Global Action Cameras Market Size

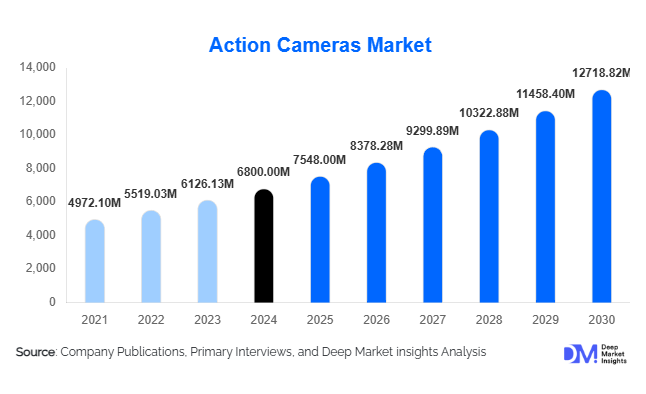

According to Deep Market Insights, the global action cameras market size was valued at USD 6,800 million in 2025 and is projected to grow from USD 7,548 million in 2026 to reach USD 12,718.82 million by 2031, expanding at a CAGR of 11% during the forecast period (2026–2031). The market growth is primarily driven by the rapid expansion of digital content creation, rising adventure tourism activities, increasing adoption of 4K/5K video technologies, and strong demand from sports, travel, and professional vlogging communities. Growing integration of AI-based stabilization, cloud connectivity, and wearable camera ecosystems is further strengthening global adoption across consumer and enterprise segments.

Key Market Insights

- Content creator economy is the primary growth engine, with vloggers, influencers, and streamers driving premium camera demand globally.

- 4K action cameras dominate the market due to rising demand for high-definition, cinematic-quality content across social media platforms.

- North America leads global demand, driven by high disposable income and strong outdoor recreation culture.

- Asia-Pacific is the fastest-growing region, supported by rising tourism, affordable product penetration, and expanding digital creator base.

- Online retail channels dominate distribution, accounting for majority of global sales due to influencer-driven purchasing behavior.

- Industrial and enterprise adoption is increasing, especially in construction, law enforcement, and inspection applications.

What are the latest trends in the global action cameras market?

AI-Powered Imaging and Smart Connectivity

Action cameras are increasingly integrating AI-based stabilization, object tracking, voice control, and automated editing tools. Cloud connectivity and mobile app ecosystems allow instant editing and sharing, making cameras more aligned with digital-first content creation workflows. This trend is particularly strong among professional vloggers and sports broadcasters who require seamless content production pipelines.

Rise of 360-Degree and Immersive Video Content

Demand for immersive content is accelerating adoption of 360-degree action cameras, especially in travel, gaming, and virtual reality applications. These devices allow users to capture fully interactive environments, enabling new experiences in sports broadcasting, tourism marketing, and digital storytelling. Integration with VR platforms and drone systems is further expanding their usage scope.

What are the key drivers in the global action cameras market?

Expansion of Creator Economy and Social Media Monetization

The rapid growth of platforms such as YouTube, Instagram, and TikTok has transformed content creation into a full-time profession for millions of users. Action cameras offer portability, durability, and high-quality video capture, making them essential tools for vloggers, travel creators, and athletes. Increasing monetization opportunities are driving continuous upgrades and repeat purchases.

Growth in Adventure Tourism and Outdoor Activities

Rising participation in cycling, skiing, diving, surfing, and motorsports is fueling demand for rugged, waterproof, and mountable cameras. Governments promoting tourism infrastructure development are indirectly supporting this growth. Consumers increasingly prefer devices capable of capturing extreme sports experiences in high resolution and challenging environments.

Technological Advancements in Imaging Systems

Continuous innovation in sensor technology, battery efficiency, image stabilization, and ultra-wide-angle lenses is significantly enhancing product performance. Features such as 5K recording, HDR imaging, and AI-enhanced video processing are becoming standard, improving user experience and driving premium product adoption.

What are the restraints for the global market?

Competition from Smartphone Cameras

Advanced smartphones with high-resolution sensors, stabilization systems, and waterproof capabilities are reducing the need for standalone action cameras among casual users. This substitution effect is particularly strong in entry-level segments, limiting market expansion potential.

Pricing Pressure and Market Commoditization

Increasing competition from low-cost manufacturers, especially in Asia, has led to declining average selling prices. While premium brands maintain strong margins through ecosystem-based offerings, mid-range and budget segments face profitability challenges due to intense price competition.

What are the key opportunities in the global action cameras industry?

