Organic Soy Protein Concentrate Market Size

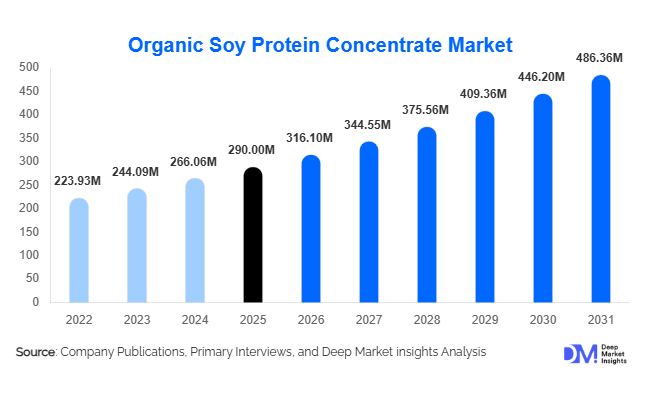

According to Deep Market Insights, the global organic soy protein concentrate market was valued at USD 290 million in 2025 and is projected to grow from USD 316.10 million in 2026 to reach USD 486.36 million by 2031, expanding at a CAGR of 9.0% during the forecast period (2026–2031). The market growth is primarily driven by the increasing adoption of plant-based diets, rising consumer preference for clean-label and organic ingredients, and technological advancements in extraction and formulation methods that enhance functional and sensory properties of soy proteins.

Key Market Insights

- Powder form of organic soy protein concentrate dominates globally, accounting for 68% of the 2025 market, due to its versatility, long shelf life, and ease of incorporation into beverages, bakery products, and functional foods.

- Food & beverages are the largest application segment, representing 61% of demand, fueled by growing plant-based meat alternatives, dairy substitutes, and protein-fortified functional foods.

- North America leads the regional market with 36% share in 2025, driven by strong consumer awareness, mature retail and e-commerce channels, and stringent organic certifications.

- Asia-Pacific is the fastest-growing region, led by China and India, due to rising urbanization, expanding middle-class incomes, and increasing health and wellness awareness.

- Technological adoption, including enzyme-assisted extraction, cold-press processing, and improved solubility formulations, is enhancing product quality and enabling broader applications across food, nutraceuticals, and personal care products.

- Export demand is increasing, particularly from North America and Europe to Asia and the Middle East, where certified organic protein ingredients command a premium price.

What are the latest trends in the organic soy protein concentrate market?

Rising Demand for Plant-Based & Clean-Label Ingredients

Consumers are increasingly prioritizing plant-based diets and clean-label products, boosting the demand for organic soy protein concentrate. Its high protein content, balanced amino acid profile, and non-GMO certification make it ideal for meat alternatives, dairy substitutes, nutrition bars, and functional beverages. Brands are focusing on transparent sourcing and sustainability, using organic soy protein concentrate as a key differentiator in competitive markets.

Technology-Driven Product Innovation

Emerging processing technologies are improving the functionality, flavor, and solubility of organic soy protein concentrate. Enzyme-assisted extraction, cold-press methods, and protein fractionation allow manufacturers to deliver enhanced protein performance without compromising organic certification. These innovations are particularly important for meat alternatives, dairy substitutes, and ready-to-drink beverages, where sensory attributes play a critical role in consumer acceptance.

What are the key drivers in the organic soy protein concentrate market?

Growth of Plant-Based and Functional Food Markets

The rising adoption of plant-based diets and functional foods is a major growth driver. Consumers are seeking protein-rich alternatives that support health, weight management, and wellness. Organic soy protein concentrate is increasingly incorporated into high-growth products such as protein bars, sports nutrition formulations, dairy alternatives, and fortified beverages, driving both volume and revenue expansion.

Increasing Awareness of Organic and Clean-Label Products

Consumers are willing to pay a premium for certified organic products that meet strict regulatory standards. Government-backed organic programs, stringent labeling requirements, and growing trust in organic certifications (USDA Organic, EU Organic) are supporting demand growth. This trend is particularly strong in North America and Europe, where clean-label and non-GMO credentials significantly influence purchasing decisions.

What are the restraints for the global market?

