3D Scanners Market Size

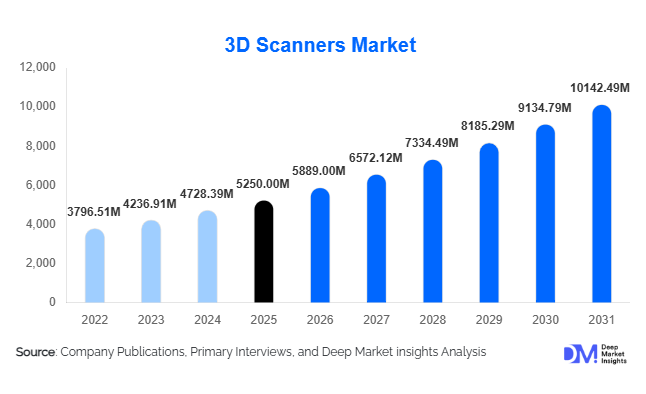

According to Deep Market Insights, the global 3D scanners market size was valued at USD 5,250 million in 2025 and is projected to grow from USD 5,859.00 million in 2026 to reach USD 10,142.49 million by 2031, expanding at a CAGR of 11.6% during the forecast period (2026–2031). The 3D scanners market growth is primarily driven by increasing adoption of Industry 4.0 practices, rising demand for precision engineering across manufacturing, automotive, and aerospace industries, and the rapid proliferation of portable and handheld scanning solutions enabling real-time data capture in diverse applications.

Key Market Insights

- Laser 3D scanners and portable devices are dominating the market globally, due to their high accuracy and versatility for industrial, healthcare, and AEC applications.

- Integration with AI, cloud platforms, and digital twin technologies is enhancing the capabilities of 3D scanning solutions, making them critical for predictive maintenance, quality inspection, and real-time data processing.

- North America leads in adoption, driven by the aerospace and automotive industries in the U.S. and Canada, accounting for roughly 34% of the 2025 market share.

- Europe is a major growth hub, with Germany and France driving high demand in automotive and manufacturing applications, representing about 29% of the global market in 2025.

- Asia-Pacific is emerging as the fastest-growing region, led by China and Japan, driven by industrial modernization, government initiatives, and rising adoption in SMEs.

- Healthcare and AR/VR applications are opening new opportunities for 3D scanning, especially in prosthetics, dental, and immersive virtual environment creation.

What are the latest trends in the 3D scanners market?

Integration with Digital Twin and Smart Manufacturing

3D scanners are increasingly being integrated with digital twin ecosystems and Industry 4.0 initiatives. This allows manufacturers to create precise virtual replicas of physical assets, enabling predictive maintenance, real-time monitoring, and optimization of production workflows. Integration with cloud-based platforms ensures seamless sharing and analysis of large 3D datasets, improving operational efficiency and reducing downtime. Companies are leveraging AI-driven analytics to detect anomalies and simulate performance, positioning 3D scanners as essential tools in automated and smart manufacturing environments.

Expansion of Portable and Handheld Scanners

Portable and handheld 3D scanners are becoming widely adopted due to their flexibility and usability in field environments such as construction sites, heritage preservation, and medical imaging. Compact form factors and wireless connectivity enable on-site scanning and rapid data transfer. This trend is particularly attractive to small and medium enterprises that require precision measurement without high infrastructure costs. Enhanced battery life, faster scanning speeds, and intuitive interfaces are further driving adoption across diverse industries.

What are the key drivers in the 3D scanners market?

Rising Adoption of Industry 4.0

Manufacturers are increasingly integrating 3D scanners into production lines for automated quality inspection, reverse engineering, and predictive maintenance. This trend reduces defects, ensures compliance with precision standards, and optimizes operational efficiency. Industry 4.0 adoption is especially strong in the automotive and aerospace sectors, where digital transformation is critical for competitive advantage.

Demand for Precision and Customization

High-resolution scanning is essential for sectors requiring customized components, such as healthcare (prosthetics, dental applications) and automotive (lightweight, precision-engineered parts). The growing emphasis on bespoke manufacturing drives the adoption of medium-to-high precision scanners, allowing industries to meet strict quality and regulatory requirements while reducing production costs.

Technological Advancements in Scanners

Recent developments in laser, structured light, and photogrammetry-based scanning technologies have improved speed, accuracy, and versatility. Enhanced software capabilities, including AI-driven post-processing, cloud-based data storage, and real-time analytics, are making scanners more valuable and user-friendly, expanding their appeal across multiple industries.

What are the restraints for the global market?

