Mycotoxin Testing Market Size

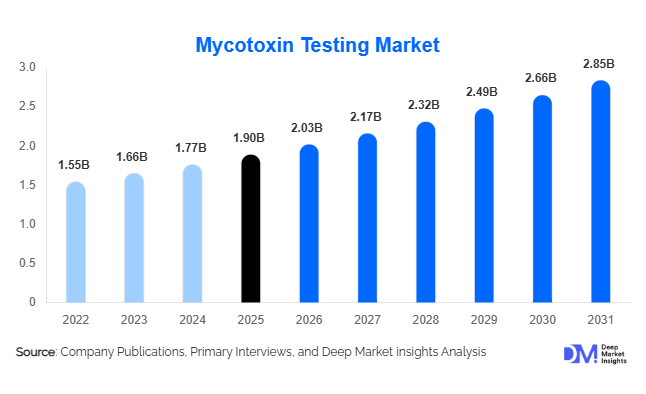

According to Deep Market Insights, the global mycotoxin testing market size was valued at USD 1.9 billion in 2025 and is projected to grow from USD 2.03 billion in 2026 to reach USD 2.85 billion by 2031, expanding at a CAGR of 7% during the forecast period (2026–2031). The market growth is primarily driven by stringent food safety regulations, rising consumer awareness about foodborne toxins, and the adoption of advanced testing technologies such as chromatography, immunoassays, and AI-enabled rapid detection systems.

Key Market Insights

- Chromatography-based testing dominates the global market due to high accuracy, regulatory acceptance, and suitability for multi-mycotoxin detection across food and feed commodities.

- Aflatoxins are the most frequently tested mycotoxins, reflecting their widespread prevalence and high health risk profile, especially in grains, nuts, and spices.

- Food manufacturers and processors lead end-user demand, driven by regulatory compliance, internal quality assurance, and export certification requirements.

- North America holds the largest regional market share, supported by USDA/FDA regulations, advanced laboratory infrastructure, and elevated consumer food safety awareness.

- Asia-Pacific is the fastest-growing region, fueled by agricultural export demand, strengthening domestic food safety regulations, and rising awareness among consumers and producers.

- Rapid testing technologies and AI-enabled solutions are increasingly integrated into workflows, offering faster detection, traceability, and predictive insights for food safety management.

What are the latest trends in the mycotoxin testing market?

Adoption of Rapid and On-site Testing Solutions

Rapid test kits and on-site screening technologies are increasingly adopted to complement laboratory-based confirmatory methods. These solutions allow food and feed producers to quickly identify contamination in supply chains, reducing the risk of recalls and production losses. Portable immunoassays and biosensors are gaining popularity in emerging markets due to their low cost, simplicity, and quick turnaround, making them suitable for initial screening before laboratory confirmation. Companies are also developing multiplex testing kits that simultaneously detect multiple mycotoxins, enhancing efficiency and compliance readiness.

Integration of AI and Digital Platforms

AI-powered detection systems and cloud-based data management platforms are transforming mycotoxin testing. Machine learning algorithms are applied to spectral data for faster, more accurate detection, while digital dashboards centralize results for compliance reporting and predictive analysis. Food processors and regulators increasingly use these solutions to monitor trends, forecast contamination risks, and optimize testing schedules. This trend particularly appeals to large-scale manufacturers seeking real-time insights, regulatory compliance, and enhanced supply chain transparency.

What are the key drivers in the mycotoxin testing market?

Stringent Food Safety Regulations

Global regulatory frameworks, including EU maximum limits, USDA/FDA guidelines, and Codex Alimentarius standards, drive demand for regular and accurate mycotoxin testing. Compliance with these regulations is essential for exporters and domestic producers, leading to increased adoption of advanced testing methods. Regular audits, certification requirements, and import/export inspections further bolster market demand for both laboratory and rapid test solutions.

Rising Consumer Awareness

Heightened awareness of mycotoxin-related health risks is prompting food manufacturers to implement proactive quality assurance programs. Consumers increasingly demand toxin-free products, motivating companies to adopt robust testing strategies. This trend is particularly strong in high-value commodities such as baby food, dairy, and processed snacks, where contamination risks carry severe health and economic consequences.

Technological Advancements in Detection Methods

Advances in chromatography, mass spectrometry, biosensors, and immunoassays have enhanced test sensitivity, throughput, and operational efficiency. Emerging technologies, such as portable PCR and AI-enabled platforms, allow for rapid, high-accuracy detection, driving broader adoption across food and feed sectors. This facilitates both regulatory compliance and risk mitigation in global supply chains.

