Ice Cream Flavors Market Size

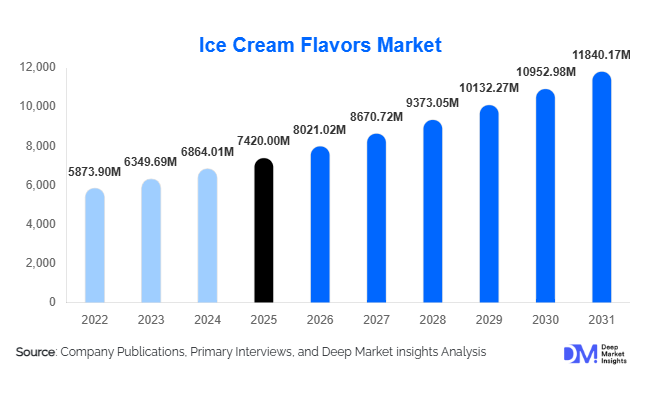

According to Deep Market Insights, the global ice cream flavors market size was valued at USD 7420 million in 2025 and is projected to grow from USD 8021.02 million in 2026 to reach USD 11840.17 million by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The ice cream flavors market growth is driven by rising global ice cream consumption, increasing demand for premium and artisanal products, rapid flavor innovation, and growing consumer preference for regionally inspired, clean-label, and functional flavor profiles.

Key Market Insights

- Traditional flavors such as vanilla and chocolate continue to dominate volume demand, serving as foundational bases for both single-flavor and blended formulations.

- Premium and dessert-inspired flavors are witnessing strong growth, supported by indulgence-driven consumption and higher disposable incomes.

- Asia-Pacific leads global growth momentum, driven by expanding middle-class populations and rising urbanization.

- Clean-label and natural flavor extracts are gaining traction amid regulatory scrutiny on artificial additives.

- Foodservice and QSR expansion is accelerating B2B demand for standardized and scalable flavor formulations.

- Technological advancements in flavor encapsulation and natural extraction are improving shelf life and taste consistency.

What are the latest trends in the ice cream flavors market?

Rise of Regional and Ethnic Flavor Profiles

Consumers are increasingly gravitating toward flavors inspired by local cuisines and cultural traditions. Regional profiles such as matcha, kulfi, ube, black sesame, and dulce de leche are transitioning from niche offerings to mainstream SKUs. Global brands are actively localizing flavor portfolios to align with regional taste preferences, while regional manufacturers are exporting ethnic flavors to international markets. This trend is strengthening flavor differentiation and supporting premium pricing strategies.

Clean-Label and Functional Flavor Innovation

Demand for clean-label ice cream flavors made using natural extracts, fruit concentrates, and plant-based ingredients is rising steadily. Botanical flavors such as ginger, turmeric, lavender, and green tea are being incorporated for both taste and perceived wellness benefits. Additionally, functional flavors supporting low-sugar, protein-enriched, and probiotic ice creams are gaining popularity, particularly in developed markets.

What are the key drivers in the ice cream flavors market?

Premiumization of Frozen Desserts

Consumers are increasingly willing to pay premium prices for indulgent ice cream experiences. Gourmet, dessert-inspired, and nut-based flavors are commanding higher margins and driving value growth. Premium ice cream brands are leveraging innovative flavor combinations to strengthen brand loyalty and differentiation.

Expansion of Modern Retail and Foodservice Channels

The rapid expansion of supermarkets, hypermarkets, and QSR chains has significantly increased the accessibility of flavored ice creams. Foodservice outlets rely heavily on standardized flavor formulations, driving bulk B2B demand for flavor manufacturers.

What are the restraints for the global market?

Volatility in Raw Material Prices

Prices of cocoa, vanilla, dairy derivatives, and natural fruit extracts remain volatile due to climate variability and supply chain disruptions. This volatility impacts formulation costs and compresses margins for flavor producers.

Regulatory Restrictions on Artificial Ingredients

Stringent regulations on artificial flavors, colors, and sweeteners—particularly in Europe and North America—are increasing compliance costs and limiting formulation flexibility for conventional flavor producers.

What are the key opportunities in the ice cream flavors industry?

Health-Oriented and Functional Flavor Development

The growing health-conscious consumer base presents opportunities for low-sugar, plant-based, and protein-enhanced ice cream flavors. Flavor developers that integrate natural sweeteners and functional ingredients can unlock premium positioning and long-term growth.

Technology-Driven Flavor Customization

Advancements in AI-based flavor profiling and micro-encapsulation technologies are enabling faster innovation cycles and improved taste stability. These technologies allow brands to test limited-edition and seasonal flavors with reduced commercialization risk.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 7420 Million |

| Market Size in 2026 | USD 8021.02 Million |

| Market Size in 2031 | USD 11840.17 Million |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Flavor Family Insights

Vanilla and plain cream flavors dominated the global market in 2025, collectively accounting for approximately 28% of total market share. Their leadership is primarily driven by their universal consumer acceptance, compatibility as base flavors for product innovation, and strong presence across both mass-market and premium offerings. These flavors are extensively used in private-label products and foodservice applications due to formulation flexibility and cost stability.

