Oryzenin Market Size

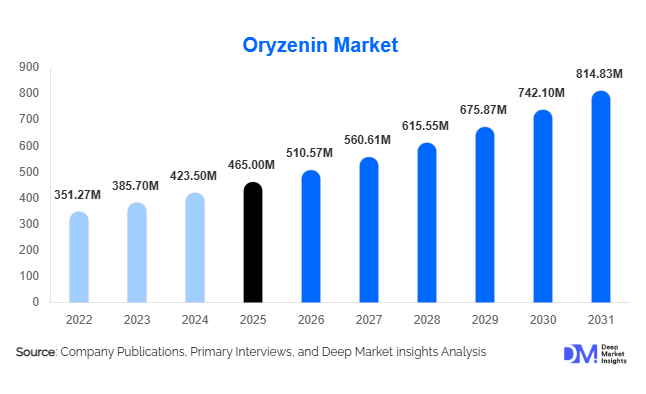

According to Deep Market Insights, the global Oryzenin (rice protein) market size was valued at USD 465 million in 2025 and is projected to grow from USD 510.57 million in 2026 to reach USD 814.83 million by 2031, expanding at a CAGR of 9.8% during the forecast period (2026–2031). The Oryzenin market growth is primarily driven by the rapid expansion of plant-based food systems, rising demand for hypoallergenic and clean-label proteins, and increasing adoption of rice protein across sports nutrition, infant nutrition, and medical food applications.

Key Market Insights

- Rice protein isolate dominates the product landscape, accounting for the largest share due to its high protein purity and suitability for sports and medical nutrition.

- Food & beverage applications remain the largest demand contributor, supported by strong growth in plant-based dairy and meat alternatives.

- North America leads global consumption, driven by high penetration of vegan, allergen-free, and performance nutrition products.

- Asia-Pacific is the fastest-growing regional market, supported by raw material availability, expanding domestic processing capacity, and government-backed protein initiatives.

- Direct B2B sales dominate distribution, as large food and nutraceutical manufacturers prefer long-term ingredient supply contracts.

- Technological advancements in enzymatic processing are improving the solubility, taste profile, and functional performance of Oryzenin.

What are the latest trends in the Oryzenin market?

Rising Adoption in Plant-Based and Allergen-Free Foods

Oryzenin is increasingly being adopted as a preferred protein source in plant-based and allergen-free food formulations. Unlike soy and dairy proteins, rice protein offers a hypoallergenic profile, making it suitable for sensitive consumer groups, including infants, elderly populations, and individuals with food intolerances. Food manufacturers are incorporating Oryzenin into plant-based dairy alternatives, baked goods, snacks, and meat analogs to meet growing clean-label and free-from claims. The rising prevalence of vegan and flexitarian diets globally continues to strengthen demand for rice-derived proteins.

Advancements in Protein Extraction and Functional Enhancement

Processing innovations, particularly enzymatic hydrolysis and wet extraction technologies, are significantly improving the functional properties of Oryzenin. Enhanced solubility, improved amino acid availability, and reduced off-flavors are enabling broader use in ready-to-drink beverages, protein powders, and clinical nutrition products. Manufacturers are also focusing on textured rice protein development to better replicate meat-like structures, supporting demand from alternative protein brands.

What are the key drivers in the Oryzenin market?

Growing Demand for Plant-Based Nutrition

The accelerating shift toward plant-based diets is a major growth driver for the Oryzenin market. Consumers are increasingly replacing animal-derived proteins with sustainable alternatives due to health, ethical, and environmental concerns. Rice protein aligns well with these preferences, offering digestibility, neutral taste, and compatibility with vegan formulations. This trend is particularly strong in North America and Europe, where plant-based product innovation is expanding rapidly.

Rising Health and Wellness Awareness

Consumers are prioritizing proteins that support digestive health, muscle recovery, and overall wellness. Oryzenin’s gluten-free and hypoallergenic characteristics make it highly suitable for dietary supplements, sports nutrition, and medical nutrition products. Growing awareness of protein quality and clean sourcing is further supporting market expansion.

