Sulfur Dioxide in Food Market Size

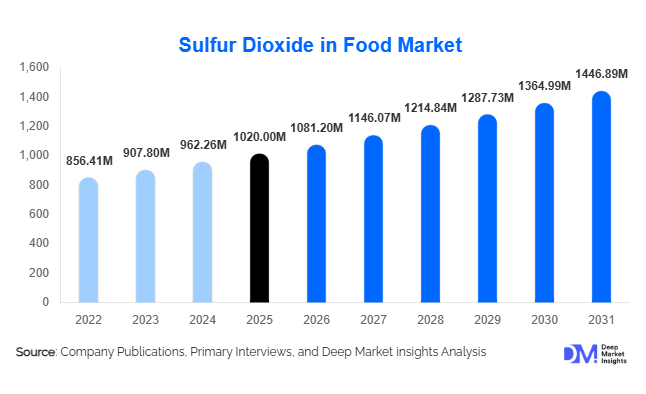

According to Deep Market Insights, the global sulfur dioxide in food market size was valued at USD 1020 million in 2025 and is projected to grow from USD 1081.20 million in 2026 to reach USD 1446.89 million by 2031, expanding at a CAGR of 6.0% during the forecast period (2026–2031). Growth in the sulfur dioxide in food market is primarily driven by rising global consumption of processed foods, increasing export-oriented food production, and the continued reliance on sulfur dioxide as a cost-effective and technically efficient preservative across multiple food categories.

Key Market Insights

- Sulfur dioxide remains a critical preservative for dried fruits, wine, and fruit concentrates due to its superior antimicrobial and antioxidant properties.

- Solid sulfite derivatives dominate global consumption owing to ease of storage, precise dosing, and regulatory compliance advantages.

- Asia-Pacific leads global demand, supported by large-scale food processing industries in China and India.

- Europe remains a regulation-driven market, with strict residue limits shaping controlled and technology-enabled usage.

- Beverage manufacturing is the fastest-growing end-use segment, particularly in wine and fruit-based alcoholic beverages.

- Technological improvements in low-residue and controlled-release sulfites are expanding adoption in highly regulated markets.

What are the latest trends in the sulfur dioxide in food market?

Shift Toward Controlled-Residue Sulfite Applications

Food manufacturers are increasingly adopting controlled-residue and precision-dosing technologies to comply with tightening regulatory standards while retaining preservation efficacy. Encapsulated sulfites and automated dosing systems are reducing excess sulfur dioxide usage, particularly in Europe and North America. This trend is improving consumer safety perception and enabling continued use of sulfur dioxide in premium food products, including organic-compliant dried fruits and specialty beverages.

Rising Demand from Export-Oriented Food Processing

Global food exports are rising steadily, with dried fruits, juices, and processed vegetables forming a significant share of cross-border trade. Sulfur dioxide remains essential for maintaining product quality during long transit periods. Export-focused processors in Asia-Pacific, Latin America, and Africa are increasing procurement volumes, positioning sulfur dioxide as a backbone input for international food trade.

What are the key drivers in the sulfur dioxide in food market?

Expansion of Processed and Packaged Food Consumption

Urbanization and changing dietary patterns are accelerating demand for processed and shelf-stable foods. Sulfur dioxide provides cost-effective microbial control and oxidation prevention, making it a preferred preservative for high-volume food production. Its multifunctional role reduces the need for multiple additives, supporting widespread adoption among industrial food processors.

Strong Growth in Global Beverage Production

Wine, fruit juice concentrates, and fermented beverages rely heavily on sulfur dioxide for stabilization and quality control. Rising beverage consumption in Asia-Pacific and Latin America, along with new winery and juice processing capacity additions, is driving sustained sulfur dioxide demand across the beverage value chain.

What are the restraints for the global market?

Stringent Regulatory and Labeling Requirements

Regulatory agencies in Europe and North America impose strict maximum residue limits and mandatory allergen labeling for sulfites. Compliance increases operational costs and restricts usage volumes, particularly for manufacturers serving premium and health-conscious consumer segments.

Growing Preference for Clean-Label Alternatives

Consumers are increasingly seeking additive-free and “clean-label” foods, prompting manufacturers to reduce sulfite usage where technically feasible. While alternatives often lack comparable efficacy, this trend acts as a long-term restraint on sulfur dioxide demand growth.

What are the key opportunities in the sulfur dioxide in food industry?

Growth of Emerging Market Food Exports

Government initiatives promoting agricultural exports in India, China, Vietnam, Chile, and African economies are boosting food processing output. Sulfur dioxide suppliers can benefit by aligning with export-oriented processors that require consistent, compliant preservation solutions for global markets.

Innovation in Food-Grade Sulfite Technologies

Investment in food-grade sulfur purification, emission-controlled manufacturing, and application-specific formulations presents opportunities for suppliers to differentiate offerings. Low-residue and application-optimized sulfites can command premium pricing in regulated markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1020 Million |

| Market Size in 2026 | USD 1081.20 Million |

| Market Size in 2031 | USD 1446.89 Million |

| CAGR | 6.0% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Form Insights

Solid sulfite derivatives accounted for approximately 48% of the global sulfur dioxide in food market in 2025, making them the dominant form segment. Their leadership is primarily driven by superior chemical stability, longer shelf life, ease of handling, and lower risk during storage and transportation. These characteristics enable precise dosing in industrial food processing, ensuring consistent preservative performance and regulatory compliance.

