Sugar-Free Liquid Water Enhancers Market Size

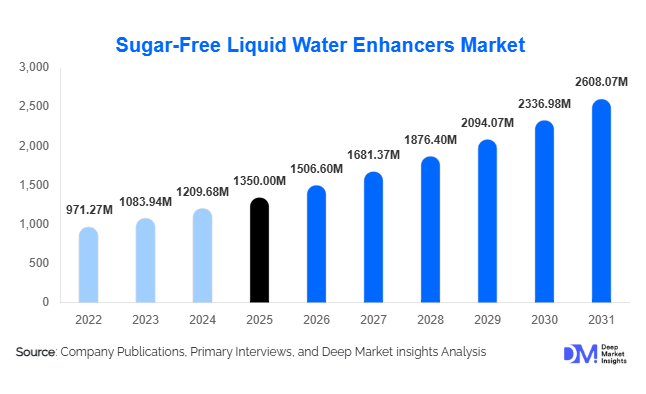

According to Deep Market Insights, the global sugar-free liquid water enhancers market size was valued at USD 1350 million in 2025 and is projected to grow from USD 1506.60 million in 2026 to reach approximately USD 2608.07 million by 2031, expanding at a CAGR of 11.6% during the forecast period (2026–2031). The market growth is primarily driven by rising consumer preference for low-calorie hydration alternatives, increasing awareness of sugar-related health risks, and strong demand for customizable, functional beverage solutions across fitness, wellness, and everyday hydration segments.

Key Market Insights

- Sugar-free liquid water enhancers are increasingly replacing carbonated soft drinks, supported by global sugar reduction initiatives and health-focused consumer behavior.

- Functional hydration products dominate demand, particularly formulations offering electrolytes, vitamins, and energy-boosting benefits.

- North America leads global consumption, driven by high adoption of fitness-oriented and clean-label beverage products.

- Asia-Pacific is the fastest-growing regional market, supported by rapid urbanization, rising disposable incomes, and expanding fitness culture.

- E-commerce and DTC channels are reshaping distribution, enabling niche and premium brands to scale rapidly.

- Advancements in natural sweetener technologies are improving taste profiles and accelerating mainstream adoption.

What are the latest trends in the sugar-free liquid water enhancers market?

Rise of Functional and Wellness-Oriented Hydration

Functional sugar-free water enhancers are gaining strong traction as consumers increasingly view hydration as a vehicle for health and wellness. Products fortified with electrolytes, vitamin B-complex, vitamin C, zinc, and magnesium are witnessing accelerated adoption among fitness enthusiasts and working professionals. Immunity-boosting and metabolism-support formulations are also becoming mainstream, particularly in post-pandemic consumer environments. Brands are positioning these products as daily wellness essentials rather than occasional flavor additives, driving higher consumption frequency and premium pricing.

Shift Toward Clean-Label and Natural Sweeteners

Clean-label trends are significantly influencing product development within the market. Consumers are actively avoiding artificial sweeteners and demanding transparency around ingredient sourcing. This has led to increased adoption of stevia, monk fruit, and fermentation-derived sweetener blends that reduce bitterness while maintaining sweetness intensity. Products featuring non-GMO, allergen-free, and plant-based claims are gaining shelf prominence, particularly in developed markets. Packaging innovations emphasizing sustainability and recyclability further support brand differentiation.

What are the key drivers in the sugar-free liquid water enhancers market?

Growing Global Focus on Sugar Reduction

Government-led sugar taxation policies and public health campaigns aimed at reducing obesity and diabetes are significantly driving demand for sugar-free beverage alternatives. Liquid water enhancers allow consumers to eliminate sugar without compromising flavor, making them an attractive substitute for traditional flavored drinks. Increasing label scrutiny and calorie-conscious consumption habits are reinforcing this shift across both developed and emerging markets.