What are the restraints for the global market?

Higher Production and Processing Costs

Rice protein extraction is more capital-intensive compared to soy or wheat protein, resulting in higher production costs. Advanced wet and enzymatic processing methods require significant investment in machinery and energy, which can limit pricing competitiveness in cost-sensitive markets.

Functional Performance Limitations

Despite technological improvements, rice protein still faces challenges related to solubility and texture in certain food applications. Manufacturers often need formulation adjustments or blending with other plant proteins, which can increase development costs and complexity.

What are the key opportunities in the Oryzenin industry?

Expansion in Sports and Performance Nutrition

Sports and performance nutrition represent a high-growth opportunity for Oryzenin. Demand for dairy-free and allergen-free protein powders is rising among athletes and fitness-conscious consumers. Rice protein isolates with enhanced digestibility and amino acid fortification are increasingly being positioned as viable alternatives to whey protein.

Regional Manufacturing and Government Support

Government initiatives such as “Make in India” and “Made in China 2025” are encouraging domestic production of plant-based proteins. These initiatives reduce import dependence, improve supply chain resilience, and support capacity expansion, creating opportunities for both local and global manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 465 Million |

| Market Size in 2026 | USD 510.57 Million |

| Market Size in 2031 | USD 814.83 Million |

| CAGR | 9.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Rice protein isolate holds the largest share of the global Oryzenin market, accounting for approximately 42% of total market revenue in 2025. The dominance of this segment is primarily driven by its high protein concentration (≥90%), superior digestibility, and low allergen profile, making it the preferred choice for sports nutrition, medical foods, and clinical nutrition formulations. Rising demand for dairy-free protein powders and clean-label nutritional products in North America and Europe has further strengthened the adoption of rice protein isolates. Rice protein concentrates represent a significant share of demand, particularly in bakery, snacks, and functional food applications, where cost efficiency and moderate protein enrichment are key formulation requirements. These products are widely adopted by mid-sized food manufacturers seeking a balance between nutritional value and pricing competitiveness.

Textured rice protein is gaining rapid traction within plant-based meat and alternative protein formulations, driven by improvements in extrusion and texturization technologies that enhance fibrous structure and mouthfeel. Meanwhile, hydrolyzed rice protein is witnessing increasing utilization in infant nutrition, clinical dietary products, and cosmetics, owing to its enhanced bioavailability, easy absorption, and proven skin-conditioning properties. Growth in this segment is particularly strong in the Asia-Pacific, where rice-based ingredients are culturally preferred.

Application Insights

Food and beverage applications dominate the global Oryzenin market, contributing nearly 48% of total demand in 2025. Growth in this segment is driven by the rapid expansion of plant-based dairy alternatives, meat analogs, protein-enriched snacks, and functional beverages. Food manufacturers increasingly prefer rice protein due to its neutral flavor profile, clean-label compatibility, and ability to meet allergen-free claims. Dietary supplements represent the second-largest application segment, supported by rising protein consumption among health-conscious consumers, aging populations, and fitness enthusiasts. Rice protein is increasingly positioned as a plant-based alternative to whey, particularly in protein powders, capsules, and ready-to-mix formulations.

Cosmetic and personal care applications are expanding steadily, especially across the Asia-Pacific markets. Rice-derived proteins are valued for their moisturizing, anti-inflammatory, and skin barrier-repair properties, leading to growing incorporation in skincare, haircare, and dermatological formulations. This trend is reinforced by increasing consumer preference for plant-based and naturally sourced cosmetic ingredients.

Distribution Channel Insights

Direct B2B sales dominate the Oryzenin market, accounting for approximately 60% of global distribution in 2025. Large food, nutraceutical, and pharmaceutical manufacturers rely on long-term supply agreements with ingredient producers to ensure consistent quality, regulatory compliance, and cost stability. This channel remains preferred for high-volume procurement and customized protein formulations.