Liquid sulfur dioxide is extensively utilized in large-scale beverage manufacturing and fruit processing facilities where automated dosing systems are deployed. Its rapid solubility and effectiveness in microbial control make it suitable for high-throughput operations. Meanwhile, gaseous sulfur dioxide is mainly applied in fumigation and surface treatment during post-harvest handling, particularly in controlled storage environments for fruits, where uniform exposure and penetration are critical.

Application Insights

Direct food additive applications dominate the sulfur dioxide in food market, representing around 44% of total demand in 2025. The leading driver for this segment is sulfur dioxide’s proven effectiveness in inhibiting microbial growth, preventing enzymatic browning, and extending shelf life across dried fruits, beverages, and processed foods.

Processing aid applications follow closely, with sulfur dioxide widely used during fermentation, juice extraction, and drying processes to enhance product stability and processing efficiency. Surface treatment and fumigation applications remain essential, particularly in post-harvest fruit preservation for export-oriented supply chains, where sulfur dioxide helps maintain visual appeal, freshness, and compliance with international quality standards.

Functional Role Insights

Preservation remains the leading functional role of sulfur dioxide, accounting for over 50% of global usage. The primary driver is its strong antimicrobial activity combined with its ability to inhibit oxidative reactions and enzymatic browning. These properties are especially critical in dried fruits, wines, juices, and fermented beverages, where shelf stability directly impacts commercial viability.

In addition to preservation, sulfur dioxide plays a significant role as an antioxidant and color stabilizer. These functions support consistent product appearance, flavor retention, and extended storage life, reinforcing its widespread adoption across both traditional and modern food processing applications.

End-Use Industry Insights

Industrial food processing represents the largest end-use industry, holding approximately 61% market share in 2025. This dominance is driven by the large-scale production of processed foods, growing global food trade, and the widespread need for effective preservation solutions that ensure extended shelf life, microbial safety, and product consistency.

Sulfur dioxide is extensively used across industrial operations such as fruit drying, juice concentration, fermentation, and packaged food manufacturing, where cost efficiency and proven preservative performance are critical. The segment further benefits from established regulatory acceptance, standardized dosing practices, and the ability of sulfur dioxide to withstand high-volume, continuous processing environments, reinforcing its strong adoption across industrial food processors worldwide.

Explore more data points, trends and opportunities Download Free Sample Report

Sulfur Dioxide in Food Market Segmentations

By Form

- Solid Sulfite Derivatives

- Liquid Sulfur Dioxide

- Gaseous Sulfur Dioxide

By Application Method

- Direct Food Additive

- Processing Aid

- Surface Treatment & Fumigation

- Packaging Atmosphere Control

By Functional Role

- Preservative

- Antimicrobial Agent

- Antioxidant

- Enzymatic Browning Inhibitor

By Food Category

- Dried Fruits

- Processed Fruits & Vegetables

- Wine & Alcoholic Beverages

- Fruit Juices & Concentrates

- Bakery & Confectionery

- Meat, Poultry & Seafood

By End-Use Industry

- Industrial Food Processing

- Beverage Manufacturing

- Commercial Bakeries

- Export-Oriented Food Producers

Regional Insights

Asia-Pacific

Asia-Pacific leads the global sulfur dioxide in food market with around 38% share in 2025. Regional growth is driven by expanding food processing capacity, rising exports of dried fruits and processed foods, and improving cold-chain and storage infrastructure. China accounts for the largest national demand due to its dominance in dried fruit exports and large-scale industrial food production.

India is the fastest-growing market in the region, expanding at over 7.5% CAGR. Growth is supported by government-backed food processing initiatives, rising domestic consumption of packaged foods and beverages, and increasing export-oriented fruit processing activities.

Europe

Europe held approximately 26% market share, led by Germany, France, Italy, and Spain. The region’s demand is strongly driven by wine production, where sulfur dioxide remains essential for fermentation control, oxidation prevention, and product consistency. Strict food safety regulations and labeling standards further encourage the use of high-purity and precisely dosed sulfite formulations.

Technological innovation, including advanced dosing systems and compliance-focused processing solutions, acts as a key growth driver, allowing manufacturers to balance preservative efficiency with regulatory constraints.

North America

North America accounted for nearly 21% of global demand, with the United States leading the region. Growth is sustained by high consumption of processed foods, strong beverage manufacturing output, and established post-harvest preservation practices.

Despite increasing clean-label and sulfite-reduction pressures, sulfur dioxide usage remains stable due to its unmatched cost efficiency, effectiveness, and regulatory acceptance within defined limits.

Latin America

Latin America represents about 9% of the global market, with Chile and Brazil driving regional demand. Growth is primarily fueled by export-oriented dried fruit, wine, and juice processing industries that rely on sulfur dioxide to meet international quality and shelf-life requirements.

Improving agricultural processing infrastructure and rising participation in global food trade continue to strengthen regional adoption.

Middle East & Africa

The Middle East & Africa region held around 6% share in 2025. Growth is concentrated in South Africa and Egypt, where expanding food processing capacity, increasing fruit exports, and investment in post-harvest preservation technologies are driving sulfur dioxide demand.

Rising focus on reducing food waste and improving export competitiveness further supports market expansion across the region.

Key Players in the Sulfur Dioxide in Food Market

- BASF SE

- Arkema S.A.

- LANXESS AG

- Solvay S.A.

- Nouryon

- Aditya Birla Chemicals

- Merck KGaA

- Tessenderlo Group

- INEOS Group

- Shandong Kailong Chemical

- Gujarat Alkalies and Chemicals

- PQ Corporation

- Chemtrade Logistics

- Sumitomo Chemical

- Mitsubishi Chemical Group