Global Adult City & Urban Bicycle Helmets Market Size

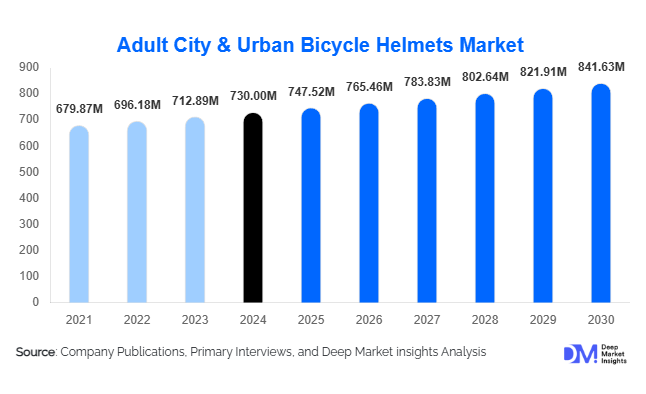

According to Deep Market Insights, the global Adult City & Urban Bicycle Helmets market size was valued at USD 2,480 million in 2025 and is projected to grow from USD 2,745.36 million in 2026 to reach USD 4,563.91 million by 2031, expanding at a CAGR of 10.7% during the forecast period (2026–2031). The market growth is strongly driven by rapid urban cycling adoption, expansion of e-bike usage, increasing government investments in cycling infrastructure, and rising consumer awareness regarding head safety and impact protection technologies in densely populated urban environments.

Key Market Insights

- Urban commuting is becoming a dominant mobility trend, with bicycles and e-bikes replacing short-distance motor vehicle travel in major cities.

- E-bike adoption is accelerating premium helmet demand, as higher speeds require advanced protection technologies such as MIPS and smart impact detection systems.

- Europe dominates the global market, supported by strong cycling culture, infrastructure, and strict safety regulations.

- Asia-Pacific is the fastest-growing region, driven by China and India’s expanding delivery ecosystems and urban mobility transitions.

- Smart helmets and connected safety devices are reshaping product innovation, integrating crash detection, GPS, lighting, and Bluetooth systems.

- Online retail channels are gaining strong momentum, driven by consumer preference for customization, price comparison, and direct-to-brand purchases.

What are the latest trends in the Adult City & Urban Bicycle Helmets market?

Smart and Connected Urban Helmets

One of the most significant trends is the rapid adoption of smart helmets integrated with IoT-based safety systems. These helmets include features such as crash detection sensors, automatic SOS alerts, integrated turn indicators, Bluetooth communication, and LED visibility systems. Urban commuters and e-bike users are increasingly adopting these products as they enhance real-time safety and connectivity. Companies are also developing app-based ecosystems that allow users to track cycling routes, monitor accident alerts, and share ride data. This trend is especially strong in technologically advanced markets such as Japan, Germany, South Korea, and the United States, where consumers prioritize digital mobility integration.

Premiumization and Lifestyle-Oriented Helmet Design

Urban helmets are increasingly evolving into lifestyle products rather than purely protective gear. Consumers now prefer helmets that combine aesthetics, lightweight construction, ventilation efficiency, and fashion compatibility with urban commuting wear. Premium materials such as carbon fiber and aerodynamic shell designs are gaining popularity among professional commuters and e-bike users. Brands are investing heavily in designer collaborations and customizable helmets to appeal to younger consumers, particularly millennials and Gen Z, who value personalization and style alongside safety performance. This shift is driving higher average selling prices and improving manufacturer margins globally.

What are the key drivers in the Adult City & Urban Bicycle Helmets market?

Rapid Expansion of Urban Cycling Infrastructure

Governments across Europe, North America, and Asia-Pacific are investing heavily in cycling infrastructure, including dedicated bike lanes, smart mobility corridors, and integrated public transport cycling systems. These initiatives are significantly increasing bicycle usage in urban areas, directly boosting helmet demand. Cities such as Amsterdam, Paris, Copenhagen, Shanghai, and Bengaluru are expanding cycling-friendly zones to reduce congestion and carbon emissions. This structural shift in urban mobility is one of the strongest long-term growth drivers for helmet adoption.

