Flavour Enhancer Market Size

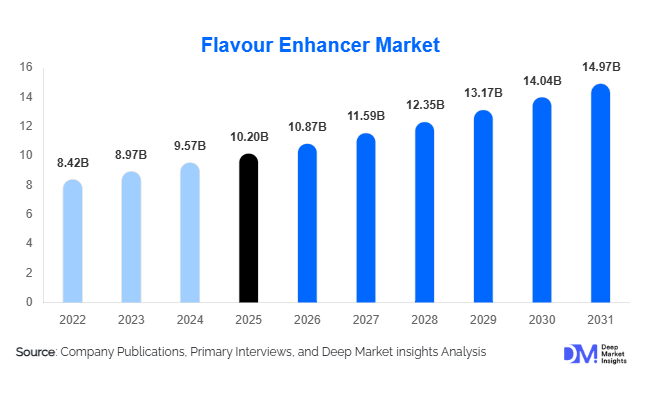

According to Deep Market Insights, the global flavour enhancer market size was valued at USD 10.2 billion in 2025 and is projected to grow from USD 10.87 billion in 2026 to reach USD 14.97 billion by 2031, expanding at a CAGR of 6.6% during the forecast period (2026–2031). The flavour enhancer market growth is primarily driven by the rising consumption of processed and convenience foods, increasing demand for taste optimization in cost-sensitive food formulations, and rapid innovation in fermentation-based and clean-label flavour enhancement technologies.

Key Market Insights

- Monosodium glutamate (MSG) remains the single largest product segment, supported by its cost efficiency, high umami intensity, and widespread adoption in Asian cuisines.

- Natural and fermentation-derived flavour enhancers are gaining rapid traction, driven by clean-label trends and regulatory scrutiny over synthetic additives.

- Asia-Pacific dominates global consumption, accounting for nearly half of total market demand due to traditional culinary usage and large-scale manufacturing capacity.

- Food and beverage processors represent the largest end-use segment, benefiting from long-term supply contracts and high-volume requirements.

- Sodium-reduction and plant-based reformulation initiatives are increasing reliance on advanced enhancer systems.

- Technological advancements in biotechnology and enzymatic processing are reshaping competitive differentiation and product portfolios.

What are the latest trends in the flavour enhancer market?

Shift Toward Natural and Clean-Label Enhancers

The flavour enhancer market is witnessing a structural shift toward natural and nature-identical solutions, particularly yeast extracts, fermented vegetable concentrates, and nucleotide blends. Food manufacturers are reformulating products to eliminate artificial additives while preserving taste intensity, positioning natural flavour enhancers as a premium yet scalable alternative. This trend is especially prominent in North America and Europe, where regulatory oversight and consumer awareness are accelerating adoption. Fermentation-derived enhancers are also gaining popularity due to their sustainability credentials and consistent quality profiles.

Flavour Enhancement for Sodium and Sugar Reduction

One of the most significant trends shaping the market is the integration of flavour enhancers into salt- and sugar-reduction strategies. Advanced umami systems enable manufacturers to reduce sodium content without compromising taste, supporting compliance with public health guidelines. This trend is expanding the role of flavour enhancers beyond taste improvement into nutritional optimization, particularly in ready meals, snacks, and processed meats.

What are the key drivers in the flavour enhancer market?

Rising Demand for Processed and Convenience Foods

Urbanization, changing lifestyles, and increasing working populations have fueled global demand for ready-to-eat meals, snacks, sauces, and instant foods. Flavour enhancers are essential for maintaining taste consistency, extending shelf life, and compensating for flavor loss during processing, making them indispensable to modern food manufacturing.

Cost Optimization and Margin Protection

Flavour enhancers allow manufacturers to reduce reliance on expensive raw materials such as meat, spices, and natural extracts while maintaining sensory appeal. This cost-optimization advantage has become increasingly important amid volatile agricultural input prices, driving sustained demand across both developed and emerging markets.

Technological Advancements in Fermentation

Advances in microbial fermentation, enzymatic hydrolysis, and biotechnology have significantly improved yield efficiency and flavor precision. These innovations enable the development of high-potency enhancers with cleaner labels, strengthening market expansion across premium and mass-market food segments.

What are the restraints for the global market?

Regulatory and Perception Challenges

Despite scientific consensus on safety, MSG and synthetic flavour enhancers continue to face consumer skepticism in certain regions. Regulatory labeling requirements and negative perceptions can restrict adoption, particularly in premium and health-focused food categories.

Raw Material Price Volatility

Fluctuations in prices of sugar substrates, molasses, and agricultural feedstocks used in fermentation processes impact production costs and profitability. Manufacturers without long-term supply agreements are particularly vulnerable to margin pressure.

What are the key opportunities in the flavour enhancer industry?

Expansion of Natural and Fermentation-Based Solutions

Growing demand for clean-label foods presents significant opportunities for manufacturers investing in bio-fermentation technologies. Natural enhancers offer higher margins and regulatory flexibility, enabling suppliers to secure long-term partnerships with multinational food producers.

Emerging Market Demand and Regional Customization

Rapid growth in Asia-Pacific, Africa, and Latin America presents opportunities for localized flavour enhancer formulations aligned with regional taste profiles. Customization strategies reduce commoditization and enhance customer loyalty.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 10.2 Billion |

| Market Size in 2026 | USD 10.87 Billion |

| Market Size in 2031 | USD 14.97 Billion |

| CAGR | 6.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Monosodium glutamate (MSG) dominates the global flavour enhancer market, accounting for approximately 38% of total demand in 2025. Its leadership is driven by low production cost, high flavour-enhancing efficacy, and widespread acceptance across mass-produced savory foods, particularly in Asia-Pacific and emerging economies. MSG remains a preferred choice for manufacturers seeking consistent umami intensity at scale.