Enterprise and Industrial Adoption

Action cameras are increasingly used in construction, mining, logistics, and law enforcement for safety documentation, inspection, and training purposes. Demand for rugged, AI-enabled enterprise-grade cameras presents a strong growth opportunity beyond consumer applications.

Expansion in Emerging Markets

Rising disposable income and growing digital content consumption in countries such as India, Indonesia, Vietnam, and Brazil are creating strong demand for affordable mid-range action cameras. E-commerce penetration is making these products more accessible to new consumer bases.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6800 Million |

| Market Size in 2026 | USD 7548 Million |

| Market Size in 2031 | USD 12718.82 Million |

| CAGR | 11% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global action camera market continues to evolve rapidly, with product innovation, sensor advancement, and connectivity features shaping consumer preferences across all major categories. Box-style action cameras remain the dominant product format, accounting for approximately 42% share of the overall market. This dominance is primarily attributed to their rugged form factor, superior heat dissipation, modular mounting capabilities, and compatibility with a wide range of accessories that support both amateur and professional use cases. These devices are widely preferred in extreme sports environments where durability and stability are critical performance parameters. The leading segment driver for box-style cameras is the increasing demand for versatile, mountable, and impact-resistant recording devices that can perform reliably under high-motion and high-vibration conditions, particularly in motorsports, cycling, skiing, and marine environments.Mid-range action cameras account for nearly 39% share of the global market, occupying a critical position between entry-level affordability and professional-grade performance. This segment benefits from balanced specifications, including decent image stabilization, water resistance, and 4K recording capabilities at accessible price points. The leading segment driver for mid-range devices is the expanding middle-income consumer base in emerging economies, where users seek value-oriented products that deliver strong performance without the premium cost associated with flagship models. This category continues to serve as the backbone of mass-market adoption globally.

Application Insights

Application diversity is one of the most significant growth accelerators in the action camera market, with sports and adventure activities representing the largest segment, accounting for approximately 36% market share. This dominance is strongly linked to the global rise in outdoor recreational activities, including cycling, skiing, surfing, mountain climbing, and motorsports. The leading segment driver for sports and adventure applications is the increasing consumer preference for experiential documentation, where individuals seek to capture immersive, first-person perspectives of high-intensity physical activities for both personal memory preservation and digital sharing.Other applications such as travel documentation, industrial inspection, law enforcement, and underwater exploration are also contributing meaningfully to market expansion. In industrial and enterprise environments, action cameras are increasingly used for remote inspection, safety monitoring, and operational documentation in hazardous or hard-to-reach locations. The leading segment driver for enterprise applications is the growing emphasis on operational efficiency and real-time visual data collection in sectors such as construction, manufacturing, and utilities. Underwater applications are gaining traction as well, supported by improved waterproofing standards and advancements in imaging clarity under low-light aquatic conditions.

Distribution Channel Insights

Distribution dynamics in the action camera market are undergoing a structural transformation, with online retail channels dominating global sales at approximately 58% share. The rapid growth of e-commerce platforms has fundamentally reshaped consumer purchasing behavior, enabling users to compare specifications, read reviews, and access competitive pricing with ease. Influencer marketing and digital advertising also play a critical role in driving online conversions, particularly among younger demographics. The leading segment driver for online channels is the convenience of direct-to-consumer purchasing combined with global product accessibility and fast delivery infrastructure.Brand-owned websites are also gaining increasing traction as manufacturers adopt integrated ecosystem strategies that combine hardware, software, and subscription-based services. These platforms allow companies to build direct relationships with customers, offer firmware updates, and provide cloud storage solutions. The leading segment driver for brand-owned digital channels is ecosystem consolidation, where manufacturers seek to retain customers within a unified digital and hardware environment to enhance lifetime value and recurring revenue streams.

End-User Insights

Individual consumers represent the largest end-user category, accounting for approximately 54% of total market demand. This segment is primarily driven by recreational users who utilize action cameras for travel documentation, sports activities, and personal content creation. The leading segment driver for individual consumers is lifestyle-driven digital expression, where capturing and sharing experiences has become an integral part of social identity and online engagement behavior.Professional content creators represent the fastest-growing end-user segment, supported by the expansion of influencer marketing, freelance videography, and independent media production. These users demand high-performance devices capable of delivering cinematic-quality output with advanced stabilization and editing flexibility. The leading segment driver for professional creators is income diversification through digital platforms, where content quality directly influences monetization potential and audience growth.Enterprise and institutional users, including media organizations, sports associations, law enforcement agencies, and industrial operators, are increasingly adopting rugged wearable camera systems for operational and strategic applications. In these environments, action cameras are used for live broadcasting, tactical documentation, safety monitoring, and training purposes. The leading segment driver for enterprise adoption is the need for real-time visual intelligence, which enhances decision-making, transparency, and operational accountability across complex workflows.