Strong Growth of E-Bike Adoption

The rising penetration of electric bicycles is significantly contributing to market expansion. E-bikes are increasingly used for commuting, delivery services, and urban mobility due to their speed and convenience. However, higher speeds increase accident risk, encouraging users to purchase advanced helmets with enhanced impact protection and smart safety features. This has led to strong demand for e-bike-specific helmets with extended coverage, ventilation systems, and integrated visibility enhancements.

Rising Safety Awareness and Regulatory Enforcement

Increasing awareness regarding head injuries and cyclist safety is driving widespread helmet adoption across urban populations. Governments and transport authorities are enforcing stricter helmet regulations, particularly for e-bike riders and delivery workers. Corporate fleets and gig economy platforms are also mandating helmet usage for riders, further boosting consistent demand. Public safety campaigns and insurance incentives are reinforcing helmet usage as a standard urban mobility practice.

What are the restraints for the global market?

High Cost of Advanced and Smart Helmets

One of the major restraints is the relatively high cost of technologically advanced helmets, particularly those with smart connectivity, MIPS protection systems, and premium composite materials. These products remain unaffordable for large segments of consumers in developing economies. Price sensitivity limits penetration in regions where cycling is still emerging as a primary transport mode, restricting mass adoption of premium helmet categories.

Presence of Low-Quality and Counterfeit Products

The market is also affected by the availability of uncertified and counterfeit helmets sold through online and unregulated channels. These products often fail to meet international safety standards, creating consumer trust issues and putting downward pressure on pricing for established brands. Inconsistent enforcement of safety regulations in some emerging markets further exacerbates this challenge.

What are the key opportunities in the Adult City & Urban Bicycle Helmets industry?

Growth in E-Bike and Gig Economy Delivery Segments

The rapid expansion of food delivery platforms, logistics services, and e-commerce-driven last-mile delivery is creating a large institutional demand base for urban helmets. Companies are increasingly mandating helmet usage for delivery personnel, generating consistent replacement cycles and bulk procurement opportunities. This segment is expected to be one of the fastest-growing contributors to market expansion globally.

Smart Mobility Integration and Digital Safety Ecosystems

The integration of helmets with smart mobility ecosystems presents a strong opportunity for innovation-led growth. Companies are developing connected platforms that integrate navigation, accident detection, ride analytics, and emergency communication features. Subscription-based safety services and app ecosystems are expected to generate recurring revenue streams, particularly in developed markets with high smartphone penetration.

Government-Led Sustainable Urban Transport Programs

Public investments in sustainable transport infrastructure, including cycling lanes, bike-sharing programs, and low-emission city initiatives, are creating strong demand for helmets. Governments are increasingly partnering with private operators to supply helmets for shared mobility fleets and public cycling systems. This institutional demand base provides long-term stability and volume growth opportunities for manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2480.00 Million |

| Market Size in 2026 | USD 2745.36 Million |

| Market Size in 2031 | USD 4563.91 Million |

| CAGR | 10.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global cycling helmet market is undergoing a significant transformation driven by rising urban mobility concerns, regulatory safety enforcement, and evolving consumer expectations around performance, comfort, and integrated technology. Within this landscape, commuter helmets continue to dominate the product type segment, accounting for approximately 31% market share. Their leadership is primarily attributed to the rapid expansion of daily urban cycling as a practical transportation mode in congested metropolitan regions. Increasing traffic congestion, rising fuel costs, and growing environmental awareness are encouraging commuters to adopt bicycles and e-bikes, thereby strengthening demand for helmets designed specifically for everyday use. Commuter helmets typically prioritize lightweight construction, ventilation, and integrated safety features, making them highly suitable for office-goers and short-distance riders who require both convenience and protection. The growth of cycling infrastructure in cities and government-backed “last-mile mobility” initiatives further reinforces this segment’s dominance.E-bike compatible helmets represent around 24% market share and are currently the fastest-growing product category. The primary growth driver is the rapid global adoption of electric bicycles and scooters, particularly in urban areas where shared mobility and micro-mobility ecosystems are expanding. E-bike riders typically travel at higher speeds than traditional cyclists, necessitating enhanced safety features such as extended coverage, impact-absorbing liners, and integrated lighting systems. Governments in several regions are also introducing regulations mandating higher safety standards for e-mobility users, further accelerating demand. The integration of smart features such as turn indicators, crash detection systems, and Bluetooth connectivity is making this segment highly attractive to tech-savvy consumers.