Premium Pricing and Supply Constraints

Organic soy protein concentrate is more expensive than conventional variants due to certification, limited acreage of organic soybeans, and higher processing costs. These pricing premiums can restrict adoption in cost-sensitive sectors such as animal feed and foodservice.

Formulation and Sensory Challenges

High inclusion rates of soy protein concentrate can cause beany flavors or texture issues in finished products. Manufacturers must invest in flavor masking, emulsification techniques, and careful formulation design, which increases R&D costs and production complexity.

What are the key opportunities in the organic soy protein concentrate industry?

Emerging Markets in Asia-Pacific and Latin America

Urbanization, rising incomes, and growing health awareness in China, India, and Brazil present significant growth opportunities. These regions are witnessing increased consumption of plant-based foods, dairy substitutes, and functional beverages, creating demand for high-quality, certified organic soy protein concentrate. Government support for organic farming and imports further boosts the market potential.

Integration into Sports Nutrition and Nutraceuticals

Organic soy protein concentrate is increasingly used in sports nutrition products, dietary supplements, and wellness beverages. Its high protein content, plant-based origin, and clean-label attributes make it a preferred ingredient for health-conscious consumers. The growing trend of active lifestyles and wellness-focused diets is opening new avenues for product innovation.

Technological Advancements in Extraction and Functionalization

Advancements such as cold-press extraction, enzyme-assisted processing, and improved protein solubility expand the functionality of soy protein concentrate in various applications. These technologies allow manufacturers to create better-tasting, higher-performing products suitable for meat alternatives, dairy replacements, and ready-to-drink formulations.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 290 Million |

| Market Size in 2026 | USD 316.10 Million |

| Market Size in 2031 | USD 486.36 Million |

| CAGR | 9.0% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Powder/dry organic soy protein concentrate continues to dominate the global market due to its extended shelf life, ease of handling, superior dispersibility, and versatility across multiple applications. Its adaptability makes it the preferred choice for food manufacturers, nutraceutical producers, and beverage formulators, accounting for the majority share of global consumption. Liquid concentrates are gaining traction, particularly in ready-to-drink beverages and dairy alternative formulations, offering convenience in industrial production lines and faster integration into liquid-based recipes. Granular and instantized forms, while niche, serve specialized applications in foodservice, bakery solutions, and dietary supplements where rapid solubility or precise dosing is critical. The dominance of the powder segment is primarily driven by its broad functionality, cost efficiency in transportation and storage, and compatibility with high-protein, clean-label formulations, positioning it as the key revenue contributor in the global market.

Application Insights

Food & beverages remain the largest application segment, representing the majority of market demand. Within this segment, plant-based meat alternatives, dairy substitutes, and protein-fortified beverages are the fastest-growing categories, reflecting rising consumer health consciousness and the shift toward sustainable, plant-based diets. Animal feed follows as a significant segment, particularly organic livestock and aquaculture feed, where soy protein concentrate enhances nutritional profiles while supporting organic certification standards. Nutraceutical applications leverage soy protein for sports nutrition, protein powders, and dietary supplements targeting active lifestyles and wellness-focused consumers. Cosmetic and personal care applications, though smaller in scale, are emerging steadily, using soy protein concentrate for functional benefits such as emulsification, moisturizing, and texturization in creams and lotions. The growth across applications is strongly influenced by consumer trends toward high-protein, plant-based, and clean-label products that combine health, convenience, and sustainability.

Distribution Channel Insights

Offline retail channels continue to dominate due to consumer preference for in-store certification verification, product familiarity, and tactile inspection, with supermarkets, hypermarkets, and specialty health food stores serving as the primary points of sale. However, online retail is rapidly expanding, particularly for niche brands, premium products, and direct-to-consumer offerings, providing convenience, broader access, and brand storytelling opportunities. B2B direct supply remains a critical distribution channel for large-scale food manufacturers and nutraceutical companies, ensuring consistent quality, bulk availability, and supply chain traceability. Increasing adoption of digital procurement platforms, integrated supply chain solutions, and e-commerce marketplaces is enhancing market reach, particularly for emerging manufacturers targeting geographically dispersed customers.

