AirPods Protective Case Market Size

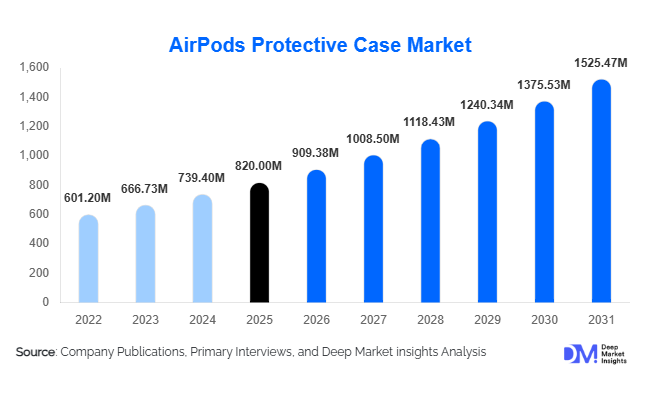

According to Deep Market Insights, the global AirPods protective case market size was valued at USD 820 million in 2025 and is projected to grow from USD 909.38 million in 2026 to reach USD 1,525.47 million by 2031, expanding at a CAGR of 10.9% during the forecast period (2026–2031). The market growth is primarily driven by the rapid adoption of wireless earbuds, increasing consumer preference for device protection and personalization, and the rising influence of lifestyle-driven accessories. As AirPods and similar premium audio devices become more ubiquitous, protective cases are evolving from basic utility products into fashion-forward and feature-rich accessories. The market is also benefiting from strong e-commerce penetration and direct-to-consumer brand expansion, enabling faster product innovation cycles and global reach.

Key Market Insights

- Protective cases are increasingly blending functionality with aesthetics, driving demand for designer, customizable, and premium materials such as leather and aluminum.

- Online retail dominates distribution, accounting for nearly 65% of total sales due to convenience, pricing transparency, and wide product availability.

- North America leads the market, supported by high AirPods penetration and strong consumer purchasing power.

- Asia-Pacific is the fastest-growing region, driven by rising middle-class income and expanding adoption of wireless earbuds.

- The mid-range pricing segment (USD 10–25) captures the largest share, balancing affordability and quality for mass consumers.

- Innovation in multifunctional cases, including battery integration and antimicrobial coatings, is emerging as a key differentiator.

What are the latest trends in the AirPods protective case market?

Rise of Premium and Lifestyle-Oriented Cases

Consumers are increasingly viewing AirPods cases as lifestyle accessories rather than purely functional products. This has led to a surge in demand for premium materials such as genuine leather, metal finishes, and designer collaborations. Brands are launching limited-edition collections and partnering with fashion labels to attract style-conscious consumers. The premium segment is experiencing higher growth compared to basic silicone cases, driven by urban consumers willing to pay for exclusivity and aesthetics. Personalization features such as engraving, color customization, and themed designs are further enhancing product appeal, especially among younger demographics influenced by social media trends.

Integration of Functional Enhancements

Technological enhancements are becoming a defining trend in the market. Manufacturers are integrating additional functionalities such as built-in battery packs, wireless charging compatibility, anti-loss features, and antimicrobial coatings. These innovations are transforming protective cases into multifunctional accessories that enhance convenience and usability. The demand for rugged and waterproof designs is also increasing among consumers seeking durability for outdoor and travel use. This trend is particularly prominent in premium segments, where consumers expect added value beyond basic protection.

What are the key drivers in the AirPods protective case market?

Expansion of Wireless Earbud Ecosystem

The rapid growth in global shipments of true wireless stereo (TWS) devices is a primary driver of the AirPods protective case market. As consumers invest in premium earbuds, the need to protect these devices from damage becomes essential. The increasing replacement cycle of earbuds further supports recurring demand for cases, ensuring steady market growth.

Growing Demand for Personalization and Fashion Accessories

Consumers are increasingly using accessories to express personal style, driving demand for customized and visually appealing cases. Social media platforms and influencer marketing have amplified this trend, encouraging users to showcase unique designs and collections. This shift has expanded the market beyond utility-driven purchases to include fashion-oriented buying behavior.

What are the restraints for the global market?

Intense Price Competition and Market Fragmentation

The AirPods protective case market is highly fragmented, with numerous small manufacturers offering low-cost products. This creates intense price competition, particularly in the economy segment, leading to margin pressures for established brands. The low barrier to entry further intensifies competition, making differentiation challenging.