Application Insights

Daily urban commuting remains the dominant application segment, accounting for nearly 46% of global demand. The leading driver of this segment is the rapid urbanization of cities combined with worsening traffic congestion and increased awareness of sustainable transportation alternatives. Cycling is increasingly being integrated into urban mobility planning, with governments investing in dedicated bike lanes, cycling highways, and public bicycle-sharing systems. These developments are encouraging a large base of daily commuters to adopt helmets as essential safety equipment. Additionally, rising fuel prices and environmental concerns are pushing individuals to shift toward cycling for short-distance travel, further strengthening this segment.Recreational and fitness cycling is another steadily expanding application segment, driven by increasing global health consciousness and lifestyle-oriented fitness trends. Consumers are increasingly adopting cycling as part of wellness routines, supported by fitness tracking technologies and social cycling communities. The leading driver here is the growing awareness of preventive healthcare and the popularity of outdoor physical activities post-pandemic. Helmets in this segment often emphasize comfort, ventilation, and aesthetic design, catering to long-duration cycling enthusiasts.Tourism and campus mobility applications represent emerging niche segments contributing incremental demand. In tourism, cycling tours in scenic destinations are gaining traction, while universities and large campuses are increasingly promoting cycling as an eco-friendly mobility option. The key driver in these segments is institutional support for sustainable transport combined with growing interest in low-impact recreational travel experiences.

Distribution Channel Insights

Online retail dominates the distribution landscape with approximately 38% market share. The leading driver of this dominance is the rapid acceleration of e-commerce penetration and the growing preference for direct-to-consumer purchasing models. Online platforms provide consumers with extensive product variety, competitive pricing, and detailed product comparisons, which significantly influence purchasing decisions. Additionally, virtual fitting tools, augmented reality previews, and customer review systems have improved buyer confidence, especially for safety equipment like helmets. Brands are also increasingly investing in their own online storefronts, reducing reliance on intermediaries and improving profit margins.Specialty bicycle stores continue to play a critical role, particularly in premium helmet segments where proper fitting and expert consultation are essential. The leading driver for this channel is the need for personalized service, as consumers often require professional guidance when selecting advanced helmets with safety technologies or custom fit systems. These stores also serve as experience centers where customers can physically test products before purchase, enhancing trust and brand loyalty.Offline retail channels, including sporting goods stores and general mobility outlets, remain important in emerging economies. The leading driver here is the continued dominance of traditional retail infrastructure in regions where digital penetration is still developing. These channels offer affordability, immediate product availability, and localized brand presence, making them crucial for mass-market adoption.

End-User Insights

Individual consumers constitute the largest end-user segment, driven by widespread urban cycling adoption and growing awareness of road safety. The leading driver is the increasing integration of cycling into daily lifestyles, particularly in urban environments where cycling offers an efficient alternative to motorized transport. Consumers are also becoming more safety-conscious due to government campaigns and rising accident awareness.Delivery and logistics riders represent the fastest-growing end-user segment due to the exponential expansion of food delivery, courier services, and last-mile logistics platforms. The leading driver is the gig economy model, which relies heavily on large fleets of independent riders who require mandatory safety equipment. High turnover rates and continuous onboarding of new riders further accelerate helmet demand in this category.Government and municipal programs are increasingly investing in cycling infrastructure and shared mobility systems, leading to large-scale procurement of helmets for bike-sharing fleets. The leading driver is the global push toward sustainable urban transport policies aimed at reducing carbon emissions and traffic congestion. Institutional procurement ensures bulk demand and long-term contracts, contributing significantly to market stability.Corporate mobility initiatives are also emerging as an important end-user segment. Companies are integrating cycling into employee wellness programs and ESG (Environmental, Social, Governance) strategies. The leading driver is corporate sustainability commitments combined with health-focused workplace initiatives that encourage employees to adopt active transportation methods.

