Airtight Containers Market Size

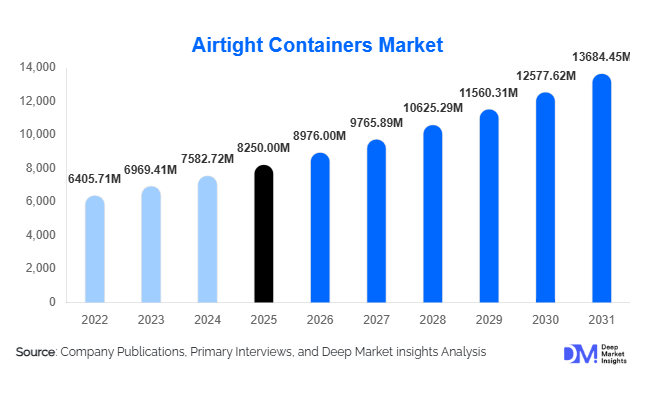

According to Deep Market Insights, the global airtight containers market size was valued at USD 8,250 million in 2025 and is projected to grow from USD 8,976 million in 2026 to reach USD 13,684.45 million by 2031, expanding at a CAGR of 8.8% during the forecast period (2026–2031). The airtight containers market growth is primarily driven by rising consumer awareness regarding food safety and preservation, increasing adoption of modular kitchen storage solutions, and expanding demand from food processing and foodservice industries worldwide. Growing urbanization, changing consumer lifestyles, and increased preference for organized storage solutions are further supporting market expansion. Manufacturers are increasingly introducing BPA-free plastics, glass-based premium storage products, and vacuum-sealed technologies to cater to evolving consumer expectations focused on hygiene, sustainability, and convenience.

Key Market Insights

- Plastic airtight containers dominate global demand due to affordability, durability, and wide residential usage.

- Asia-Pacific leads global consumption, supported by rapid urbanization and expanding middle-class populations.

- Residential households account for the majority of demand, driven by meal preparation trends and kitchen organization preferences.

- E-commerce sales channels are expanding rapidly, enabling brands to reach global consumers through direct-to-consumer models.

- Sustainable materials adoption is accelerating, with glass and stainless-steel containers gaining traction.

- Foodservice and cloud kitchen expansion is creating new commercial demand for high-performance storage solutions.

What are the latest trends in the airtight containers market?

Shift Toward Sustainable and BPA-Free Storage Solutions

The airtight containers industry is witnessing a strong transition toward eco-friendly materials as consumers increasingly prioritize sustainability and health safety. Manufacturers are replacing conventional plastics with BPA-free polymers, borosilicate glass, and recyclable materials to comply with tightening environmental regulations. Premium reusable storage products are gaining traction among environmentally conscious consumers, particularly in Europe and North America. Companies are also investing in recyclable packaging and circular product designs to reduce environmental impact. Sustainability certifications and eco-labeling are becoming key differentiators influencing purchasing decisions across retail and online platforms.

Rise of Modular and Space-Optimized Kitchen Storage

The growing popularity of modular kitchens and organized living spaces is transforming product innovation within the market. Stackable and uniform container designs that maximize pantry efficiency are increasingly preferred by urban households. Transparent containers enabling easy visibility of stored food items are gaining strong adoption. Social media-driven home organization trends are encouraging consumers to invest in aesthetically aligned storage systems. Manufacturers are responding by offering coordinated container sets designed specifically for modern kitchens, enhancing functionality while improving visual appeal.

What are the key drivers in the airtight containers market?

Growing Awareness of Food Preservation and Waste Reduction

Rising global concerns regarding food wastage and hygiene are major drivers of airtight container adoption. Airtight sealing technology helps extend shelf life by preventing moisture exposure, bacterial contamination, and odor transfer. Governments and sustainability organizations promoting food waste reduction initiatives are indirectly encouraging households and food businesses to adopt efficient storage solutions. Increased home cooking and meal-prepping practices further reinforce consistent product demand.

Expansion of Food Processing and Packaged Food Industry

The rapid growth of packaged foods and processed food production globally is significantly boosting demand for airtight storage systems. Food manufacturers rely on airtight containers for ingredient storage, inventory handling, and product quality preservation. Emerging economies such as India, China, and Southeast Asian countries are investing heavily in food processing infrastructure, driving commercial-scale adoption of durable storage solutions.

What are the restraints for the global market?

Raw Material Price Volatility

The industry remains sensitive to fluctuations in plastic resin, glass, and metal prices. Changes in petroleum-based raw material costs directly impact manufacturing expenses, creating pricing pressure for producers. Rising logistics costs and supply chain disruptions further influence product pricing and profit margins.