Expansion of Fitness, Sports, and Active Lifestyles

The rapid expansion of the global fitness economy is fueling demand for portable, functional hydration solutions. Sugar-free liquid water enhancers are widely adopted by gym-goers, athletes, and outdoor enthusiasts due to their convenience, zero-calorie profile, and performance-enhancing formulations. The growing popularity of endurance sports, recreational fitness, and home workouts is further strengthening this demand base.

What are the restraints for the global market?

Taste Acceptance and Flavor Consistency Challenges

Despite advancements in sweetener technologies, taste perception remains a challenge for some consumer segments. Certain natural sweeteners can impart aftertastes, which may limit repeat purchases and slow adoption among first-time users. Maintaining consistent flavor quality across regions and production batches also poses formulation challenges for manufacturers.

Regulatory Variability Across Regions

Differences in sweetener regulations across regions create formulation and compliance complexities. Restrictions on specific artificial and natural sweeteners in Europe and parts of Asia increase development costs and can delay product launches, potentially impacting market growth.

What are the key opportunities in the sugar-free liquid water enhancers industry?

Emerging Market Penetration and Localization

Asia-Pacific, Latin America, and the Middle East represent high-growth opportunities due to rising health awareness and expanding middle-class populations. Localized flavors, affordable pack sizes, and region-specific wellness positioning can significantly improve market penetration. Countries such as India, China, Brazil, and Indonesia offer substantial untapped demand potential.

Personalized Nutrition and Smart Hydration

The integration of personalized nutrition presents strong future opportunities. Brands can leverage data-driven hydration solutions aligned with fitness tracking, dietary preferences, and health goals. Subscription-based DTC models and personalized flavor packs are expected to gain traction, enabling long-term customer engagement and higher lifetime value.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1350 Million |

| Market Size in 2026 | USD 1506.60 Million |

| Market Size in 2031 | USD 2608.07 Million |

| CAGR | 11.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Flavor Type Insights

Fruit-based flavors dominate the sugar-free liquid water enhancers market, accounting for approximately 42% of the global market share in 2025. This leadership is primarily driven by their universal taste appeal, familiarity across age groups, and strong compatibility with functional additives such as vitamins, electrolytes, and minerals. Citrus, berry, and tropical variants remain the most preferred, as they effectively mask aftertastes associated with natural sweeteners while delivering refreshing sensory profiles.

Herbal and botanical flavors are gaining momentum, particularly among wellness-focused consumers seeking natural, calming, and clean-label hydration solutions. Ingredients such as mint, ginger, chamomile, and hibiscus are increasingly positioned around stress relief, digestion, and holistic wellness.Functional specialty flavors, including energy-boosting, immunity-support, and electrolyte-infused blends, are witnessing the fastest growth. This segment is driven by rising fitness participation, demand for performance hydration, and lifestyle-driven consumption among active and on-the-go consumers.

Sweetener Type Insights

Stevia-based formulations hold the largest share of the market at nearly 38% in 2025, driven by strong consumer preference for plant-based, zero-calorie, and naturally sourced sweeteners. Regulatory acceptance, clean-label positioning, and growing awareness of stevia’s health benefits continue to support its dominance.Monk fruit blends are emerging rapidly due to advancements in taste-masking technologies and improved flavor profiles, making them increasingly competitive in premium and health-focused product lines.

Sucralose-based products continue to maintain relevance in cost-sensitive and mass-market segments, supported by their stability, affordability, and consistent sweetness performance.Multi-sweetener formulations are increasingly adopted by manufacturers to optimize taste balance, reduce formulation costs, and comply with evolving regional regulations, making them a strategic choice for global product portfolios.

Distribution Channel Insights

Supermarkets and hypermarkets account for approximately 41% of global sales, driven by strong product visibility, wide brand assortments, and impulse purchasing behavior. These channels remain critical for brand discovery and volume-driven sales.

Online retail and direct-to-consumer (DTC) platforms represent the fastest-growing distribution channel. Growth is fueled by subscription-based purchasing models, influencer-driven marketing strategies, personalized product offerings, and the convenience of home delivery.Specialty health stores continue to attract premium consumers seeking clean-label, functional, and wellness-oriented hydration products, supporting higher-margin sales and brand credibility.

