanding at a CAGR of 7–8%, supported by rising awareness of pet health issues such as obesity, digestive disorders, and allergies. Functional and nutraceutical pet foods are also gaining traction, incorporating ingredients like probiotics, omega fatty acids, and joint-support compounds. Semi-moist foods and specialized formulations further diversify the product landscape, catering to specific dietary requirements and enhancing overall market value.

Animal Type Insights

The dog segment remains the largest contributor to the global pet food market, accounting for approximately 48% of total revenue in 2025. This dominance is primarily attributed to higher food consumption per animal, greater product variety, and increased spending on premium and functional diets for dogs. Dog owners are more likely to invest in specialized nutrition, including breed-specific, age-specific, and health-focused formulations, which significantly boosts segment value. Cats represent the second-largest segment, contributing around 36% of the market. Growth in the cat segment is particularly strong in urban environments, where space constraints make cats more suitable pets. The demand for wet food is notably higher in this segment due to cats’ hydration needs and dietary preferences.

Other animal categories, including birds, fish, reptiles, and small mammals, collectively account for a smaller share but are experiencing relatively faster growth in regions such as Asia-Pacific and Europe. This growth is driven by increasing interest in exotic pets, rising disposable incomes, and expanding product availability tailored to niche dietary requirements. The diversification of pet ownership beyond traditional cats and dogs is expected to create incremental growth opportunities for specialized pet food manufacturers.

Distribution Channel Insights

Supermarkets and hypermarkets continue to lead the distribution landscape, accounting for approximately 35% of total market share. Their dominance is driven by strong retail networks, consumer trust, and the ability to offer competitive pricing and bulk purchasing options. These channels are particularly popular for economy and mid-range pet food products, where price sensitivity and convenience are key decision factors. Online retail and direct-to-consumer (D2C) channels are the fastest-growing segments, expanding at double-digit growth rates. The rise of e-commerce is fueled by increasing internet penetration, urban lifestyles, and consumer preference for doorstep delivery. Subscription-based models are gaining traction, ensuring a consistent supply while enhancing customer retention and brand loyalty. Digital platforms also enable personalized recommendations, allowing companies to target specific pet needs more effectively.

Veterinary clinics play a critical role in the distribution of prescription and therapeutic diets, particularly for pets with medical conditions. Specialty pet stores remain important for premium and niche products, offering curated selections and expert advice. The evolving omni-channel strategy, combining offline and online touchpoints, is becoming essential for market players to maximize reach and consumer engagement.

Explore more data points, trends and opportunities Download Free Sample Report

Animal and Pet Food Market Segmentations

By Animal Type

- Dogs

- Cats

- Birds

- Fish & Aquatic Pets

- Small Mammals

- Reptiles & Exotic Pets

By Product Type

- Dry Pet Food

- Wet Pet Food

- Semi-Moist Pet Food

- Pet Treats & Snacks

- Veterinary Diets

- Functional & Nutraceutical Pet Food

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Pet Stores

- Veterinary Clinics

- Online Retail / E-commerce

- Direct-to-Consumer (D2C)

By Price Tier

- Economy

- Mid-Range

- Premium

- Super-Premium / Holistic

By Functionality

- Maintenance Diet

- Growth Diet

- Therapeutic / Medical Diet

- Weight Management

- Digestive & Skin Health

Regional Insights

North America

North America remains the largest regional market, accounting for approximately 35% of the global market share in 2025. The United States dominates the region, driven by high pet ownership rates, significant per-pet expenditure, and strong consumer preference for premium, organic, and functional pet foods. The presence of leading global manufacturers and well-established distribution networks further supports market growth. Additionally, the rapid adoption of e-commerce and subscription-based pet food services has enhanced accessibility and consumer convenience. Canada complements regional growth with increasing demand for high-quality and sustainably sourced pet food products.

Europe

Europe holds approximately 25% of the global market share, with key markets including Germany, France, and the United Kingdom. The region is characterized by a strong preference for sustainable, organic, and ethically sourced pet food products. Strict regulatory frameworks related to food safety and labeling enhance consumer trust and product quality, supporting market expansion. Additionally, increasing awareness of pet health and nutrition is driving demand for premium and functional products.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at a CAGR of approximately 8.5%. China and India are the primary growth engines, supported by rapid urbanization, rising disposable incomes, and increasing pet ownership among millennials. The growing middle class and changing lifestyles are driving demand for premium, functional, and imported pet food products. Japan and Australia represent mature markets with steady demand, particularly for high-quality and specialized diets.

Latin America

Latin America accounts for approximately 10% of the global market, with Brazil and Mexico leading regional demand. The market is characterized by growing pet adoption rates and improving retail infrastructure. While price sensitivity remains a key factor, there is a gradual shift toward premium products, particularly in urban areas. Local manufacturing and increasing availability of international brands are supporting market expansion.

Middle East & Africa

The Middle East and Africa region holds around 8% of the global market share. Growth is driven by countries such as the UAE, Saudi Arabia, and South Africa, where rising urbanization and increasing expatriate populations are boosting pet ownership. Premium pet food demand is particularly strong in the Middle East, supported by high disposable incomes and a preference for imported products. In Africa, the market is still developing but benefits from export-oriented production and regional trade. The animal and pet food market is moderately consolidated, with the top five players accounting for 45% of the global market share. Premium and functional product innovation, combined with strong branding, enable leading companies to maintain market dominance.

Key Players in the Animal and Pet Food Market

- Mars Petcare

- Nestlé Purina

- J.M. Smucker

- Hill’s Pet Nutrition

- General Mills (Blue Buffalo)

- Colgate-Palmolive

- Diamond Pet Foods

- Heristo AG

- Thai Union Group

- Unicharm Corporation

- Spectrum Brands

- WellPet LLC

- Deuerer GmbH

- Nutreco N.V.

- Freshpet Inc.