Chocolate-based flavors followed closely, supported by sustained indulgence-driven consumption, especially among adult consumers and premium product lines. Continuous innovation in cocoa intensity, origin-based chocolate profiles, and low-sugar chocolate variants has further reinforced demand.Fruit-based flavors, including strawberry, mango, and mixed tropical profiles, represent the fastest-growing flavor family. Growth is driven by increasing consumer preference for clean-label, naturally derived ingredients, and the rising appeal of refreshing and health-positioned flavor profiles. Emerging markets show particularly strong demand for regionally inspired fruit flavors.

Product Formulation Insights

Single-flavor formulations led the market with nearly 46% share in 2025, primarily due to their cost efficiency, ease of large-scale manufacturing, and consistent flavor performance. These formulations are widely adopted by industrial manufacturers and private-label brands focused on high-volume production.

Blended and multi-flavor formulations are gaining momentum within premium, artisanal, and experiential product categories. The leading growth driver for this segment is rising consumer interest in complex flavor profiles and novel taste experiences, particularly in urban and developed markets.Seasonal and limited-edition formulations are increasingly used as strategic brand engagement tools. These offerings support higher margins and enable manufacturers to respond quickly to evolving consumer trends and regional flavor preferences.

Application Format Insights

Hard ice cream remains the dominant application format, accounting for approximately 41% of total demand in 2025. Its market leadership is supported by extended shelf life, well-established cold-chain infrastructure, and broad availability across modern retail formats.Soft serve and gelato formats are expanding rapidly, particularly through foodservice, café, and dessert parlors. The key growth driver for these formats is the expansion of experiential dining, rising urban footfall, and increasing consumer willingness to pay for freshly prepared and premium-textured products.

Distribution Channel Insights

Retail channels accounted for nearly 58% of total market demand in 2025, supported by expanding modern trade, private-label penetration, and strong freezer placement in supermarkets and hypermarkets. Retail dominance is reinforced by consistent consumer purchasing behavior and promotional pricing strategies.

Foodservice channels represent the fastest-growing distribution segment. Growth is driven by the rapid expansion of quick-service restaurants (QSRs), café chains, and dessert-focused outlets, particularly in urban and tourist-heavy locations.Industrial B2B demand is rising steadily through private-label manufacturing, contract production, and export-oriented operations, especially in regions with cost-efficient production capabilities.

Consumer Group Insights

Adult consumers constitute the largest consumption segment, contributing approximately 55% of total demand. This dominance is driven by increasing preference for premium, indulgent, and specialty flavors, as well as growing interest in artisanal and functional variants.Children-focused products remain volume-driven, supported by classic flavors and price-sensitive offerings. Meanwhile, health-conscious consumers are emerging as a high-growth segment, accelerating demand for low-sugar, reduced-fat, and functional formulations enriched with probiotics or natural ingredients.

Explore more data points, trends and opportunities Download Free Sample Report

Ice Cream Flavors Market Segmentations

By Flavor Family

- Vanilla & Plain Cream

- Chocolate-Based

- Fruit-Based

- Nut-Based

- Caramel & Toffee

- Coffee & Tea-Based

- Dessert-Inspired Flavors

- Regional & Ethnic Flavors

- Functional & Novelty Flavors

By Product Formulation

- Single-Flavor Formulations

- Blended / Multi-Flavor Formulations

- Seasonal & Limited-Edition Flavors

By Nature

- Conventional

- Organic

- Clean-Label / Natural Extract-Based

By Application Format

- Hard Ice Cream

- Soft Serve

- Gelato

- Sorbet & Sherbet

- Frozen Desserts & Novelties

By Distribution Channel

- Retail / Off-Trade

- Foodservice / HoReCa

- Industrial / B2B

Regional Insights

North America

North America accounted for approximately 29% of global market share in 2025, led primarily by the United States. Regional growth is driven by strong demand for premium, organic, and functional flavor variants, alongside high consumer awareness of ingredient transparency. Continuous innovation in plant-based and low-sugar formulations further supports market expansion.

Europe

Europe held nearly 26% of the global market, with Germany, France, Italy, and the U.K. as key contributors. Growth drivers include strict regulatory emphasis on clean-label compliance, strong artisanal ice cream traditions, and rising demand for natural and origin-specific flavor profiles. Sustainability-focused sourcing is also influencing formulation strategies.

Asia-Pacific

Asia-Pacific emerged as the fastest-growing region, accounting for approximately 31% of global demand in 2025. Rapid urbanization, rising disposable incomes, and expanding cold-chain infrastructure in China, India, and Japan are key growth drivers. Increasing exposure to Western-style desserts combined with strong demand for localized flavors further accelerates regional market expansion.

Latin America

Latin America is driven by Brazil and Mexico, where strong consumer preference for fruit-based and regionally inspired flavors supports demand. Growth is further fueled by improving retail penetration, expanding middle-class populations, and increasing export-oriented manufacturing capabilities.

Middle East & Africa

The Middle East & Africa region is experiencing steady growth, supported by rising tourism, expanding foodservice infrastructure, and premium retail development in the UAE, Saudi Arabia, and South Africa. Increasing adoption of Western dessert formats and growing demand for indulgent and exotic flavors are key regional growth drivers.

Key Players in the Ice Cream Flavors Market

- Givaudan

- Firmenich

- International Flavors & Fragrances (IFF)

- Symrise

- Kerry Group

- Takasago

- Sensient Technologies

- Mane

- T. Hasegawa

- Döhler

- Robertet Group

- Bell Flavors & Fragrances

- Flavorchem

- Aromatech

- Huabao International