High Initial Costs

Advanced 3D scanning systems, particularly high-precision models, involve significant capital investment, restricting adoption among SMEs and cost-sensitive industries. While entry-level solutions are becoming more affordable, high-end hardware remains a barrier for broader market penetration.

Complex Data Processing and Integration

Handling large volumes of 3D data requires specialized software and trained personnel. Integration with existing enterprise systems, CAD/CAM tools, and quality control workflows can be challenging and resource-intensive. These operational complexities may slow adoption and increase costs for end-users.

What are the key opportunities in the 3D scanners market?

Emerging Healthcare Applications

The healthcare sector presents high-growth opportunities, particularly for patient-specific prosthetics, dental scanning, and surgical planning. Integration with CAD/CAM workflows and medical imaging enhances treatment precision and reduces production timelines. Increasing healthcare digitization and rising demand for personalized medicine create a favorable environment for 3D scanner adoption.

Expansion into Emerging Markets

Asia-Pacific and Latin America are emerging as high-potential regions due to rapid industrialization, infrastructure development, and government-supported manufacturing initiatives. Affordable and modular 3D scanning solutions tailored to SMEs can unlock significant market potential in these regions.

AR/VR and Metaverse Applications

The demand for high-resolution 3D models in gaming, media, and virtual environments is driving new use cases. 3D scanners that efficiently capture realistic textures and geometries can support immersive digital experiences, positioning them as essential tools in content creation and simulation-driven industries.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5250 Million |

| Market Size in 2026 | USD 5889 Million |

| Market Size in 2031 | USD 10142.49 Million |

| CAGR | 11.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Hardware continues to dominate the 3D scanners market, accounting for approximately 55% of global demand in 2025, primarily driven by the widespread adoption of high-performance laser and structured light scanners across industrial applications. Laser scanners, in particular, lead this segment due to their superior accuracy, ability to capture complex geometries, and effectiveness in large-scale environments such as automotive assembly lines and construction sites. The dominance of hardware is further supported by increasing capital investments in smart manufacturing and quality inspection infrastructure.

However, the software segment is emerging as the fastest-growing component, fueled by the integration of 3D scanning data with AI-driven analytics, cloud computing, and digital twin ecosystems. Advanced software solutions are enabling real-time data processing, automated defect detection, and seamless integration with CAD/CAM platforms, significantly enhancing the value proposition of scanning systems. Meanwhile, services, including calibration, maintenance, training, and data processing, play a critical enabling role, particularly in high-precision industries such as aerospace and healthcare, where system reliability and compliance with stringent standards are essential. The growing complexity of scanning workflows is also driving demand for managed services and subscription-based software models.

Application Insights

Quality inspection and metrology lead the application segment, accounting for nearly 34% of the global market in 2025. This leadership is driven by increasing demand for precision manufacturing, stringent regulatory standards, and the need for real-time defect detection in high-value industries such as automotive, aerospace, and electronics. The shift toward automated inspection systems and in-line quality control is further reinforcing the dominance of this segment. Reverse engineering and rapid prototyping are also witnessing strong growth, particularly as companies accelerate product development cycles and reduce time-to-market. 3D scanners enable accurate replication of legacy components and facilitate design optimization, making them indispensable in manufacturing and industrial design. Additionally, cultural heritage digitization is gaining traction, with governments and institutions using 3D scanning to preserve artifacts and historical sites.

Emerging applications in healthcare and AR/VR are significantly expanding the market scope. In healthcare, 3D scanning is being widely adopted for prosthetics, orthotics, dental imaging, and surgical planning, driven by the trend toward personalized medicine. In parallel, the rapid growth of immersive technologies is fueling demand for high-resolution 3D models in gaming, simulation, and virtual environments, positioning these applications as key future growth drivers.

Distribution Channel Insights

Direct sales remain the dominant distribution channel, particularly for high-value and industrial-grade 3D scanners, as they enable manufacturers to offer customized solutions, technical consultation, installation support, and training services. This channel is preferred by large enterprises that require tailored solutions and long-term service agreements. Distributors and channel partners play a crucial role in expanding market reach, especially among small and medium enterprises (SMEs) and in emerging markets. These intermediaries provide localized support, after-sales services, and easier access to mid-range and entry-level products, making them essential for market penetration.

Meanwhile, online sales channels are gaining traction, particularly for portable and desktop scanners. The increasing digitalization of procurement processes, availability of virtual product demonstrations, and transparent pricing models are encouraging customers to adopt e-commerce platforms. Manufacturers are also investing in direct-to-customer (D2C) digital strategies, integrating interactive tools, AR-based demos, and subscription-based purchasing models, which are reshaping the buying experience and broadening customer access.