Environmental Concerns Around Plastic Usage

Despite widespread adoption, plastic containers face increasing regulatory scrutiny due to environmental concerns. Restrictions on single-use plastics and sustainability mandates require manufacturers to invest in alternative materials, increasing production costs and operational complexity. Transitioning to eco-friendly materials while maintaining affordability remains a key challenge for market participants.

What are the key opportunities in the airtight containers industry?

Expansion of Eco-Friendly Product Portfolios

Growing demand for sustainable kitchenware presents strong opportunities for innovation. Glass, stainless steel, and hybrid containers with recyclable components are gaining popularity among premium consumers. Companies investing in biodegradable materials and reusable storage ecosystems can unlock long-term growth potential and improve brand differentiation.

Commercial Demand from Cloud Kitchens and Food Delivery Ecosystems

The global expansion of cloud kitchens and food delivery services is creating new demand for professional-grade airtight storage solutions. Restaurants and catering operators increasingly require stackable, temperature-resistant containers for efficient ingredient management and food preservation. Manufacturers developing specialized commercial product lines can tap into this fast-growing segment.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8250 Million |

| Market Size in 2026 | USD 8976 Million |

| Market Size in 2031 | USD 13684.45 Million |

| CAGR | 8.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Modular airtight containers dominate the global airtight containers market, accounting for approximately 33% of total market share in 2025. The segment’s leadership is primarily driven by increasing consumer preference for organized and aesthetically coordinated kitchen storage systems that align with modern modular kitchen designs. Rising urbanization, smaller living spaces, and demand for efficient space utilization are encouraging households to adopt stackable and uniform storage solutions. Additionally, manufacturers are introducing modular systems with interchangeable lids, transparent materials, and ergonomic designs, further strengthening adoption.Jar-type containers continue to maintain strong demand, particularly for spice storage, dry ingredients, and pantry organization, owing to their familiarity, affordability, and ease of use. Meanwhile, vacuum airtight containers are emerging as a high-growth category as consumers increasingly prioritize food preservation, waste reduction, and longer shelf life. Technological advancements in vacuum sealing mechanisms and oxygen-control features are enhancing product appeal among health-conscious households.Stackable and clip-lock container designs are expanding rapidly due to their convenience, portability, and improved sealing performance. The growing popularity of coordinated container sets and premium kitchen organization solutions is also driving higher-value purchases globally. Leading Segment Driver: Increasing adoption of modular kitchens and consumer demand for space-efficient, organized food storage solutions continues to propel the modular container segment.

Application Insights

Dry food storage represents the largest application segment, contributing nearly 41% of global demand. Airtight containers are widely used for storing grains, cereals, pulses, flour, spices, and snacks, where protection against moisture, pests, and contamination is essential. Rising awareness regarding food hygiene and waste reduction is further strengthening adoption across residential and commercial kitchens.Refrigerated storage applications are expanding steadily alongside the global rise in meal-preparation practices and leftover food management. Freezer-safe containers are gaining traction among working households seeking convenience and longer food preservation cycles. Improvements in temperature-resistant materials and durable sealing technologies are enhancing product reliability across cold storage environments.Liquid storage applications are also witnessing growth due to advancements in leak-proof and spill-resistant sealing mechanisms, making containers suitable for soups, sauces, and beverages. Meal preparation and portion-control usage represent fast-growing application areas driven by fitness awareness, diet planning, and lifestyle shifts toward home-cooked meals.Leading Segment Driver: Increasing focus on food preservation, hygiene, and reduction of household food waste is the primary factor driving dominance of dry food storage applications globally.

Distribution Channel Insights

Offline retail channels dominate the airtight containers market with approximately 62% market share, supported by supermarkets, hypermarkets, department stores, and specialty kitchenware retailers. Consumers continue to prefer physical product evaluation, particularly for assessing material quality, sealing mechanisms, durability, and size suitability before purchase. Promotional in-store displays and bundled product offerings also support strong offline sales performance.However, online retail represents the fastest-growing distribution channel as e-commerce platforms provide broader product assortments, competitive pricing, customer reviews, and doorstep delivery convenience. The expansion of digital payment ecosystems and improved logistics infrastructure are accelerating online adoption across both developed and emerging markets.Direct-to-consumer (DTC) brand websites are gaining traction through personalized product bundles, subscription-based kitchen organization solutions, and exclusive product launches. Influencer marketing, social media demonstrations, and short-form video commerce are increasingly shaping purchasing decisions, particularly among younger consumers.Leading Segment Driver: Rapid expansion of omnichannel retail strategies and increasing consumer reliance on digital shopping platforms are fueling distribution channel evolution.

