Air Circulator Fan Market Size

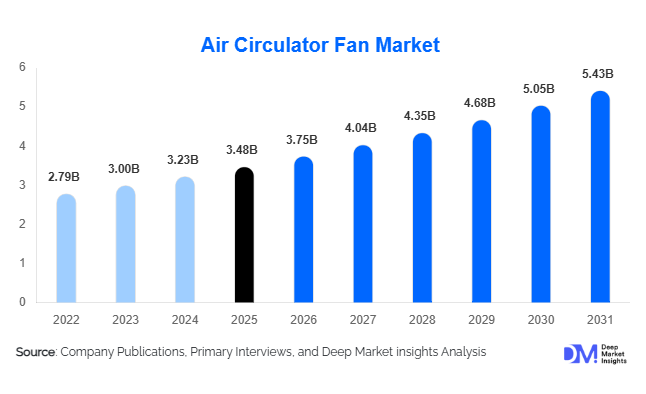

According to Deep Market Insights, the global air circulator fan market size was valued at USD 3.48 billion in 2025 and is projected to grow from USD 3.75 billion in 2026 to reach USD 5.43 billion by 2031, expanding at a CAGR of 7.7% during the forecast period (2026–2031). The air circulator fan market growth is primarily driven by increasing consumer demand for energy-efficient cooling appliances, rising awareness regarding indoor air quality management, and growing adoption of smart home technologies integrated with ventilation systems. Air circulator fans are increasingly being preferred over traditional fans due to their ability to optimize airflow distribution, improve HVAC efficiency, and reduce electricity consumption.

Growing urbanization, rising global temperatures, and the expansion of compact residential spaces are accelerating product adoption across residential and commercial sectors. Manufacturers are introducing technologically advanced solutions featuring brushless DC motors, IoT-enabled controls, voice assistant integration, bladeless designs, and silent operation capabilities. The increasing trend toward premium home appliances is also positively influencing market expansion, particularly in developed economies.

Asia-Pacific remains the dominant regional market due to large-scale manufacturing capabilities, rising middle-class income levels, and expanding household appliance penetration in countries such as China and India. Meanwhile, North America and Europe continue witnessing strong replacement demand driven by sustainability initiatives and energy efficiency regulations. Commercial applications across offices, warehouses, healthcare facilities, and hospitality infrastructure are also creating substantial demand for high-performance air circulation systems globally.

Key Market Insights

- Energy-efficient DC motor air circulators are rapidly replacing conventional AC motor models, driven by rising electricity costs and stricter energy-efficiency regulations globally.

- Smart air circulator fans integrated with Wi-Fi and voice assistants are witnessing strong premium demand, especially across North America, Japan, and Western Europe.

- Asia-Pacific dominates the global market, supported by strong manufacturing ecosystems, growing urban populations, and increasing appliance penetration.

- Residential applications account for the majority of global demand, fueled by urban apartment living and rising consumer focus on indoor comfort solutions.

- E-commerce and direct-to-consumer channels are reshaping product distribution, enabling brands to reach emerging markets more efficiently.

- Commercial and industrial ventilation optimization is emerging as a key growth area, particularly across warehouses, logistics hubs, hospitality, and healthcare infrastructure.

Air Circulator Fan Market Trends

Smart and Connected Air Circulators Gaining Popularity

The integration of smart technologies into air circulator fans is becoming a major market trend globally. Manufacturers are increasingly launching IoT-enabled products featuring smartphone app controls, Wi-Fi connectivity, AI-powered airflow adjustment, programmable timers, and compatibility with voice assistants such as Alexa and Google Assistant. Consumers are prioritizing connected home ecosystems that improve convenience and energy management. Premium smart air circulators are also incorporating environmental sensors capable of automatically adjusting airflow based on room temperature and occupancy levels. This trend is especially strong in developed markets where smart-home adoption rates continue expanding rapidly. Companies are additionally investing in software-driven energy optimization features that help consumers reduce electricity consumption while improving indoor air circulation efficiency.

Demand for Silent and Energy-Efficient Products Increasing

Consumers are increasingly demanding low-noise and energy-efficient air circulator fans suitable for bedrooms, home offices, healthcare environments, and educational facilities. Manufacturers are responding through the adoption of brushless DC motors, aerodynamic blade engineering, and inverter-based technologies that significantly reduce operational noise while improving airflow performance. Silent operation has become a critical purchasing factor in premium product categories. Simultaneously, energy-efficiency certifications and sustainability-focused purchasing decisions are accelerating demand for products that consume less electricity compared to traditional cooling appliances. Manufacturers are also focusing on recyclable materials and eco-friendly product designs to align with broader environmental sustainability trends and regulatory standards.