End-Use Insights

Food manufacturers remain the largest end users, accounting for approximately 58% of the market, driven by widespread incorporation of organic soy protein concentrate in meat alternatives, bakery products, functional beverages, and fortified foods. Animal feed producers and nutraceutical companies represent growing segments, leveraging the protein content and clean-label credentials of organic soy protein concentrate to meet increasing demand for organic livestock feed and plant-based dietary supplements. Food service adoption, although smaller, is rising in premium and health-focused segments, including high-end restaurants, meal-kit providers, and wellness cafes seeking protein-enriched ingredients that align with clean-label and sustainability trends. The growth in end-use sectors is primarily fueled by consumer preference for plant-based nutrition, regulatory support for organic labeling, and the expanding adoption of functional foods and beverages globally.

Explore more data points, trends and opportunities Download Free Sample Report

Organic Soy Protein Concentrate Market Segmentations

By Product Type

- Powder/Dry Organic Soy Protein Concentrate

- Liquid Organic Soy Protein Concentrate

- Granular/Instantized Organic Soy Protein Concentrate

By Application

- Food & Beverages

- Animal Feed

- Nutraceuticals/Sports Nutrition

- Cosmetics & Personal Care

By Distribution Channel

- Offline Retail (Supermarkets, Health Stores)

- Online Retail / D2C Platforms

- B2B Direct Supply

By End-Use Industry

- Food Manufacturing

- Animal Feed Production

- Nutraceutical & Dietary Supplement Companies

- Foodservice & Premium Restaurants

Regional Insights

North America

North America is the largest regional market (36% of global share in 2025), led by the U.S. Strong consumer awareness of organic and plant-based products, established organic certification frameworks (USDA Organic), and robust retail penetration drive growth. Canada also shows steady uptake, particularly in protein-fortified beverages and plant-based meat alternatives. Regional growth is supported by health-conscious consumer trends, increasing demand for functional foods, high disposable incomes, and a mature supply chain infrastructure that facilitates the reliable distribution of certified organic soy protein concentrate. Investments in local organic soybean production and processing facilities further strengthen market development.

Europe

Europe accounts for 29% of the global market, with Germany, the UK, and France leading demand. High per capita consumption of plant-based foods, strict organic labeling regulations, and strong consumer preference for clean-label products support steady adoption. Functional foods, dairy alternatives, and plant-based meat products are key growth drivers. The region benefits from increasing health and sustainability awareness, government incentives for organic farming, and established distribution networks across retail and foodservice channels. Consumer focus on protein-enriched, low-impact products, combined with growing plant-based diet adoption, is accelerating regional demand.

Asia-Pacific

Asia-Pacific is the fastest-growing region, driven by China and India. Rising middle-class incomes, rapid urbanization, and increasing health-consciousness are fueling demand in food & beverages and nutraceutical applications. Expanding food processing infrastructure, emerging organic certification programs, and growing e-commerce adoption support market penetration. Rising awareness of plant-based nutrition and clean-label ingredients, combined with government policies encouraging organic agriculture, are key drivers of growth. Urban consumers in major cities are increasingly seeking protein-fortified functional beverages, meat alternatives, and wellness supplements, providing a strong growth runway.

Latin America

Brazil and Mexico are driving regional growth, with limited domestic organic soybean production necessitating imports from North America. Increasing consumer awareness of plant-based diets, rising health-consciousness, and the growing popularity of functional foods support market expansion. Investments in food processing infrastructure, improved cold-chain logistics, and import facilitation are key growth drivers. The shift toward premium, health-oriented food products and expanding urban middle-class populations are further supporting market development.

Middle East & Africa

While smaller in market share, demand in GCC countries and South Africa is increasing due to rising organic food awareness, premium foodservice adoption, and the desire for imported certified organic ingredients. Intra-African trade and investment in urban food retail networks are contributing to gradual growth. Key drivers include increasing health consciousness, higher disposable incomes, government initiatives promoting food quality and safety, and rising urbanization leading to greater demand for functional and protein-enriched products.

Company Market

Key Players in the Organic Soy Protein Concentrate Market

- Harvest Innovations

- Puris Foods

- SunOpta

- Devansoy Inc.

- The Scoular Company

- Cargill, Incorporated

- Archer Daniels Midland (ADM)

- Ingredion Incorporated

- Batory Foods

- Axiom Foods

- Eden Foods

- Solae LLC

- Tofflon Science & Technology

- Nature’s Path Foods

- BioProtein Technologies