What are the restraints for the global market?

High Costs of Advanced Testing Systems

Advanced instruments like LC-MS/MS and high-resolution HPLC systems require significant capital and operational investment, limiting accessibility for small and medium enterprises. Maintenance, calibration, and skilled personnel requirements add to the total cost of ownership, slowing adoption in emerging markets and smaller production facilities.

Infrastructure Gaps in Developing Regions

Limited laboratory infrastructure and a shortage of skilled technicians in many developing countries restrict market expansion. In regions lacking accredited facilities, the adoption of sophisticated testing technologies remains constrained, requiring public-private investment and capacity-building initiatives to enhance accessibility.

What are the key opportunities in the mycotoxin testing industry?

Harmonization of Global Regulatory Standards

The alignment of mycotoxin regulations across countries creates opportunities for standardized testing protocols and globally validated solutions. Exporters and food processors can streamline compliance, while testing service providers can expand offerings across multiple geographies without region-specific modifications. Harmonized standards also facilitate market entry for emerging players and support international trade growth.

Integration of AI and Smart Testing Platforms

Combining digital analytics with rapid testing technologies offers improved detection accuracy, predictive insights, and traceability. AI-enabled solutions reduce manual intervention, optimize resource utilization, and enhance supply chain monitoring. Companies that provide end-to-end platforms integrating detection, reporting, and risk forecasting stand to gain a competitive advantage.

Growing Demand in Emerging Economies

Asia-Pacific, Latin America, and Africa offer high growth potential due to expanding agricultural production, export requirements, and rising consumer food safety awareness. Countries like China, India, and Brazil are investing in laboratory infrastructure and regulatory compliance programs, driving the adoption of advanced and rapid testing solutions. This creates opportunities for both local and international market players to establish a strong presence in these regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.9 Billion |

| Market Size in 2026 | USD 2.03 Billion |

| Market Size in 2031 | USD 2.85 Billion |

| CAGR | 7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Chromatography-based methods dominate the global mycotoxin testing market, primarily due to their high analytical accuracy, multi-mycotoxin detection capability, and strong regulatory acceptance across major food safety authorities. Technologies such as LC-MS/MS and HPLC are widely used for confirmatory testing, particularly for export-oriented food and feed products, as they meet stringent compliance requirements set by the EU, FDA, and Codex Alimentarius. The ability of chromatography-based systems to deliver reproducible, high-sensitivity results makes them indispensable for high-risk and high-value commodities, reinforcing their leadership position in overall market revenue.

Emerging biosensor-based platforms and PCR-based technologies are gaining traction in high-throughput and on-site applications, driven by demand for faster results, automation, and digital integration. These technologies complement traditional laboratory testing by supporting decentralized testing models and real-time monitoring, particularly in regions with limited laboratory infrastructure.

Application Insights

Food and feed testing remain the primary applications for mycotoxin analysis, collectively accounting for the majority of market demand. Grain and cereal testing dominates this segment due to the high susceptibility of crops such as maize, wheat, and rice to fungal contamination during storage and transportation. Given the central role of cereals in global food and feed supply chains, regulatory agencies mandate frequent testing, making this application the leading revenue contributor.

High-value commodities such as dairy products, spices, nuts, dried fruits, and infant food are subject to particularly stringent testing requirements. Even low levels of contamination in these products can trigger recalls, trade rejections, and reputational damage, prompting manufacturers to implement rigorous testing protocols. Infant nutrition and baby food applications are among the fastest-growing sub-segments due to zero-tolerance thresholds in several countries. Emerging applications include environmental testing in agricultural settings, phytosanitary inspections for export certification, and the validation of organic, non-GMO, and specialty food claims. As sustainability and clean-label trends intensify, mycotoxin testing is increasingly used to support premium product positioning and regulatory transparency.

Distribution Channel Insights

Mycotoxin testing services are primarily delivered through centralized laboratory networks, direct B2B engagements with food and feed manufacturers, and the distribution of rapid test kits. Accredited contract laboratories play a critical role in servicing small and mid-sized producers that lack in-house analytical capabilities, offering confirmatory testing, certification, and regulatory documentation.