Air Circulator Fan Market Drivers

Growing Focus on Energy Conservation

Increasing awareness regarding energy efficiency and electricity cost optimization is one of the major drivers supporting air circulator fan market growth. Consumers and commercial building operators are increasingly using air circulators alongside HVAC systems to improve airflow distribution and reduce dependence on air conditioning systems. Air circulator fans consume substantially lower energy compared to air conditioners while enhancing thermal comfort and indoor ventilation. Governments across North America, Europe, and Asia are promoting energy-efficient appliances through energy labeling regulations and efficiency standards, further accelerating market adoption. Rising utility costs and sustainability goals are encouraging households and businesses to invest in circulation-based cooling solutions as cost-effective alternatives.

Rapid Urbanization and Residential Construction Growth

Rapid urbanization and increasing residential infrastructure development across emerging economies are significantly contributing to market expansion. Growing apartment living, smaller residential spaces, and higher appliance ownership rates are boosting demand for compact and portable air circulation solutions. Countries such as India, China, Indonesia, and Vietnam are witnessing rising disposable incomes and increasing penetration of household cooling appliances. Urban consumers are increasingly prioritizing indoor comfort, air movement optimization, and aesthetically designed home appliances, supporting demand for premium and multifunctional air circulators. Rising work-from-home trends have also increased demand for quiet and compact circulation systems suitable for home offices and personal environments.

Air Circulator Fan Market Restraints

Intense Price Competition and Market Fragmentation

The global air circulator fan market remains highly fragmented, with numerous international and regional manufacturers competing aggressively across price-sensitive segments. Low-cost producers, particularly in Asia-Pacific, continue exerting downward pressure on product pricing and operating margins. This intense pricing competition creates challenges for premium brands attempting to differentiate through technology and innovation. Smaller manufacturers often struggle to maintain profitability while investing in advanced motor technologies, smart connectivity features, and product differentiation strategies. Commoditization risks remain especially high within entry-level product categories.

Seasonal Demand Volatility

Demand for air circulator fans remains heavily influenced by seasonal weather conditions in several regions. Sales volumes typically increase during summer periods and decline significantly during colder months, creating inventory management and production planning challenges for manufacturers and distributors. Unpredictable climate conditions and temperature fluctuations can further impact annual sales cycles. Seasonal demand concentration also affects retail pricing strategies, promotional campaigns, and supply chain efficiency. Companies operating across multiple climatic regions are increasingly focusing on product diversification and export expansion to reduce dependency on seasonal domestic demand patterns.

Air Circulator Fan Market Opportunities

Expansion of Smart Home Ecosystems

The rapid global expansion of smart home ecosystems presents substantial opportunities for air circulator fan manufacturers. Consumers increasingly seek connected appliances that can integrate seamlessly with centralized home automation systems. Smart air circulators equipped with app-based controls, automated airflow adjustment, voice assistant compatibility, and energy monitoring capabilities are becoming attractive premium offerings. Manufacturers capable of combining advanced connectivity with energy efficiency and premium aesthetics are likely to capture higher-value market segments. The rising adoption of AI-enabled home appliances is expected to further accelerate innovation within the air circulation industry.

Growing Commercial and Industrial Ventilation Demand

Commercial and industrial facilities are increasingly adopting high-performance air circulator systems to improve ventilation efficiency, worker comfort, and HVAC optimization. Warehouses, logistics centers, manufacturing plants, hospitality facilities, and healthcare infrastructure are becoming major demand generators for industrial-grade circulation systems. The expansion of e-commerce fulfillment centers and large-scale commercial buildings is creating sustained opportunities for high-velocity airflow solutions. Companies are also integrating air circulation systems into smart building management platforms to improve energy efficiency and indoor climate control. These trends are expected to support long-term institutional demand globally.

Product Type Insights

Tabletop air circulator fans dominate the global market, accounting for nearly 28% of the overall revenue share in 2025. Their popularity is primarily driven by affordability, portability, and strong demand from urban residential consumers. Compact tabletop circulators are increasingly preferred for apartments, home offices, bedrooms, and personal workspaces where efficient airflow management is required without occupying significant space. Pedestal and tower air circulators are also witnessing strong growth due to rising consumer demand for premium home appliances with silent operation and aesthetic appeal. Bladeless tower circulators are gaining traction within premium product categories, particularly in North America and Europe, due to enhanced safety features, modern design, and smart connectivity integration. Meanwhile, industrial floor circulators continue experiencing growing adoption across warehouses, logistics centers, and manufacturing facilities requiring high-velocity airflow systems.

