3D Mouse Market Size

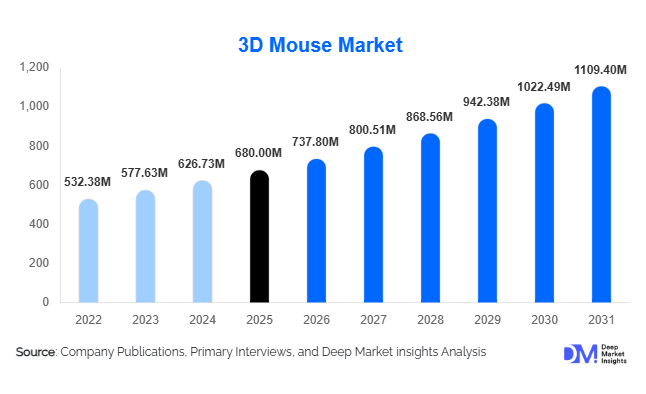

According to Deep Market Insights, the global 3D mouse market size was valued at USD 680 million in 2025 and is projected to grow from USD 737.80 million in 2026 to reach USD 1,109.40 million by 2031, expanding at a CAGR of 8.5% during the forecast period (2026–2031). The 3D mouse market growth is primarily driven by increasing adoption of CAD, BIM, and simulation tools across industries such as manufacturing, architecture, and healthcare, along with rising demand for intuitive human-machine interfaces in digital environments.

Key Market Insights

- Wireless 3D mice dominate the market, accounting for over 58% share due to demand for flexible and mobile work environments.

- CAD and 3D modeling applications lead adoption, contributing nearly 46% of total market demand globally.

- North America holds the largest market share, supported by advanced manufacturing and strong software ecosystem integration.

- Asia-Pacific is the fastest-growing region, driven by industrialization and government-backed manufacturing initiatives.

- Manufacturing and automotive sectors remain the largest end-users, contributing around 34% of overall demand.

- Integration with VR/AR and digital twin technologies is emerging as a key trend reshaping product innovation and adoption.

What are the latest trends in the 3D mouse market?

Integration with Immersive Technologies

The 3D mouse market is increasingly aligning with immersive technologies such as virtual reality (VR) and augmented reality (AR). As industries adopt digital twins and simulation-based workflows, 3D mice are evolving into spatial controllers that enable seamless navigation within virtual environments. This trend is particularly evident in sectors like automotive design, aerospace engineering, and gaming development, where real-time 3D manipulation is critical. Manufacturers are focusing on enhancing compatibility with VR platforms, enabling users to interact more naturally within immersive workspaces. This integration is expanding the use cases of 3D mice beyond traditional CAD environments into training simulations, collaborative design reviews, and metaverse-related applications.

Shift Toward Wireless and Ergonomic Designs

There is a strong shift toward wireless and ergonomically optimized 3D mice. Professionals increasingly prefer clutter-free workspaces and devices that reduce physical strain during prolonged usage. Wireless 3D mice with Bluetooth and RF connectivity are gaining traction, particularly among remote and hybrid workers. At the same time, ergonomic innovations such as improved grip design, customizable buttons, and adaptive sensitivity settings are enhancing user comfort and productivity. This trend is driving repeat purchases and strengthening brand loyalty, especially among professional designers and engineers who rely heavily on precision tools.

What are the key drivers in the 3D mouse market?

Rising Adoption of CAD, BIM, and Simulation Tools

The widespread adoption of CAD, BIM, and simulation tools across industries is a primary driver of the 3D mouse market. These tools require precise navigation within complex 3D environments, which traditional input devices cannot efficiently provide. 3D mice enhance workflow efficiency by enabling simultaneous pan, zoom, and rotate functions, significantly reducing design time and improving accuracy. As industries such as construction, automotive, and aerospace continue to digitize their design processes, the demand for advanced input devices is increasing.

Growth of Industry 4.0 and Digital Twins

The rise of Industry 4.0 and digital twin technologies is accelerating demand for 3D mice. Manufacturers are increasingly relying on virtual models for real-time monitoring, predictive maintenance, and simulation-based decision-making. These applications require intuitive navigation tools, making 3D mice an essential component of modern industrial workflows. The growing investment in smart manufacturing and automation is expected to sustain this demand over the forecast period.

What are the restraints for the global market?

High Cost Compared to Conventional Input Devices

One of the major restraints in the 3D mouse market is the relatively high cost of these devices compared to standard mice. While they offer significant productivity benefits, their premium pricing can limit adoption among small businesses, freelancers, and price-sensitive markets. This cost barrier is particularly evident in developing regions where budget constraints influence purchasing decisions.

