3D Printed Lighting Market Size

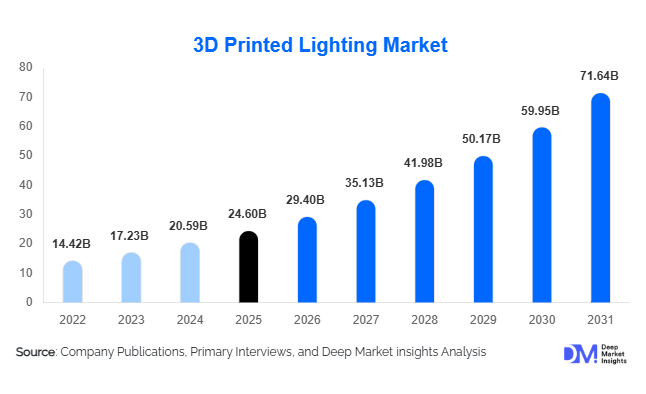

According to Deep Market Insights, the global 3D printed lighting market size was valued at USD 24.6 billion in 2025 and is projected to grow from USD 29.40 billion in 2026 to reach USD 71.64 billion by 2031, expanding at a CAGR of 19.5% during the forecast period (2026–2031). The market growth is primarily driven by rising adoption of customized lighting fixtures, increasing integration of additive manufacturing technologies in interior décor, growing demand for sustainable lighting systems, and expanding investments in smart buildings and architectural lighting applications.

Key Market Insights

- 3D printed lighting is rapidly transitioning from niche designer applications to mainstream architectural and commercial adoption, supported by advances in additive manufacturing scalability and material innovation.

- LED-integrated printed lighting fixtures dominate global demand, owing to their energy efficiency, low heat generation, and compatibility with intricate customized designs.

- Europe dominates the global market, driven by strong designer lighting industries, sustainability regulations, and widespread adoption of premium interior décor products.

- Asia-Pacific remains the fastest-growing regional market, supported by rapid urbanization, smart city projects, and expanding additive manufacturing infrastructure in China and India.

- Hospitality, luxury residential, and commercial office applications are accelerating demand, as businesses increasingly prioritize visually differentiated and customizable lighting solutions.

- AI-assisted generative design and sustainable printable materials are transforming product innovation, enabling lightweight, recyclable, and highly complex lighting structures.

3D Printed Lighting Market Trends

Growing Adoption of Sustainable and Recyclable Lighting Solutions

Sustainability has become one of the most important trends shaping the 3D printed lighting market. Manufacturers are increasingly shifting toward recyclable polymers, biodegradable materials, and low-waste additive manufacturing processes to align with global ESG mandates and green building standards. Compared to conventional manufacturing, additive production minimizes material wastage while enabling localized production that reduces transportation-related emissions. Luxury hospitality projects, commercial buildings, and environmentally conscious residential consumers are increasingly demanding eco-friendly decorative lighting systems. Many companies are also incorporating bio-based filaments and circular economy manufacturing models into their operations. This sustainability-focused transition is particularly strong across Europe and North America, where environmental regulations and green infrastructure initiatives continue to accelerate demand for sustainable lighting products.

Smart and AI-Integrated Lighting Designs Expanding Rapidly

The integration of smart technologies with 3D printed lighting systems is emerging as a major market trend. Companies are increasingly combining IoT-enabled lighting controls, voice-assisted automation, AI-powered generative design software, and connected LED systems to create multifunctional lighting solutions. AI-assisted design tools allow manufacturers and architects to produce highly intricate parametric lighting geometries optimized for aesthetics, energy efficiency, and structural durability. Smart lighting systems compatible with home automation ecosystems are witnessing strong demand across luxury residential and commercial office environments. Cloud-connected lighting systems capable of adaptive brightness control, occupancy sensing, and remote management are also becoming more common in hospitality and infrastructure projects. These technological advancements are significantly expanding the commercial viability of 3D printed lighting products globally.

3D Printed Lighting Market Drivers

Rising Demand for Customized and Designer Lighting Fixtures

The increasing global preference for personalized interior décor and architecturally distinctive spaces is significantly driving demand for 3D printed lighting solutions. Traditional manufacturing methods often struggle to economically produce low-volume customized designs, whereas additive manufacturing enables rapid prototyping and complex geometries without expensive tooling costs. Architects, interior designers, hospitality operators, and luxury residential developers are increasingly adopting 3D printed fixtures to create unique visual experiences. The ability to manufacture bespoke designs with shorter lead times and lower inventory requirements is making additive manufacturing highly attractive within premium lighting applications.

Expansion of Smart Buildings and Sustainable Infrastructure

The rapid growth of smart buildings and sustainable urban infrastructure projects is creating strong long-term demand for advanced lighting systems. Governments and commercial developers are investing heavily in energy-efficient buildings equipped with intelligent lighting controls and IoT-enabled infrastructure. 3D printed lighting systems integrated with LEDs and smart automation technologies align well with these evolving construction requirements. Public infrastructure modernization projects across Asia-Pacific, Europe, and the Middle East are increasingly utilizing customized architectural lighting systems that support both energy efficiency and modern design aesthetics.

