Soy Lecithin Market Size

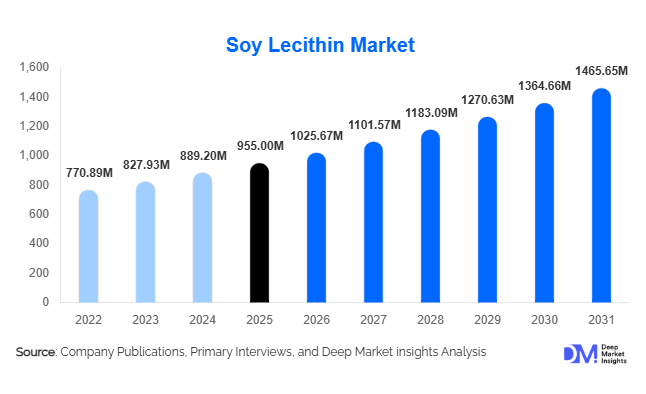

According to Deep Market Insights, the global soy lecithin market size was valued at USD 955 million in 2025 and is projected to grow from USD 1025.67 million in 2026 to reach USD 1465.65 million by 2031, expanding at a CAGR of 7.4% during the forecast period (2026–2031). The soy lecithin market growth is primarily driven by rising demand for natural emulsifiers, increasing adoption of clean-label food ingredients, and expanding applications across food & beverage, animal nutrition, pharmaceuticals, and nutraceuticals.

Key Market Insights

- Soy lecithin remains the most widely used natural emulsifier globally, supported by its multifunctionality and cost efficiency compared to synthetic alternatives.

- Food & beverage applications dominate demand, driven by bakery, confectionery, dairy alternatives, and processed foods.

- Asia-Pacific leads global consumption, supported by rapid food processing growth and expanding soybean crushing capacity.

- Non-GMO and organic soy lecithin segments are growing at a faster pace, particularly in North America and Europe.

- Direct B2B supply contracts dominate distribution, reflecting long-term procurement strategies by large food and feed manufacturers.

- Technological advancements in de-oiling and fractionation are enabling higher-purity and pharmaceutical-grade soy lecithin production.

What are the latest trends in the soy lecithin market?

Rising Demand for Clean-Label and Plant-Based Ingredients

Global food manufacturers are increasingly replacing synthetic emulsifiers with naturally derived alternatives to meet clean-label and transparency requirements. Soy lecithin benefits from its plant-based origin, allergen-managed labeling, and functional versatility. This trend is especially prominent in bakery, confectionery, and dairy-alternative products, where emulsification, texture stability, and shelf-life extension are critical. The clean-label movement has also accelerated the adoption of minimally processed liquid and powdered soy lecithin across premium food formulations.

Expansion of High-Purity and Specialty Lecithin Grades

Technological improvements in fractionation, enzymatic modification, and de-oiling processes are driving the production of high-purity soy lecithin. These specialty grades are increasingly used in pharmaceuticals, nutraceuticals, and cosmetics, where consistent phospholipid content and functionality are essential. Pharmaceutical-grade soy lecithin is gaining traction as a drug delivery excipient, while nutraceutical manufacturers are using it as a bioavailability enhancer in supplements.

What are the key drivers in the soy lecithin market?

Growth of the Global Food Processing Industry

Processed food consumption continues to rise globally, driven by urbanization, changing lifestyles, and increasing demand for convenience foods. Soy lecithin plays a critical role as an emulsifier, dispersing agent, and release agent in baked goods, chocolates, margarines, and instant foods. Expansion of food manufacturing capacity in Asia-Pacific and Latin America has significantly boosted bulk soy lecithin demand.

Rising Demand from Animal Feed and Aquaculture

Soy lecithin improves fat metabolism and nutrient absorption in animal feed, particularly in poultry, swine, and aquaculture applications. Growing global meat consumption and aquaculture output are driving steady demand for feed-grade soy lecithin, especially in China, India, and Southeast Asia.

What are the restraints for the global market?