End-Use Insights

The automotive industry remains the largest end-use segment, accounting for approximately 27% of global demand in 2025. This dominance is driven by the extensive use of 3D scanners in design validation, dimensional inspection, and production optimization. The transition toward electric vehicles (EVs), lightweight materials, and complex component geometries is further accelerating demand for high-precision scanning solutions. The aerospace sector is another major contributor, leveraging 3D scanning for maintenance, repair, and overhaul (MRO), as well as for ensuring compliance with strict safety and quality standards. Meanwhile, healthcare is the fastest-growing end-use segment, with a CAGR of approximately 13%, driven by increasing adoption in prosthetics, dental applications, and surgical planning. The push toward personalized and patient-specific solutions is significantly boosting demand in this sector.

The architecture, engineering, and construction (AEC) industry is also witnessing strong growth due to the adoption of Building Information Modeling (BIM) and digital twin technologies. 3D scanners are being used for site mapping, structural analysis, and renovation projects. Additionally, export-driven demand from industrial hubs such as Germany, China, and Japan continues to play a vital role, as these countries emphasize precision manufacturing and technological innovation.

Explore more data points, trends and opportunities Download Free Sample Report

3D Scanners Market Segmentations

By Product Type

- Laser 3D Scanners

- Structured Light 3D Scanners

- Optical/White Light Scanners

- Photogrammetry-Based Scanners

- Contact 3D Scanners

By Application

- Quality Inspection & Metrology

- Reverse Engineering

- Rapid Prototyping

- Digital Twin & Virtual Simulation

- Healthcare & Medical Applications

- Cultural Heritage Preservation

By Distribution Channel

- Direct Sales

- Distributors & Channel Partners

- Online Sales Platforms

Regional Insights

North America

North America dominates the 3D scanners market, accounting for approximately 34% of global demand in 2025, with the United States contributing the majority share. The region’s leadership is driven by strong adoption in aerospace, automotive, and advanced manufacturing sectors. High levels of R&D investment, early adoption of Industry 4.0 technologies, and the presence of leading market players further support growth. Additionally, increasing demand for digital twin solutions and smart factory implementations is accelerating adoption. Government support for innovation, along with a robust ecosystem of technology providers, continues to reinforce North America’s market position.

Europe

Europe holds around 29% of the global market, led by Germany, France, and the United Kingdom. The region’s growth is primarily driven by its strong industrial base, particularly in automotive and precision engineering. Germany, as a manufacturing powerhouse, is a key contributor, with extensive use of 3D scanners in quality control and production processes. Stringent regulatory standards and a focus on product quality are major drivers of adoption. Furthermore, increasing investments in smart manufacturing, sustainability initiatives, and digital transformation programs are supporting long-term growth. The region’s emphasis on innovation and advanced engineering continues to create sustained demand for high-precision scanning technologies.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at a CAGR of approximately 13%, and accounts for about 27% of the global market. China and Japan are the primary growth engines, with China benefiting from large-scale industrialization and government initiatives such as “Made in China 2026,” which promote advanced manufacturing technologies. Japan’s focus on precision engineering and robotics further supports demand. India is emerging as a key market, driven by growth in healthcare, construction, and manufacturing sectors, supported by initiatives like “Make in India.” The rapid expansion of SMEs, increasing automation, and rising demand for cost-effective scanning solutions are key drivers of regional growth.

Latin America

Latin America represents approximately 5% of the global market, with Brazil and Mexico being the leading contributors. Growth in the region is driven by expanding automotive manufacturing, industrial modernization, and increasing foreign investments. Rising awareness of advanced manufacturing technologies and the gradual adoption of automation are supporting market expansion. Infrastructure development and government initiatives to boost industrial output are also contributing to demand, although economic volatility remains a challenge.

Middle East & Africa

The Middle East & Africa region accounts for around 5% of the market, with key growth observed in the UAE, Saudi Arabia, and South Africa. The adoption of 3D scanning technologies is being driven by large-scale infrastructure projects, smart city initiatives, and increasing focus on industrial diversification. Government-led programs aimed at reducing dependence on oil revenues and promoting advanced manufacturing are significant growth drivers. In Africa, gradual industrialization and infrastructure development are supporting adoption, while increasing investments in construction and energy sectors are creating new opportunities for 3D scanning applications.

Key Players in the 3D Scanners Market

- Hexagon AB

- FARO Technologies

- Nikon Corporation

- Trimble Inc.

- Carl Zeiss AG

- Topcon Corporation

- Creaform (AMETEK)

- Artec 3D

- Shining 3D

- 3D Systems Corporation

- Perceptron Inc.

- Leica Geosystems

- Konica Minolta

- Basis Software

- Maptek