3D Printed Lighting Market Restraints

High Production Costs for Industrial Additive Manufacturing

Despite strong growth potential, industrial-scale additive manufacturing remains relatively expensive compared to conventional mass production methods. High costs associated with industrial 3D printers, advanced printing materials, post-processing systems, and precision manufacturing continue to limit adoption in price-sensitive market segments. While 3D printing is highly cost-effective for customization and limited production runs, traditional molding and large-scale manufacturing still offer lower costs for standardized lighting products. This pricing gap remains a key challenge for broader mainstream adoption.

Regulatory and Product Standardization Challenges

The market also faces challenges related to product certification, electrical safety compliance, and quality standardization. Commercial and industrial lighting products must comply with strict thermal, durability, fire-resistance, and electrical safety regulations. Many regions still lack uniform standards specifically addressing additive-manufactured lighting systems, creating certification complexities for manufacturers. Inconsistent product quality and limited awareness among traditional procurement channels can further slow adoption, particularly within infrastructure and industrial applications.

3D Printed Lighting Market Opportunities

Growth in Smart City and Commercial Infrastructure Projects

Global smart city development initiatives are creating significant opportunities for 3D printed lighting manufacturers. Governments across Asia-Pacific, Europe, and the Middle East are investing heavily in intelligent urban infrastructure, including energy-efficient street lighting, smart commercial buildings, airports, and public spaces. 3D printing allows manufacturers to develop lightweight, modular, and architecturally customized lighting systems suited for large-scale infrastructure applications. Demand for IoT-enabled lighting integrated with smart controls and sensor technologies is expected to create substantial long-term growth opportunities for market participants.

Luxury Hospitality and Premium Residential Expansion

The rapid expansion of luxury hospitality projects and premium residential developments presents another major growth opportunity. Hotels, resorts, luxury apartments, and high-end retail spaces increasingly prioritize visually distinctive interior environments to enhance customer experience and brand positioning. 3D printed lighting allows designers to create highly customized fixtures that are difficult to replicate through conventional manufacturing. Premium hospitality operators are also adopting sustainable and designer-focused lighting concepts, creating strong demand for additive-manufactured decorative lighting systems.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 24.6 Billion |

| Market Size in 2026 | USD 29.40 Billion |

| Market Size in 2031 | USD 71.64 Billion |

| CAGR | 19.50% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Pendant lights dominate the global 3D printed lighting market, accounting for nearly 24% of total market revenue in 2025. Their popularity is driven by extensive usage across luxury residential projects, restaurants, hotels, retail stores, and modern office environments where aesthetic appeal plays a critical role. Pendant lighting designs produced through additive manufacturing allow highly complex geometries, lightweight structures, and artistic customization that traditional manufacturing processes cannot easily achieve. Table lamps and wall-mounted decorative fixtures are also witnessing strong demand due to increasing consumer preference for personalized home décor products. Ceiling-mounted modular lighting systems are gaining adoption in commercial infrastructure projects, while outdoor and landscape lighting applications are gradually expanding alongside smart city developments and sustainable urban infrastructure investments.

Application Insights

Commercial lighting remains the largest application segment, representing approximately 37% of the global market in 2025. Hotels, restaurants, luxury retail stores, commercial office spaces, and experiential environments are increasingly utilizing customized 3D printed fixtures to enhance interior aesthetics and customer engagement. Residential applications are also expanding rapidly, particularly within premium urban housing projects and smart homes where consumers seek visually differentiated and energy-efficient lighting systems. Architectural and infrastructure lighting applications are gaining momentum as governments and developers invest in smart buildings and public infrastructure modernization. Entertainment venues, museums, galleries, and event installations are emerging as niche but high-value applications due to growing demand for immersive lighting experiences.

Distribution Channel Insights

Direct sales remain the dominant distribution channel in the 3D printed lighting market, particularly for large commercial projects requiring collaborative customization and project-specific lighting solutions. Architectural firms, hospitality developers, and interior designers often work directly with manufacturers to create tailor-made lighting systems optimized for unique spatial requirements. Online retail channels are expanding rapidly as consumers increasingly purchase decorative and customizable lighting products through digital platforms. Several manufacturers are investing in interactive online configurators that allow customers to personalize shapes, materials, and finishes before purchase. Specialty lighting stores and design studios also continue to play an important role, particularly within premium designer lighting categories and luxury interior décor markets.