Dependence on AirPods Sales Cycle

The market is closely tied to the sales performance of AirPods and similar devices. Any slowdown in product innovation or sales can directly impact demand for protective cases. Seasonal fluctuations and product launch cycles also influence purchasing patterns, creating demand volatility.

What are the key opportunities in the AirPods protective case industry?

Expansion in Emerging Markets

Emerging economies such as India, Indonesia, and Brazil present significant growth opportunities due to rising disposable income and increasing adoption of wireless earbuds. Companies can leverage localized pricing strategies and regional e-commerce platforms to capture high-volume demand in these markets. Affordable yet durable cases are expected to gain traction among price-sensitive consumers.

Innovation in Multifunctional and Smart Cases

There is strong potential for integrating advanced features such as tracking compatibility, battery charging capabilities, and hygiene-focused coatings. These innovations can differentiate products and command premium pricing. Early adopters of such technologies are likely to gain a competitive advantage in an evolving market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 820 Million |

| Market Size in 2026 | USD 909.38 Million |

| Market Size in 2031 | USD 1525.47 Million |

| CAGR | 10.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Rugged and shockproof cases dominate the product type segment, accounting for approximately 27% of the global market share in 2025. These cases are preferred for their durability and ability to protect against drops and impacts, making them popular among frequent travelers and outdoor users. Slim-fit cases are also widely adopted due to their lightweight design and ease of use, while luxury designer cases are gaining traction in premium markets. Transparent cases remain popular for showcasing the original AirPods design, particularly among minimalist consumers.

Material Type Insights

Silicone cases continue to dominate the AirPods protective case market, accounting for approximately 32% of the total market share in 2025. This leadership position is primarily driven by their low production cost, high flexibility, lightweight nature, and strong shock-absorbing capabilities, making them ideal for mass-market adoption. The affordability of silicone cases aligns well with the largest consumer segment, mid-range buyers, while their availability in a wide variety of colors and designs supports personalization trends. Additionally, silicone’s ease of manufacturing allows brands to rapidly introduce new styles, contributing to faster inventory turnover and sustained demand.

Thermoplastic polyurethane (TPU) and hybrid material cases are gaining significant traction due to their superior durability, resistance to wear and tear, and enhanced grip. These materials cater to consumers seeking a balance between protection and aesthetics, particularly in the mid-to-premium price segments. Hybrid cases combining TPU with polycarbonate are increasingly preferred for rugged applications, offering dual-layer protection.

Leather cases, although representing a smaller share (approximately 12–15%), are a high-value segment driven by premiumization trends and consumer preference for luxury accessories. These cases often command higher margins due to craftsmanship and brand positioning. Meanwhile, metal and aluminum cases are emerging as niche offerings, particularly among premium and outdoor-focused consumers who prioritize durability and distinctive design, though their higher price points limit mass adoption.

Distribution Channel Insights

Online retail channels dominate the AirPods protective case market, contributing approximately 65% of total sales in 2025, making it the leading distribution segment globally. This dominance is driven by the rapid expansion of e-commerce ecosystems, increasing smartphone penetration, and consumer preference for convenience and competitive pricing. Platforms such as global marketplaces and direct-to-consumer (D2C) websites enable brands to showcase extensive product portfolios, leverage targeted digital marketing, and respond quickly to changing consumer preferences.

The leading position of online channels is further supported by shorter product life cycles in this market. Manufacturers can launch new designs, test demand, and scale production rapidly through digital platforms without the constraints of physical retail space. Additionally, user reviews, influencer endorsements, and social media integration significantly influence purchasing decisions, particularly among younger consumers.

Offline channels, including consumer electronics stores, mobile accessory outlets, and large-format retail chains, continue to play a complementary role. These channels are particularly relevant for impulse purchases and for consumers who prefer tactile product evaluation. However, their overall share is declining gradually due to higher operational costs and limited product variety compared to online platforms.

End-User Insights

Individual consumers represent the largest end-user segment, accounting for over 78% of the total market share in 2025. This segment’s dominance is driven by the widespread adoption of AirPods and similar wireless earbuds for personal use. The increasing replacement cycle of accessories, coupled with rising demand for multiple cases for different occasions (e.g., casual, travel, premium), further strengthens this segment’s growth. Personalization and lifestyle-driven purchasing behavior are key drivers, with consumers seeking cases that reflect their identity and preferences.