Specialty ingredient distributors play a critical role in serving mid-sized and regional manufacturers, offering technical support, formulation assistance, and flexible purchasing volumes. These distributors help expand market penetration across emerging economies and niche application areas. Online B2B platforms are emerging as a supplementary distribution channel, particularly for startups, small-scale formulators, and innovation-driven brands. Digital procurement platforms offer easier access to specialty proteins, transparent pricing, and faster sourcing, supporting early-stage product development and market entry.

End-Use Insights

Vegan and plant-based food manufacturers represent the largest end-use segment, accounting for approximately 37% of total Oryzenin market demand in 2025. Strong consumer shift toward plant-based diets, combined with regulatory support for alternative proteins, continues to drive sustained demand from this segment. Sports nutrition brands are the fastest-growing end-use segment, expanding at over 11% CAGR during the forecast period. Demand is fueled by increasing adoption of dairy-free, allergen-free protein supplements among athletes, gym-goers, and lifestyle consumers seeking clean and sustainable nutrition.

Infant and medical nutrition applications are emerging as high-value segments due to stringent allergen-free requirements, regulatory oversight, and the growing prevalence of digestive sensitivities. Rice protein’s hypoallergenic nature positions it as a preferred ingredient for specialized nutrition products in both developed and emerging markets.

Explore more data points, trends and opportunities Download Free Sample Report

Oryzenin Market Segmentations

By Product Type

- Rice Protein Isolate

- Rice Protein Concentrate

- Textured Rice Protein

- Hydrolyzed Rice Protein

By Application

- Food & Beverages

- Dietary Supplements

- Animal Nutrition

- Cosmetics & Personal Care

- Pharmaceutical & Medical Nutrition

By Distribution Channel

- Direct B2B Sales

- Specialty Ingredient Distributors

- Online B2B Platforms

By End Use

- Vegan & Plant-Based Food Manufacturers

- Sports Nutrition Brands

- Nutraceutical Companies

- Infant & Medical Nutrition Manufacturers

- Cosmetic & Personal Care Companies

Regional Insights

North America

North America accounted for approximately 32% of the global Oryzenin market in 2025, with the United States leading regional demand. Growth is driven by the strong presence of sports nutrition brands, plant-based food innovators, and dietary supplement manufacturers. High consumer awareness of clean-label and allergen-free nutrition, coupled with well-established regulatory frameworks supporting plant-based ingredients, continues to reinforce market expansion. The region also benefits from advanced food processing infrastructure and high R&D investment in alternative proteins.

Europe

Europe held nearly 28% of the global market share, supported by stringent clean-label regulations and a strong consumer preference for sustainable, traceable, and non-GMO food ingredients. Germany, the U.K., and France are key demand centers, driven by growth in vegan food consumption and functional nutrition. European food manufacturers are increasingly adopting rice protein to comply with allergen labeling regulations and to support carbon footprint reduction goals.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, registering a CAGR of approximately 11.5%. China, India, and Japan lead demand due to abundant rice availability, expanding domestic protein processing capacity, and supportive government initiatives promoting plant-based and alternative protein production. Rising health awareness, increasing disposable income, and cultural familiarity with rice-based ingredients further accelerate adoption across food, nutrition, and cosmetic applications.

Latin America

Latin America represents an emerging growth market, with Brazil and Mexico showing increasing adoption of rice protein in dietary supplements, functional foods, and sports nutrition. Growth is supported by expanding urban middle-class populations, rising fitness culture, and increasing imports of plant-based ingredients. Local manufacturers are gradually incorporating rice protein into formulations to diversify protein sources beyond soy.

Middle East & Africa

The Middle East and Africa region remains nascent but is witnessing gradual growth, driven by increasing imports of plant-based proteins, rising health consciousness, and expanding vegan and flexitarian consumer bases. Gulf countries such as the UAE and Saudi Arabia are emerging as key demand hubs due to premium nutrition trends and growing investment in functional food manufacturing. In Africa, demand is supported by improving food processing capabilities and increasing awareness of plant-based nutrition.