End-Use Insights

Household consumers represent the largest end-use segment, accounting for nearly 48% of total demand. Growth in this segment is driven by daily hydration routines, sugar reduction initiatives, and rising health consciousness among families.

Sports and fitness consumers are the fastest-growing segment, expanding at over 13% CAGR. This growth is supported by increasing participation in gym workouts, endurance sports, recreational fitness, and active lifestyle trends, where convenient and customizable hydration solutions are essential.Foodservice outlets and healthcare institutions are emerging as incremental demand generators, particularly in wellness-focused environments, hospitals, corporate offices, and hospitality settings, where low-sugar hydration options are gaining preference.

Explore more data points, trends and opportunities Download Free Sample Report

Sugar-Free Liquid Water Enhancers Market Segmentations

By Flavor Type

- Fruit-Based (Citrus, Berry, Tropical, Apple, Mixed Fruit)

- Herbal & Botanical

- Functional & Specialty

- Dessert & Indulgent

By Sweetener Type

- Stevia-Based

- Monk Fruit-Based

- Sucralose-Based

- Erythritol & Multi-Sweetener Blends

By Functional Claim

- Hydration Enhancement

- Energy & Focus

- Weight Management

- Immunity & Wellness

- Sports & Fitness Recovery

By Packaging Format

- Squeeze Bottles

- Dropper Bottles

- Single-Serve Sachets/Pods

- Multi-Serve Concentrate Bottles

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail & Direct-to-Consumer

- Specialty Health Stores

- Foodservice & Institutional Sales

By End Use

- Household Consumers

- Sports & Fitness Consumers

- Foodservice (Hotels, Cafés, Restaurants)

- Healthcare & Wellness Institutions

Regional Insights

North America

North America holds approximately 38% of the global market share in 2025, led by the United States, which alone accounts for nearly 30%. Regional dominance is driven by high health awareness, strong fitness culture, early adoption of sugar-free innovations, and widespread availability of premium and functional products. Robust retail infrastructure and aggressive marketing by leading brands further support market expansion.

Europe

Europe accounts for around 26% of global demand, with Germany, the U.K., and France serving as key markets. Growth is supported by strict sugar reduction regulations, strong clean-label preferences, and rising demand for natural sweeteners. Sustainability-driven packaging and transparency in ingredient sourcing further enhance consumer acceptance.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at a CAGR of approximately 14.2%. China, India, and Japan are leading demand growth, driven by rapid urbanization, rising disposable incomes, expanding middle-class populations, and increasing fitness and wellness adoption. The region also benefits from growing e-commerce penetration and rising awareness of lifestyle-related health conditions.

Latin America

Latin America is witnessing gradual but steady adoption, led by Brazil and Mexico. Growth is driven by increasing diabetes prevalence, rising health awareness, and growing demand for functional and reduced-sugar beverages. Improving retail penetration and product affordability are expected to further support market development.

Middle East & Africa

The Middle East & Africa market is supported by premium hydration demand in the UAE and Saudi Arabia, along with expanding urban populations and rising health-conscious consumer segments. Government-led wellness initiatives and growing interest in fitness lifestyles are contributing to the gradual adoption of sugar-free liquid water enhancers across the region.The sugar-free liquid water enhancers market is moderately consolidated, with the top five players collectively accounting for approximately 52% of global market share. Established beverage companies dominate due to strong brand equity, global distribution networks, and continuous product innovation.

Key Players in the Sugar-Free Liquid Water Enhancers Market

- The Coca-Cola Company

- PepsiCo, Inc.

- Nestlé S.A.

- Kraft Heinz Company

- Keurig Dr Pepper

- Arizona Beverage Company

- Hint Water

- Primo Brands

- Vitamin Well AB

- Nuun & Company

- Liquid I.V.

- True Citrus

- Stur Drinks

- Waterdrop

- Cirkul