Technology Insights

DC motor-based air circulators account for the largest technology share globally, representing approximately 34% of market demand in 2025. Consumers increasingly prefer DC motor systems due to lower power consumption, quieter operation, and longer operational life compared to traditional AC motor alternatives. Smart IoT-enabled air circulators are among the fastest-growing segments, supported by rising smart-home adoption and connected appliance ecosystems. Manufacturers are integrating AI-based airflow optimization, voice assistant compatibility, and remote-control functionality into premium product offerings. Bladeless technology is also expanding rapidly within high-end residential applications, particularly among consumers prioritizing aesthetics, safety, and low-noise performance. HEPA-integrated air circulation systems are additionally gaining popularity in healthcare facilities and urban households concerned about indoor air quality and allergen management.

Distribution Channel Insights

Offline retail channels continue dominating the global air circulator fan market, accounting for nearly 58% of total sales in 2025. Consumers often prefer physical retail stores for appliance purchases due to product demonstrations, immediate availability, and after-sales support services. Electronics retailers, appliance showrooms, and hypermarkets remain major sales channels globally. However, online retail is rapidly emerging as the fastest-growing distribution channel due to increasing e-commerce penetration and direct-to-consumer brand strategies. Online platforms enable consumers to compare pricing, product specifications, customer reviews, and energy-efficiency ratings more efficiently. Manufacturers are increasingly investing in digital marketing campaigns, influencer partnerships, and direct e-commerce portals to strengthen online customer engagement and improve profit margins.

End-Use Insights

The residential segment dominates global demand, contributing approximately 61% of total market revenue in 2025. Rising urbanization, increasing household appliance penetration, and growing awareness regarding energy-efficient cooling solutions are driving residential adoption. Commercial applications are experiencing significant growth across offices, hotels, healthcare facilities, educational institutions, and retail spaces where air circulators help optimize HVAC performance and improve indoor comfort. Industrial demand is also expanding steadily due to rising investments in warehouses, manufacturing facilities, and logistics infrastructure requiring high-volume airflow management systems. Outdoor recreational applications such as camping, outdoor dining, sports events, and emergency preparedness are emerging as promising niche segments for portable rechargeable air circulators.

| By Product Type | By Technology | By End User | By Distribution Channel | By Airflow Capacity |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 24% of the global air circulator fan market, driven primarily by strong replacement demand and high smart-home penetration rates in the United States and Canada. Consumers increasingly prefer premium smart circulators featuring Wi-Fi connectivity, silent operation, and energy-efficient technologies. Commercial demand is also expanding across healthcare, hospitality, and office infrastructure where ventilation optimization and sustainability initiatives are becoming increasingly important. Growing awareness regarding indoor air quality and energy conservation continues supporting long-term market growth across the region.

Europe

Europe represents nearly 21% of global market demand, led by Germany, the United Kingdom, France, and Italy. Stringent energy-efficiency regulations and growing environmental awareness are accelerating adoption of advanced DC motor and low-noise circulation systems. Germany remains a major commercial and industrial demand center due to expanding warehouse automation and manufacturing infrastructure investments. Southern European countries are additionally experiencing rising demand due to increasing summer temperatures and climate-related cooling requirements. Consumers across Europe also demonstrate strong preference for sustainable and aesthetically designed appliances.

Asia-Pacific

Asia-Pacific dominates the global air circulator fan market with approximately 43% share in 2025. China remains the largest manufacturing and consumption hub globally due to its extensive appliance production ecosystem and growing domestic demand. India is among the fastest-growing markets, supported by rapid urbanization, rising disposable incomes, and increasing residential infrastructure development. Japan and South Korea continue witnessing strong demand for premium silent air circulators and smart-home integrated appliances. Expanding middle-class populations and increasing electrification rates across Southeast Asia are further accelerating regional market growth.

Latin America

Latin America is witnessing gradual market expansion led by Brazil and Mexico. Rising temperatures, growing urban populations, and increasing appliance affordability are supporting residential demand growth across the region. Mexico is also emerging as an important export-oriented manufacturing hub for North American appliance supply chains. Commercial infrastructure development and improving e-commerce penetration are additionally contributing to regional market expansion.

Middle East & Africa

The Middle East & Africa region is experiencing increasing demand due to extreme climatic conditions, rapid infrastructure development, and rising commercial construction activity. Gulf countries such as Saudi Arabia and the UAE are investing heavily in smart buildings, hospitality infrastructure, and commercial cooling optimization systems. Industrial airflow management demand is also rising across the manufacturing and logistics sectors. Africa represents an emerging market where growing urbanization and electrification are gradually improving household appliance penetration and consumer purchasing power.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Air Circulator Fan Market

- Vornado Air LLC

- Dyson Ltd.

- Midea Group

- Honeywell International Inc.

- Lasko Products LLC

- Panasonic Holdings Corporation

- SharkNinja, Inc.

- Toshiba Corporation

- Xiaomi Corporation

- IRIS Ohyama Inc.

- Rowenta

- Pelonis Technologies, Inc.

- Crompton Greaves Consumer Electricals Ltd.

- Orient Electric Limited

- Havells India Ltd.