Explore more data points, trends and opportunities Download Free Sample Report

Action Cameras Market Segmentations

By Product Type

- Box-Style Action Cameras

- Cube-Style Action Cameras

- Bullet-Style Action Cameras

- 360-Degree Action Cameras

- Modular Action Cameras

- Wearable Clip-On Action Cameras

- Rugged Outdoor Action Cameras

- Waterproof Action Cameras

- Mini/Compact Action Cameras

- Professional Cinematic Action Cameras

By Resolution

- HD (720p)

- Full HD (1080p)

- 2.7K

- 4K

- 5K and Above

By Application

- Sports & Adventure

- Travel & Tourism

- Vlogging & Content Creation

- Commercial Filmmaking

- Law Enforcement & Security

- Industrial Inspection

- Marine & Underwater Activities

- Drone Integration

- Wildlife & Nature Recording

- Education & Training

By End User

- Individual Consumers

- Professional Content Creators

- Sports Professionals

- Media & Entertainment Companies

- Industrial & Commercial Enterprises

- Defense & Law Enforcement Agencies

Regional Insights

North America

North America holds approximately 34% of global market share, making it the most mature and technologically advanced regional market for action cameras. The United States serves as the primary growth engine due to its strong outdoor recreation culture, high disposable income levels, and early adoption of advanced imaging technologies. The region also benefits from a highly developed content creation ecosystem supported by social media platforms, professional videography networks, and sports broadcasting industries. A key regional growth driver is the integration of action cameras into mainstream digital storytelling, where users increasingly document both everyday experiences and extreme sports activities. The presence of leading manufacturers such as :contentReference[oaicite:0]{index=0} further strengthens innovation cycles, driving continuous improvements in stabilization, resolution, and software integration.

Europe

Europe accounts for nearly 24% of the global market share, supported by a strong tradition of adventure tourism, cycling culture, and winter sports participation. Countries such as Germany, the United Kingdom, France, Italy, and Spain represent key demand centers where consumers actively engage in outdoor recreational activities. The regional market is characterized by a growing preference for sustainable and high-performance imaging devices, with consumers increasingly valuing energy efficiency, durability, and long product lifecycles. The leading regional growth driver in Europe is the expansion of eco-tourism and experiential travel, where travelers prioritize immersive documentation of cultural and natural landscapes. Additionally, regulatory emphasis on product quality and safety standards has encouraged manufacturers to develop more robust and environmentally conscious designs.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, driven by rapid digitalization, rising disposable incomes, and the explosive growth of social media usage. Countries such as China, India, Japan, and South Korea are at the forefront of this expansion. India, in particular, is emerging as one of the fastest-growing action camera markets globally due to the rapid expansion of the creator economy, increased affordability of devices, and widespread smartphone penetration. The leading regional growth driver is the democratization of digital content creation, where millions of new users are entering video-based platforms and adopting action cameras as essential tools for storytelling, travel documentation, and entrepreneurial content production. Additionally, the expansion of tourism infrastructure and adventure sports industries is further accelerating demand.

Latin America

Latin America is witnessing steady growth, led by Brazil and Mexico, where increasing social media engagement and rising interest in adventure tourism are driving demand for action cameras. The region benefits from a vibrant influencer culture and expanding e-commerce penetration, which makes advanced imaging devices more accessible to middle-income consumers. The leading regional growth driver is the rise of digital entertainment consumption and mobile-first content creation, where users increasingly rely on video platforms for both income generation and personal expression. Additionally, sports enthusiasm, particularly in football and outdoor recreational activities, continues to support sustained adoption across urban and semi-urban populations.

Middle East & Africa

The Middle East & Africa region is experiencing gradual but steady growth, supported by tourism diversification strategies in countries such as the United Arab Emirates and Saudi Arabia. These nations are heavily investing in entertainment, luxury tourism, and adventure travel infrastructure, which is increasing demand for high-quality imaging devices. In Africa, countries such as South Africa and Kenya are seeing rising adoption driven by safari tourism and wildlife documentation activities. The leading regional growth driver is tourism-led digital transformation, where governments and private enterprises are actively promoting experiential travel and visual storytelling as part of broader economic diversification strategies. Additionally, rising disposable incomes in urban centers are contributing to increased penetration of mid-range and premium action cameras across the region.

Key Players in the Global Action Cameras Market

- GoPro Inc.

- DJI

- Sony Group Corporation

- Insta360

- Akaso

- Canon Inc.

- Nikon Corporation

- Garmin Ltd.

- Panasonic Holdings Corporation

- Xiaomi Corporation