Corporate and promotional buyers are emerging as a high-potential segment, particularly for branded merchandise, employee gifting, and marketing campaigns. Companies are increasingly using customized AirPods cases as promotional tools due to their practical utility and visibility. This segment is witnessing steady growth, especially in developed markets where corporate gifting budgets are substantial.

Bulk buyers and resellers also contribute significantly to market volume, particularly in emerging economies. These players benefit from economies of scale and cater to local demand through offline retail networks and regional e-commerce platforms. The expansion of distribution networks in countries such as India and Southeast Asia is further supporting this segment’s growth.

Explore more data points, trends and opportunities Download Free Sample Report

AirPods Protective Case Market Segmentations

By Material Type

- Silicone Cases

- Thermoplastic Polyurethane (TPU) Cases

- Polycarbonate (PC) Hard Cases

- Leather Cases (Genuine & Synthetic)

- Hybrid Material Cases

- Metal/Aluminum Cases

By Product Type / Design

- Slim/Fit Cases

- Rugged/Shockproof Cases

- Waterproof/Weatherproof Cases

- Luxury/Designer Cases

- Transparent/Clear Cases

- Customizable/Personalized Cases

- Battery-Integrated Charging Cases

By Distribution Channel

- Online Retail

- Consumer Electronics Stores

- Mobile Accessories Stores

- Brand Retail Stores

- Hypermarkets/Supermarkets

By End-User

- Individual Consumers

- Corporate/Promotional Buyers

- Bulk Buyers & Resellers

By Price Range

- Economy (Below USD 10)

- Mid-Range (USD 10–25)

- Premium (Above USD 25)

Regional Insights

North America

North America remains the largest market, accounting for approximately 34% of the global share in 2025, with the United States contributing the majority of demand. The region’s leadership is driven by high penetration of premium wireless earbuds, strong consumer purchasing power, and a well-established ecosystem of accessory brands. A key growth driver in this region is the strong inclination toward premium and designer cases, supported by lifestyle-oriented consumption patterns. Additionally, the presence of leading brands and robust e-commerce infrastructure accelerates product availability and innovation. The U.S. market alone is estimated to exceed USD 220 million, with steady growth driven by frequent product upgrades and high accessory attachment rates.

Asia-Pacific

Asia-Pacific accounts for around 29% of the global market and is the fastest-growing region, with a CAGR exceeding 13%. China plays a dual role as both the largest manufacturing hub and a major exporter, supplying over 60% of global demand. India is emerging as a high-growth market, driven by rising disposable incomes, increasing smartphone and TWS adoption, and rapid expansion of e-commerce platforms. Southeast Asian countries such as Indonesia and Vietnam are also contributing to growth due to expanding middle-class populations. The primary driver in this region is volume growth fueled by affordability and rising consumer awareness, making it a key focus area for both global and regional players.

Europe

Europe holds approximately 21% of the global market share, led by key countries such as Germany, the United Kingdom, and France. The region’s growth is driven by premiumization and increasing demand for sustainable and eco-friendly products. European consumers show a strong preference for high-quality materials, including leather and recycled plastics, which supports higher average selling prices. Regulatory emphasis on sustainability and environmental standards is also encouraging manufacturers to innovate in biodegradable and recyclable materials, acting as a key growth driver in this region.

Middle East & Africa

The Middle East & Africa region accounts for approximately 8% of the global market, with the UAE and Saudi Arabia leading demand. Growth in this region is primarily driven by high disposable incomes, strong demand for premium electronics, and increasing urbanization. The popularity of luxury accessories and branded products is particularly high in Gulf countries, supporting demand for premium AirPods cases. Additionally, expanding retail infrastructure and growing e-commerce adoption are contributing to market growth, especially in urban centers.

Latin America

Latin America holds around 8% of the global market share, with Brazil and Mexico as the primary contributors. The region’s growth is driven by increasing smartphone penetration, rising adoption of wireless audio devices, and expanding digital commerce platforms. Price sensitivity remains a key factor, leading to strong demand for economy and mid-range cases. However, improving economic conditions and growing urban populations are gradually supporting the adoption of higher-value products. The expansion of regional distribution networks and cross-border e-commerce is further enhancing product accessibility, acting as a key growth driver in the region.