Volatility in Soybean and Soy Oil Prices

Soy lecithin production is directly linked to soybean crushing and soy oil refining. Fluctuations in soybean prices caused by climate variability, geopolitical trade restrictions, and supply chain disruptions can impact lecithin pricing and manufacturer margins.

Rising Adoption of Alternative Lecithins

Concerns related to soy allergens and GMO labeling are encouraging some manufacturers to explore sunflower and rapeseed lecithin alternatives. While soy lecithin remains dominant, these substitutes pose a competitive restraint in specific premium applications.

What are the key opportunities in the soy lecithin market?

Growth of Non-GMO and Organic Soy Lecithin

Demand for Non-GMO and organic soy lecithin is expanding rapidly, particularly in North America and Europe. Manufacturers investing in identity-preserved sourcing, traceability systems, and organic certifications can command premium pricing and higher margins.

Pharmaceutical and Nutraceutical Expansion

The growing global nutraceutical and pharmaceutical industries present significant opportunities for high-purity soy lecithin. Its role in liposomal drug delivery, supplement formulations, and emulsified APIs positions soy lecithin as a strategic excipient for advanced healthcare applications.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 955 Million |

| Market Size in 2026 | USD 1025.67 Million |

| Market Size in 2031 | USD 1465.65 Million |

| CAGR | 7.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Form Insights

Based on product form, liquid soy lecithin dominates the global market, accounting for approximately 46% of total market share in 2025. Its leadership is primarily driven by cost efficiency, superior emulsification properties, ease of storage and transportation, and seamless integration into large-scale food and animal feed manufacturing processes. Liquid soy lecithin is widely used in bakery products, confectionery, dairy alternatives, and compound feed formulations, where uniform dispersion and processing flexibility are critical.

Powdered and granulated soy lecithin are witnessing steady growth, particularly in dry mixes, instant food products, powdered beverages, and dietary supplements. These forms offer improved shelf stability, precise dosing, and compatibility with dry processing environments, making them increasingly attractive to nutraceutical and functional food manufacturers. Meanwhile, de-oiled soy lecithin is gaining traction in high-value applications such as pharmaceuticals, cosmetics, and infant nutrition, owing to its higher phospholipid concentration, reduced fat content, and enhanced functional purity.

Processing Type Insights

By processing type, conventional soy lecithin remains the dominant segment, holding nearly 62% of the global market share in 2025. This dominance is supported by large-scale soybean availability, well-established extraction infrastructure, and lower production costs, making conventional lecithin the preferred choice for mass-market food, feed, and industrial applications.

However, Non-GMO and organic soy lecithin segments are experiencing faster growth rates, driven by rising consumer awareness, stringent labeling regulations, and increasing demand for clean-label, natural, and sustainably sourced ingredients. Food manufacturers targeting premium, health-oriented, and export markets—particularly in North America and Europe—are increasingly shifting toward Non-GMO and certified organic soy lecithin to meet regulatory and consumer expectations.

End-Use Industry Insights

The food & beverage industry represents the largest end-use segment, accounting for approximately 54% of total market demand in 2025. Growth in this segment is driven by rising consumption of processed and convenience foods, increased use of emulsifiers in bakery and confectionery products, and expanding demand for plant-based and allergen-free formulations.

Animal feed applications form the second-largest segment, supported by the use of soy lecithin as an energy source, pellet binder, and digestibility enhancer in poultry, swine, and aquaculture feed. The pharmaceutical, nutraceutical, and cosmetics sectors collectively represent a high-growth segment, benefiting from soy lecithin’s role as a bioavailability enhancer, stabilizer, and natural emulsifier. Industrial applications, including paints, inks, coatings, and lubricants, contribute a smaller yet stable share, supported by lecithin’s lubricating and dispersing properties.

Distribution Channel Insights

Direct sales dominate the global soy lecithin market, accounting for nearly 61% of total distribution in 2025. Large food processors, feed manufacturers, and pharmaceutical companies prefer direct procurement through long-term contracts to ensure consistent quality, reliable supply, and price stability.