Learning Curve and User Adaptation Challenges

Another key challenge is the learning curve associated with 3D mouse usage. Unlike traditional input devices, 3D mice require users to adapt to multi-axis navigation, which may initially reduce productivity. Organizations often need to invest in training programs to ensure effective utilization, which can slow down adoption, especially in industries resistant to workflow changes.

What are the key opportunities in the 3D mouse industry?

Expansion into Emerging Markets

Emerging economies such as India, China, and Brazil present significant growth opportunities for the 3D mouse market. Rapid industrialization, infrastructure development, and increasing adoption of digital design tools are driving demand in these regions. Government initiatives promoting domestic manufacturing and digital transformation are further supporting market expansion. Companies that offer cost-effective solutions and establish strong distribution networks in these markets can capture substantial growth opportunities.

Product Diversification for Education and Freelancers

The growing number of students, independent designers, and freelance professionals represents a large untapped market. Developing entry-level and mid-range 3D mice tailored to this segment can significantly expand the customer base. Educational institutions are increasingly incorporating CAD and 3D modeling into their curricula, creating long-term demand for affordable input devices. This trend is expected to drive volume growth in the coming years.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 680 Million |

| Market Size in 2026 | USD 737.80 Million |

| Market Size in 2031 | USD 1109.40 Million |

| CAGR | 8.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Wireless 3D mice dominate the global market, accounting for approximately 58% of total revenue in 2025, and this leadership is expected to strengthen further over the forecast period. The primary driver behind this dominance is the rapid shift toward hybrid and remote work environments, where mobility, flexibility, and workspace optimization are critical. Wireless devices eliminate cable constraints, enabling seamless workstation setups and improved user ergonomics. Additionally, advancements in Bluetooth Low Energy (BLE), multi-device pairing, and extended battery life have significantly enhanced performance reliability, addressing earlier concerns around latency and connectivity.

Another key driver is the increasing use of collaborative and cloud-based design platforms, where professionals frequently switch between devices and locations. Wireless 3D mice support this dynamic workflow, making them the preferred choice among architects, designers, and engineers. Meanwhile, wired 3D mice continue to maintain relevance in industrial and mission-critical environments, where uninterrupted connectivity and precision are essential, such as in manufacturing control rooms and high-end simulation labs. However, ongoing improvements in wireless stability and security protocols are gradually narrowing this gap, positioning wireless devices as the long-term standard across both commercial and industrial applications.

Application Insights

3D modeling and CAD design remain the leading application segment, contributing approximately 46% of the global market in 2025. This dominance is primarily driven by the global expansion of digital design workflows across industries such as architecture, engineering, automotive, and aerospace. The increasing adoption of Building Information Modeling (BIM), parametric design tools, and simulation software has created a strong need for precise and intuitive navigation devices, making 3D mice indispensable in professional environments. A key growth driver for this segment is the rising complexity of design projects, which requires efficient manipulation of multi-dimensional models. 3D mice significantly reduce design time and improve accuracy, thereby enhancing productivity. In parallel, the media and entertainment segment is witnessing rapid growth, fueled by increasing demand for high-quality animation, visual effects (VFX), and gaming content. The proliferation of streaming platforms and immersive content formats is further accelerating adoption in this segment.

Emerging applications such as healthcare imaging, surgical planning, and industrial automation are also gaining traction. In healthcare, 3D mice enable more intuitive navigation of complex imaging datasets, while in industrial automation, they support real-time control of robotic systems and simulation environments. These expanding use cases are expected to diversify the application landscape and contribute to sustained market growth.

Distribution Channel Insights

Direct enterprise sales dominate the distribution landscape, accounting for approximately 52% of total market revenue in 2025. This leadership is driven by the procurement preferences of large organizations, which prioritize bulk purchasing, product customization, and integrated support services. Enterprises often require tailored solutions that align with specific software ecosystems and workflow requirements, making direct engagement with manufacturers the most efficient channel. A major driver for this segment is the increasing adoption of 3D mice in large-scale industrial and infrastructure projects, where standardized deployment across teams is essential. Direct sales also facilitate long-term service agreements, training programs, and software integration, enhancing overall customer value.

Meanwhile, online retail channels are experiencing rapid growth, particularly among freelancers, small businesses, and educational institutions. The convenience of online purchasing, coupled with competitive pricing and product comparisons, is driving adoption in this segment. Additionally, specialized distributors continue to play a critical role in catering to niche markets, providing technical expertise and bridging the gap between manufacturers and end-users in specialized industries.