End User Insights

Interior designers and architects represent one of the fastest-growing end-user segments in the market. Additive manufacturing technologies enable designers to create highly intricate parametric lighting structures and project-specific installations with significantly reduced design constraints. Hospitality operators are also major adopters due to increasing investments in premium guest experiences and differentiated interior branding strategies. Luxury residential developers continue to drive strong demand for personalized decorative lighting products integrated with smart home systems. Corporate offices are increasingly adopting energy-efficient and aesthetically modern lighting systems as part of sustainable workplace transformation initiatives. Public infrastructure agencies are gradually incorporating 3D printed architectural lighting into smart city projects, airports, and urban redevelopment programs.

Material Type Insights

Plastics and polymers account for approximately 46% of the global 3D printed lighting market, making them the leading material category. Materials such as PLA, ABS, PETG, nylon, and polycarbonate are widely utilized because they offer lightweight structures, cost efficiency, flexibility, and compatibility with multiple additive manufacturing technologies. Bio-based and recyclable polymers are witnessing particularly strong growth as sustainability becomes a core purchasing criterion among both commercial and residential consumers. Metal-based 3D printed lighting systems are also gaining traction in premium architectural applications where durability, industrial aesthetics, and high structural strength are required. Composite materials reinforced with carbon fiber and glass-filled polymers are increasingly being adopted for advanced commercial installations requiring enhanced performance characteristics.

Explore more data points, trends and opportunities Download Free Sample Report

3D Printed Lighting Market Segmentations

By Product Type

- Pendant Lights

- Table Lamps

- Floor Lamps

- Wall Lights

- Ceiling Lights

- Outdoor & Landscape Lighting

- Specialty & Customized Lighting

By Printing Technology

- FDM (Fused Deposition Modeling)

- SLA (Stereolithography)

- SLS (Selective Laser Sintering)

- DLP (Digital Light Processing)

- MJF (Multi Jet Fusion)

- DMLS (Direct Metal Laser Sintering)

By Application

- Residential Lighting

- Commercial Lighting

- Industrial Lighting

- Architectural & Infrastructure Lighting

- Automotive & Transportation Lighting

- Healthcare & Institutional Lighting

- Entertainment & Event Lighting

By Distribution Channel

- Direct Sales (B2B)

- Online Retail

- Specialty Lighting Stores

- Interior Design & Architectural Firms

- B2B Industrial Procurement Platforms

Regional Insights

North America

North America accounts for nearly 29% of the global 3D printed lighting market in 2025, driven primarily by strong demand from the United States. The region benefits from advanced additive manufacturing infrastructure, high smart home penetration, and strong consumer spending on luxury interior décor products. Commercial office modernization, hospitality investments, and sustainable building initiatives continue to support market growth across the U.S. and Canada. Demand for smart LED-integrated lighting systems and customized designer fixtures remains particularly strong within urban metropolitan areas.

Europe

Europe remains the largest regional market, accounting for approximately 34% of global market revenue in 2025. Germany, Italy, France, the United Kingdom, and the Netherlands are key contributors due to strong designer lighting industries, sustainable architecture initiatives, and advanced manufacturing ecosystems. Italy remains a global center for premium decorative lighting and luxury interior products, while Germany leads in industrial additive manufacturing innovation. The region’s emphasis on sustainability and energy-efficient construction continues to accelerate adoption of recyclable and bio-based printed lighting systems.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market and is expected to register a CAGR exceeding 22% during the forecast period. China dominates regional production capacity due to its large-scale additive manufacturing infrastructure and expanding construction industry. India is witnessing rapid growth driven by smart city investments, increasing hospitality projects, and government-backed manufacturing initiatives such as “Make in India.” Japan and South Korea continue investing heavily in precision manufacturing, smart lighting systems, and IoT-enabled infrastructure. Rising urbanization and growing middle-class demand for premium home décor are further accelerating regional market expansion.

Latin America

Latin America represents a relatively smaller but steadily growing market for 3D printed lighting. Brazil and Mexico are the leading contributors due to increasing urban infrastructure investments, hospitality development, and retail modernization projects. Adoption remains concentrated within premium commercial and luxury residential applications, although increasing awareness of additive manufacturing technologies is gradually expanding the addressable market across the region.

Middle East & Africa

The Middle East & Africa region is witnessing increasing adoption of 3D printed lighting solutions, particularly within luxury hospitality, commercial infrastructure, and smart city projects. The UAE and Saudi Arabia are major growth centers due to large-scale tourism investments, futuristic urban development programs, and high demand for premium architectural lighting systems. Smart city initiatives such as NEOM are accelerating adoption of sustainable and technologically advanced lighting products. South Africa also represents an emerging market driven by commercial real estate modernization and hospitality sector expansion.

Key Players in the 3D Printed Lighting Market

- Signify N.V.

- Stratasys Ltd.

- 3D Systems Corporation

- Materialise NV

- EOS GmbH

- HP Inc.

- Desktop Metal Inc.

- Carbon Inc.

- Acuity Brands Inc.

- Zumtobel Group AG

- Formlabs Inc.

- GE Additive

- Voxeljet AG

- Proto Labs Inc.

- Philips Lighting Solutions