End-Use Insights

The residential segment leads the airtight containers market, accounting for nearly 58% of global demand. Growth is supported by rising urbanization, increasing home cooking trends, and greater emphasis on kitchen organization and food safety. Smaller households and compact living environments are encouraging consumers to invest in efficient storage solutions that maximize space utilization.The foodservice and hospitality sector represents the fastest-growing end-use segment, driven by restaurant expansion, cloud kitchen proliferation, and growing takeaway and delivery services. Airtight containers play a crucial role in ingredient storage, inventory management, and maintaining food quality standards.Food processing companies provide a stable demand base, utilizing airtight storage systems for ingredient preservation, quality control, and regulatory compliance. Healthcare and pharmaceutical applications are emerging niche areas where contamination-free and moisture-controlled storage environments are essential.Leading Segment Driver: Rising home cooking culture combined with increasing awareness of food hygiene and storage efficiency continues to drive residential segment dominance.

Explore more data points, trends and opportunities Download Free Sample Report

Airtight Containers Market Segmentations

By Material Type

- Plastic Airtight Containers

- Glass Airtight Containers

- Metal Airtight Containers

- Silicone Airtight Containers

- Hybrid / Composite Containers

By Product Type

- Modular Storage Containers

- Jar-Type Airtight Containers

- Vacuum Airtight Containers

- Stackable Airtight Containers

- Clip-Lock Airtight Containers

- Push-Button Lid Containers

- Meal Prep & Lunch Containers

By Application

- Dry Food Storage

- Refrigerated Storage

- Freezer Storage

- Liquid Storage

- Meal Preparation & Portion Control

By Distribution Channel

- Online Retail

- Hypermarkets & Supermarkets

- Specialty Kitchenware Stores

- Department Stores

- Direct-to-Consumer Brand Stores

By End-Use Industry

- Residential / Household

- Foodservice & Hospitality

- Food Processing Industry

- Retail & Packaging

- Healthcare & Pharmaceutical Storage

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global airtight containers market with approximately 39% market share in 2025. China leads regional demand due to its strong manufacturing ecosystem, large consumer base, and widespread availability of affordable storage products. India represents the fastest-growing market, supported by rising disposable incomes, expanding middle-class populations, and rapid adoption of modular kitchens in urban households. Japan and South Korea contribute significantly through premium product adoption and consumer preference for high-quality, durable storage solutions.Regional Growth Drivers: Rapid urbanization, expanding e-commerce penetration, increasing nuclear families, growth in organized retail, and rising awareness of food safety and waste reduction are key factors accelerating regional market expansion.

North America

North America accounts for nearly 26% of global demand, led primarily by the United States. Strong adoption of meal preparation practices, organized kitchen culture, and demand for premium and branded kitchenware products support market growth. Canada demonstrates rising preference for sustainable storage solutions, particularly glass and BPA-free containers aligned with environmentally conscious consumption trends.Regional Growth Drivers: Increasing health-conscious lifestyles, growth of meal-prep culture, high consumer spending capacity, innovation in sustainable materials, and strong penetration of online retail channels are driving regional demand.

Europe

Europe holds approximately 22% market share, with Germany, France, and the United Kingdom leading regional consumption. Strict environmental regulations promoting sustainable packaging and reusable materials are accelerating the shift toward glass, stainless steel, and recyclable plastic containers. European consumers prioritize product durability, design aesthetics, and eco-certifications.Regional Growth Drivers: Sustainability regulations, circular economy initiatives, increasing adoption of eco-friendly materials, and strong consumer preference for premium-quality household products are supporting market growth.

Latin America

Latin America contributes roughly 7% of global demand, led by Brazil and Mexico. Market expansion is supported by improving economic conditions, growing middle-class populations, and modernization of retail infrastructure. Increasing urban lifestyles and adoption of organized kitchen solutions are gradually strengthening product penetration.Regional Growth Drivers: Expansion of supermarkets and hypermarkets, rising disposable income levels, urban household growth, and increasing awareness of food preservation practices are fueling regional demand.

Middle East & Africa

The Middle East and Africa region is experiencing steady growth driven by expanding hospitality industries and increasing consumption of packaged and stored food products. The UAE and Saudi Arabia represent key markets supported by rapid urbanization, rising expatriate populations, and development of modern retail infrastructure.Regional Growth Drivers: Growth of tourism and hospitality sectors, rising modern retail penetration, changing dietary habits, and increasing demand for hygienic food storage solutions are contributing to regional market development.

Key Players in the Airtight Containers Market

- Tupperware Brands Corporation

- Newell Brands

- Lock & Lock Co., Ltd.

- Rubbermaid Commercial Products

- Sistema Plastics

- OXO International

- Anchor Hocking Company

- Snapware Corporation

- Luminarc

- Glasslock Co., Ltd.

- Hamilton Housewares Pvt. Ltd.

- Cello World Ltd.

- Tiger Corporation

- IKEA

- World Kitchen LLC