End-Use Industry Insights

The manufacturing and automotive sector leads the market, accounting for approximately 34% of total demand in 2025. This dominance is driven by the extensive use of computer-aided design (CAD), simulation, prototyping, and digital twin technologies in product development processes. The transition toward electric vehicles (EVs), autonomous systems, and advanced manufacturing techniques is further accelerating demand for precision input devices such as 3D mice. The architecture, engineering, and construction (AEC) sector is another major contributor, supported by the rapid adoption of BIM technologies and increasing global infrastructure investments. Governments worldwide are investing heavily in smart cities and large-scale construction projects, creating strong demand for advanced design tools.

The media and entertainment industry is the fastest-growing end-use segment, driven by the expansion of gaming, animation, and digital content creation. The rise of immersive media, including VR and AR content, is further boosting demand for intuitive 3D navigation devices. Additionally, the healthcare sector is emerging as a high-potential segment, particularly in radiology, medical imaging, and surgical planning. The growing use of 3D visualization in diagnostics and treatment planning is expected to drive long-term adoption in this industry.

Explore more data points, trends and opportunities Download Free Sample Report

3D Mouse Market Segmentations

By Product Type

- Wired 3D Mouse

- Wireless 3D Mouse

By Application

- 3D Modeling & CAD Design

- Media & Entertainment

- Healthcare Imaging & Surgical Planning

- Industrial Automation & Robotics Control

- Geospatial & Oil/Gas Visualization

- Education & Research

By Distribution Channel

- Direct Enterprise Sales

- Online Retail

- Specialized IT & Design Equipment Distributors

By End-Use Industry

- Manufacturing & Automotive

- Architecture, Engineering & Construction (AEC)

- Healthcare

- Media & Entertainment

- Energy & Utilities

- Academic & Research Institutions

Regional Insights

North America

North America holds the largest share of the global 3D mouse market, accounting for approximately 38% in 2025, with the United States being the primary contributor. The region’s dominance is driven by early adoption of advanced design technologies, strong presence of CAD software providers, and high investment in Industry 4.0 initiatives. The widespread implementation of digital twin technologies, automation, and smart manufacturing is a key growth driver. Additionally, the presence of a large base of professional designers, engineers, and content creators further strengthens demand. The region also benefits from high enterprise spending on productivity-enhancing tools and a mature IT infrastructure, supporting continued market expansion.

Europe

Europe accounts for approximately 27% of the global market, with Germany, the UK, and France as major contributors. Germany leads the region due to its strong automotive and industrial manufacturing base, where precision engineering and advanced simulation tools are widely used. The UK and France are driven by robust demand from the AEC and media sectors. A key growth driver in Europe is the region’s emphasis on innovation, sustainability, and digital transformation, supported by government initiatives promoting smart manufacturing and green construction. Additionally, the adoption of Industry 4.0 technologies across European industries continues to fuel demand for advanced input devices.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a projected CAGR exceeding 10% during the forecast period. China and India are the primary growth engines, driven by rapid industrialization, infrastructure development, and increasing adoption of digital design tools. Government initiatives such as “Made in China 2026” and “Make in India” are accelerating the adoption of advanced manufacturing technologies, directly boosting demand for 3D mice. Japan and South Korea also contribute significantly due to their technological sophistication and strong electronics and automotive industries. Additionally, the growing number of engineering graduates and the expanding design outsourcing industry in the region are key drivers of market growth.

Latin America

Latin America is experiencing steady growth, with Brazil and Mexico leading regional demand. The market is driven by expanding manufacturing activities, increasing foreign investments, and the gradual adoption of digital design technologies. The automotive and construction sectors are key contributors, supported by infrastructure development projects. While the market remains relatively smaller compared to other regions, improving economic conditions and rising awareness of advanced design tools are expected to drive future growth.

Middle East & Africa

The Middle East and Africa region is emerging as a promising market, led by the UAE and Saudi Arabia. Growth in this region is driven by significant investments in smart cities, infrastructure development, and digital construction technologies. Government-led initiatives aimed at economic diversification, such as Saudi Arabia’s Vision 2031, are promoting the adoption of advanced design and engineering tools. Additionally, increasing focus on industrial development and modernization is expected to create new opportunities for 3D mouse adoption. While the market is still in its early stages, strong investment momentum and technological adoption are likely to support long-term growth.