Direct B2B relationships between testing solution providers and large food processors are expanding, particularly for high-throughput chromatography systems and long-term testing contracts. Meanwhile, distributors and channel partners facilitate the penetration of rapid test kits in emerging markets, where affordability and accessibility are key adoption drivers. Digital platforms, cloud-based reporting tools, and IoT-enabled testing devices are increasingly integrated into distribution models. These technologies enable real-time data reporting, automated compliance monitoring, and predictive analytics, enhancing operational efficiency and traceability across complex food supply chains.

End-User Insights

Food manufacturers and animal feed producers account for the largest share of demand in the mycotoxin testing market, driven by mandatory regulatory compliance, internal quality assurance programs, and export certification requirements. Large manufacturers increasingly adopt a dual testing approach, combining rapid in-house screening with third-party confirmatory analysis to reduce risk and improve turnaround time.

Contract testing laboratories represent a critical end-user group, serving both multinational corporations and small-scale producers. These laboratories invest heavily in advanced instrumentation and accreditation to meet diverse regulatory standards across regions, reinforcing their importance in the global testing ecosystem. Government agencies and research institutions utilize mycotoxin testing platforms for food safety surveillance, agricultural monitoring, and policy enforcement. Their role is expanding as countries strengthen national food safety systems and increase monitoring frequency to protect public health and support international trade.

Explore more data points, trends and opportunities Download Free Sample Report

Mycotoxin Testing Market Segmentations

By Product Type

- Chromatography-Based Testing

- Immunoassay-Based Testing

- PCR-Based Mycotoxin Detection

- Biosensors & Emerging Rapid Testing Technologies

By Application

- Food Testing

- Animal Feed Testing

- Grain & Cereal Testing

- Dairy, Spices, Nuts & Infant Food Testing

- Environmental & Agricultural Surveillance

By Distribution Channel

- Contract Testing Laboratories

- Direct B2B Sales to Food & Feed Manufacturers

- Rapid Test Kit & Consumables Distribution

- Digital, IoT-Enabled & Remote Monitoring Platforms

Regional Insights

North America

North America holds the largest market share, accounting for approximately 33% of global revenue in 2025, led by the United States and Canada. Regional growth is driven by stringent enforcement of FDA and USDA regulations, well-established laboratory infrastructure, and high consumer awareness regarding food safety risks. The region’s strong export orientation for grains, nuts, and processed foods further fuels demand for both rapid screening and confirmatory testing. Continuous investment in advanced analytical technologies and digital compliance systems reinforces North America’s market leadership.

Europe

Europe represents around 28% of the global market, with Germany, France, and the UK as major contributors. Growth in this region is driven by strict EFSA regulations, harmonized EU food safety standards, and rigorous import-export controls. High consumer expectations for food quality and transparency compel manufacturers to adopt frequent and multi-mycotoxin testing. The increasing adoption of multiplex and rapid testing technologies alongside traditional chromatography reflects Europe’s focus on efficiency without compromising regulatory compliance.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, driven by China, India, Japan, and Southeast Asian countries. Key growth drivers include the rapid expansion of agricultural exports, the strengthening of food safety regulations, and rising domestic consumption of processed foods. Government-led investments in laboratory infrastructure, coupled with growing awareness among producers and consumers, are accelerating adoption. The region also benefits from increasing use of cost-effective rapid testing solutions to bridge infrastructure gaps, making it a strategic growth hub for global players.

Latin America

Latin America accounts for approximately 9–10% of the global market, with Brazil, Argentina, and Mexico leading regional demand. Growth is primarily driven by export-oriented agriculture, particularly grains, oilseeds, and nuts destined for North American and European markets. To meet stringent import requirements, producers increasingly rely on contract laboratories and partnerships with international testing service providers, supporting steady regional expansion.

Middle East & Africa

The Middle East & Africa region holds a 6–7% market share and is gradually developing. Growth drivers include rising food imports, improving regulatory frameworks, and targeted investments in food safety infrastructure across Gulf countries and South Africa. Intra-regional trade and export compliance programs are expanding, while government initiatives aimed at strengthening food security are creating incremental demand for mycotoxin testing services.

Key Players in the Mycotoxin Testing Market

- Eurofins Scientific

- SGS SA

- Intertek Group plc

- Bureau Veritas

- Neogen Corporation

- Mérieux NutriSciences

- Romer Labs

- ALS Limited

- Asurequality

- Microbac Laboratories

- Agilent Technologies

- PerkinElmer Inc.

- R-Biopharm AG

- Symbio Laboratories

- Fera Science Limited