Yeast extracts represent the fastest-growing product segment, supported by strong clean-label positioning, natural fermentation origins, and increasing use in premium, organic, and reduced-sodium food formulations. Food manufacturers are increasingly substituting synthetic enhancers with yeast-based alternatives to meet regulatory and consumer transparency expectations.Hydrolyzed vegetable proteins (HVPs) and nucleotide blends are gaining traction in processed meats, soups, sauces, and instant foods, where they are valued for enhancing umami depth, mouthfeel, and overall flavor complexity. Growth in this segment is driven by the expanding ready-meal market and rising demand for cost-effective flavour optimization solutions.

Application Insights

Savory foods constitute the largest application segment, capturing nearly 44% of the global flavour enhancer market. The segment’s dominance is driven by high consumption of instant noodles, processed meats, soups, and frozen meals, where flavour enhancers are essential for taste consistency and sensory appeal.Snacks and convenience foods follow closely, supported by rapid urbanization, busy lifestyles, and growing demand for ready-to-eat products. Meanwhile, sauces, dressings, and ready meals are emerging as high-growth applications, benefiting from increasing global packaged food consumption and the expansion of quick-service restaurants (QSRs) and foodservice chains.

End-Use Industry Insights

Food and beverage processing dominates end-use demand, accounting for approximately 68% of total market share. This leadership is supported by large-scale industrial food production, private-label manufacturing, and export-oriented processing facilities that rely heavily on flavour enhancers for product standardization.Foodservice operators are increasingly adopting customized flavour enhancer blends to maintain consistent taste profiles across multi-location outlets, particularly in fast food and casual dining formats. Additionally, the pet food industry is emerging as a niche growth area, driven by rising pet ownership and increasing focus on palatability and nutritional appeal.

Form Insights

Powdered flavour enhancers account for over 60% of global consumption, owing to their longer shelf life, ease of storage, cost efficiency, and compatibility with automated industrial processing systems. Powdered forms are widely used in dry mixes, seasonings, and instant food products.Liquid and paste forms are gaining traction, particularly in sauces, dressings, and ready-to-eat applications that require rapid solubility and uniform dispersion. Growth in these formats is supported by rising demand from foodservice kitchens and premium prepared food manufacturers.

Explore more data points, trends and opportunities Download Free Sample Report

Flavour Enhancer Market Segmentations

By Product Type

- Monosodium Glutamate (MSG)

- Yeast Extracts

- Hydrolyzed Vegetable Protein (HVP)

- Disodium Inosinate & Disodium Guanylate

- Other Flavour Enhancers (Nucleotide Blends, Kokumi Peptides)

By Source

- Natural

- Nature-Identical

- Synthetic

By Form

- Powder

- Liquid

- Granules / Paste

By Application

- Savory Foods

- Snacks & Convenience Foods

- Meat & Seafood Products

- Sauces, Dressings & Condiments

- Soups & Ready Meals

By End-Use Industry

- Food & Beverage Processing

- Foodservice (QSRs, Restaurants, Catering)

- Household / Retail Consumption

- Pet Food Industry

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global flavour enhancer market, accounting for approximately 46% of total demand in 2025. The region benefits from deep-rooted culinary traditions centered on umami-rich ingredients, combined with large-scale MSG production capacity in China, Japan, South Korea, Indonesia, and Thailand.Regional growth is driven by expanding food processing industries, rising disposable incomes, and increasing exports of processed foods. India represents the fastest-growing market, supported by rapid industrialization, government initiatives promoting food manufacturing, and growing demand for packaged and ready-to-eat foods.

North America

North America accounts for approximately 21% of global flavour enhancer demand, led primarily by the United States. Growth in the region is driven by strong packaged food consumption, an expanding foodservice sector, and innovation in low-sodium and clean-label flavour solutions.Manufacturers are increasingly adopting natural, yeast-based, and fermentation-derived enhancers to comply with regulatory standards and evolving consumer preferences for healthier food products.

Europe

Europe holds nearly 18% of the global market share, with Germany, France, and the United Kingdom as key contributors. The region’s growth is shaped by stringent food safety regulations, high clean-label awareness, and demand for sustainable and traceable ingredients.Adoption of yeast extracts and plant-based flavour enhancers is accelerating as manufacturers reformulate products to meet regulatory compliance and consumer demand for natural alternatives.

Latin America

Latin America represents around 7% of the global flavour enhancer market, led by Brazil and Mexico. Growth is supported by rising urban populations, increasing consumption of processed foods, and expanding food manufacturing infrastructure.Export-oriented food production and growing trade ties with North America are further driving demand for flavour enhancers across the region.

Middle East & Africa

The Middle East & Africa accounts for approximately 8% of global demand. Growth in the region is driven by rising packaged food imports, rapid expansion of foodservice outlets, and increasing adoption of Western-style diets.Countries such as Saudi Arabia, the UAE, and South Africa are key growth markets, supported by urbanization, tourism-driven foodservice demand, and investments in local food processing capacity.

Key Players in the Flavour Enhancer Market

- Ajinomoto Co., Inc.

- Kerry Group plc

- DSM-Firmenich

- Givaudan SA

- Tate & Lyle PLC

- Sensient Technologies

- Angel Yeast Co., Ltd.

- Fufeng Group

- Meihua Holdings Group

- Lesaffre Group

- CJ CheilJedang

- Lallemand Inc.

- Novozymes

- Synergy Flavors

- Vedan International