Explore more data points, trends and opportunities Download Free Sample Report

Adult City & Urban Bicycle Helmets Market Segmentations

By Product Type

- Commuter Bicycle Helmets

- Urban Lifestyle Helmets

- Smart Connected Helmets

- Folding & Compact Helmets

- E-Bike Specific Helmets

- Premium & Designer Helmets

- Multi-Sport Urban Helmets

- High-Visibility & Reflective Helmets

- Modular Helmets with Visors

- Integrated Lighting Helmets

By Safety Technology

- Standard EPS Foam Helmets

- MIPS Technology Helmets

- WaveCel Technology Helmets

- Koroyd Protection Helmets

- Rotational Impact Protection Helmets

- Smart Sensor Integrated Helmets

- Crash Detection Enabled Helmets

- AI-Based Safety Helmets

By Distribution Channel

- Online Retail

- Specialty Bicycle Stores

- Sporting Goods Retailers

- Hypermarkets & Supermarkets

- Urban Mobility Stores

- Department Stores

- Bike-Sharing Fleet Procurement Channels

Regional Insights

Europe

Europe holds approximately 37% of the global market share, making it the most mature and dominant regional market. The leading growth driver in Europe is the continent’s well-established cycling culture combined with extensive cycling infrastructure and strong regulatory safety frameworks. Countries such as the Netherlands, Germany, France, and the United Kingdom have deeply integrated cycling into urban mobility systems, supported by dedicated cycling lanes, parking systems, and public awareness campaigns. The rapid expansion of e-bike adoption across Europe is further boosting demand for advanced helmets, particularly those with integrated safety technologies and enhanced comfort features. Environmental sustainability policies under the European Green Deal are also encouraging citizens to adopt cycling over motorized transport, strengthening long-term market stability.

Asia-Pacific

Asia-Pacific accounts for approximately 31% market share and is the fastest-growing region globally. The leading driver is rapid urbanization combined with increasing population density in major cities, which is creating severe traffic congestion and pushing consumers toward cycling and e-mobility solutions. China dominates both production and consumption, while India is witnessing explosive growth driven by gig economy expansion and affordable mobility solutions. In Japan and South Korea, high consumer preference for technologically advanced and premium helmets is driving demand for smart safety features. Government initiatives promoting clean transportation and investments in cycling infrastructure are further accelerating regional growth.

North America

North America contributes approximately 22% of global market share, with the United States leading demand. The key growth driver in this region is the rising adoption of cycling as both a recreational and commuting activity, particularly in urban centers such as New York, Portland, and San Francisco. The increasing popularity of e-bikes and micro-mobility solutions is significantly expanding helmet demand. Additionally, growing awareness of head injury prevention and stricter safety regulations in certain states are encouraging the adoption of advanced helmets with integrated safety technologies. Corporate wellness programs and outdoor fitness culture are also supporting long-term market growth.

Latin America

Latin America represents an emerging market with strong growth potential, particularly in countries such as Brazil and Mexico. The leading driver is the increasing reliance on bicycles for affordable transportation in densely populated urban areas where public transport systems are overloaded. Expansion of delivery services and gig economy platforms is also contributing to rising helmet adoption. However, price sensitivity remains a key challenge, influencing demand for low-cost and mid-range helmets. Government investments in urban mobility improvements are expected to gradually support market expansion.

Middle East & Africa

The Middle East & Africa region is in an early development stage but is witnessing gradual growth, particularly in urban centers such as Dubai, Riyadh, and Cape Town. The leading driver is the emergence of smart city initiatives and diversification efforts aimed at reducing dependency on oil-based economies. Investments in recreational cycling infrastructure, tourism-driven cycling activities, and urban mobility planning are creating new demand pockets. Although the market is still relatively small, increasing awareness of cycling safety and gradual infrastructure development are expected to support long-term expansion.

Key Players in the Adult City & Urban Bicycle Helmets Market

- Vista Outdoor

- Giro Sport Design

- Trek Bicycle Corporation

- Specialized Bicycle Components

- MET-Helmets

- ABUS

- KASK

- POC Sports

- Lazer Sport

- Scott Sports

- Thousand

- Livall

- Nutcase Helmets

- Uvex Sports

- Bern Unlimited