Distributors and ingredient traders play a vital role in serving mid-sized manufacturers and regional buyers by offering flexible order quantities and logistical support. Additionally, online procurement platforms and digital ingredient marketplaces are emerging as alternative channels, particularly for specialty grades, Non-GMO, and small-volume purchases, enhancing market accessibility for niche and startup manufacturers.

Explore more data points, trends and opportunities Download Free Sample Report

Soy Lecithin Market Segmentations

By Product Form

- Liquid Soy Lecithin

- Powdered Soy Lecithin

- Granulated Soy Lecithin

- De-oiled Soy Lecithin

By Processing Type

- Conventional Soy Lecithin

- Non-GMO Soy Lecithin

- Organic Soy Lecithin

By Functionality

- Emulsifier

- Dispersing Agent

- Wetting Agent

- Release Agent

- Anti-Spattering Agent

By End-Use Industry

- Food & Beverage

- Animal Feed

- Pharmaceuticals

- Dietary Supplements & Nutraceuticals

- Cosmetics & Personal Care

- Industrial Applications

By Distribution Channel

- Direct Sales (B2B / Contract Supply)

- Distributors & Ingredient Traders

- Online & E-Procurement Platforms

Regional Insights

Asia-Pacific

Asia-Pacific holds the largest share of the global soy lecithin market, accounting for approximately 34% of global demand in 2025. China remains the largest consumer due to its extensive food processing, bakery, confectionery, and animal feed industries, while India represents the fastest-growing market, supported by rising packaged food consumption and expanding soybean processing capacity.Key growth drivers in the region include rapid urbanization, increasing disposable incomes, expanding middle-class populations, and strong growth in processed food, infant nutrition, and poultry feed sectors. Government initiatives supporting domestic soybean cultivation and food manufacturing further enhance regional market expansion.

North America

North America accounts for approximately 26% of global soy lecithin demand, led by the United States. The region benefits from a mature food processing ecosystem, high consumption of nutraceuticals and dietary supplements, and widespread adoption of functional and clean-label ingredients.Regional growth is driven by rising demand for Non-GMO and organic food products, increasing use of lecithin in plant-based alternatives, and strong regulatory emphasis on ingredient transparency. Advanced R&D capabilities and innovation in food formulations continue to support market development.

Europe

Europe represents a significant market for soy lecithin, particularly Non-GMO and organic variants, with Germany, France, and the U.K. leading demand. The region’s market is supported by stringent food safety regulations and strong consumer preference for natural additives.Growth drivers include increasing demand for clean-label bakery and confectionery products, expansion of organic food markets, and regulatory restrictions on synthetic emulsifiers, which encourage the use of plant-based alternatives such as soy lecithin.

Latin America

Latin America plays a critical role in the global soy lecithin supply chain, with Brazil and Argentina dominating production and exports due to extensive soybean cultivation and crushing capacity.Regional growth is supported by strong agricultural output, cost-competitive raw material availability, and rising investments in value-added soybean processing. Increasing domestic consumption of processed foods and animal feed further contributes to market expansion.

Middle East & Africa

The Middle East & Africa market is primarily driven by imported soy lecithin to meet food manufacturing and animal feed requirements. Growth remains moderate but consistent across the region.Key drivers include expanding food processing industries, rising population and urbanization, increasing demand for packaged foods, and growing livestock and poultry sectors, particularly in Gulf countries and South Africa.

Key Players in the Soy Lecithin Market

- Cargill, Inc.

- Archer Daniels Midland (ADM)

- Bunge Limited

- Wilmar International

- Lipoid GmbH

- Stern-Wywiol Gruppe

- DuPont (IFF Nutrition & Biosciences)

- Clarkson Grain

- American Lecithin Company

- Sodrugestvo Group

- Lasenor Emul

- Kewpie Corporation

- Ruchi Soya Industries

- Shankar Soya Concepts

- Vav Life Sciences