Filling Equipment Market Size

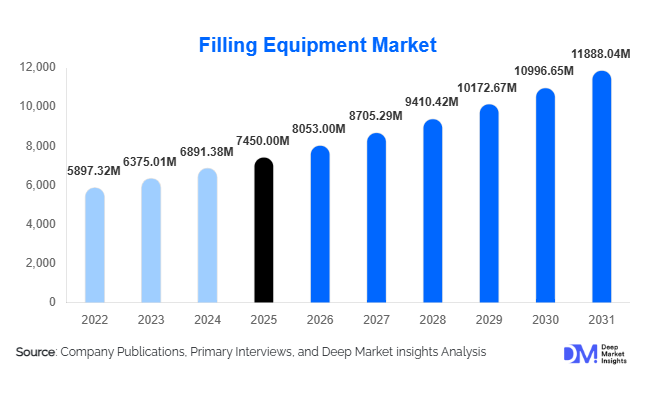

According to Deep Market Insights, the global filling equipment market was valued at USD 7,450 million in 2025 and is projected to grow from USD 8,053.45 million in 2026 to reach USD 11,888.04 million by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The market growth is primarily driven by the increasing demand for automated packaging solutions across the food & beverage, pharmaceutical, and cosmetic industries, the adoption of advanced filling technologies, and the rising trend of production line optimization to improve operational efficiency.

Key Market Insights

- Automation and smart technologies are transforming the filling equipment landscape, enabling manufacturers to improve precision, reduce product wastage, and increase throughput.

- Pharmaceutical and biotech sectors are driving demand for hygienic and aseptic filling systems, particularly for injectable drugs and vaccines requiring high sterility standards.

- Food & beverage industry dominates the market, accounting for a substantial share due to rising consumption of packaged beverages, sauces, and liquid dairy products.

- Asia-Pacific is emerging as the fastest-growing regional market, fueled by rising industrialization, growing consumer demand for packaged goods, and increased foreign investment in production facilities.

- North America holds a significant share, led by stringent regulatory compliance, technological adoption, and strong industrial CapEx investments.

- Sustainability integration, including energy-efficient machines and waste reduction technologies, is increasingly shaping manufacturer strategies globally.

What are the latest trends in the filling equipment market?

Automation and Industry 4.0 Adoption

Filling equipment manufacturers are increasingly integrating Industry 4.0 technologies, such as IoT-enabled monitoring, predictive maintenance, and AI-driven production line optimization. Automated systems enhance efficiency, minimize human errors, and ensure consistent filling accuracy. Smart sensors, real-time analytics, and remote monitoring allow operators to identify bottlenecks and optimize machine performance. This trend is particularly strong in the pharmaceutical and beverage industries, where precision and compliance are critical. Integration with ERP and MES systems is also improving end-to-end traceability and production planning.

Sustainability and Eco-Friendly Systems

Energy efficiency, water conservation, and reduced packaging waste are key considerations driving new filling equipment designs. Manufacturers are launching machines with lower energy consumption, optimized fluid handling, and recyclable material compatibility. This trend responds to regulatory pressures and growing customer demand for environmentally sustainable operations. Machines designed for multi-format packaging, such as PET, glass, and flexible pouches, further enhance material efficiency and reduce carbon footprint.

What are the key drivers in the filling equipment market?

Rising Demand in the Food & Beverage Industry

Increasing consumption of packaged beverages, dairy products, sauces, and ready-to-drink items is propelling growth in the filling equipment market. Beverage manufacturers, especially in carbonated drinks and bottled water, require high-speed, automated filling lines to meet production volumes. The expansion of retail and e-commerce channels globally also drives demand for packaged food products, directly boosting the need for efficient filling equipment.

Stringent Pharmaceutical and Hygiene Regulations

Pharmaceutical companies are investing heavily in aseptic and sterile filling machines to meet FDA, EMA, and WHO compliance standards. Injectable drugs, vaccines, and biologics require advanced filling solutions that minimize contamination risk. Regulatory compliance ensures consistent product quality and patient safety, positioning this segment as a high-growth driver in the global market.

Technological Advancements in Filling Systems

Innovations such as multi-head fillers, volumetric and piston fillers, rotary and inline systems, and robotics integration have enhanced operational efficiency and flexibility. These technologies reduce human labor, improve precision, and allow rapid format changes, which is increasingly essential for manufacturers serving multiple SKUs. Smart filling systems also support predictive maintenance and remote diagnostics, reducing downtime and operational costs.

What are the restraints for the global market?

High Initial Investment

The adoption of automated filling equipment requires significant capital expenditure, especially for advanced systems with robotics, sensors, and Industry 4.0 features. Small and medium enterprises may face challenges in affording high-end machines, limiting widespread deployment.

Complex Maintenance and Skilled Labor Requirement

Advanced filling equipment requires skilled operators and regular maintenance to ensure optimal performance. Lack of trained personnel, high maintenance costs, and downtime risks are key restraints, particularly in emerging markets where technical expertise is limited.

What are the key opportunities in the filling equipment industry?

Expansion in Emerging Markets

Rising demand for packaged food, beverages, and pharmaceuticals in Asia-Pacific, Latin America, and the Middle East presents significant growth opportunities. Countries such as India, China, Brazil, and Saudi Arabia are investing in modern manufacturing facilities, driving demand for automated and hygienic filling equipment. The opportunity lies in targeting fast-growing regional production hubs and partnering with local equipment distributors to expand market presence.

Integration with Smart Manufacturing

Companies can leverage Industry 4.0 technologies, including IoT, AI, and predictive analytics, to offer value-added solutions. Smart filling systems that enable remote monitoring, energy efficiency, and rapid SKU changeover provide a competitive edge. Early adoption of connected equipment allows manufacturers to differentiate their offerings and attract clients seeking next-generation production lines.

Sustainability-Driven Innovation

Growing regulatory pressures and corporate sustainability commitments are creating opportunities for energy-efficient, eco-friendly filling equipment. Machines optimized for minimal product wastage, recyclable packaging, and reduced energy consumption are increasingly preferred. Players who invest in sustainable product lines can capture environmentally conscious buyers while complying with global regulations.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 7450 Million |

| Market Size in 2026 | USD 8053 Million |

| Market Size in 2031 | USD 11888.04 Million |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Piston fillers lead the market, accounting for approximately 28% of the 2025 market, due to their accuracy, versatility across liquid viscosities, and suitability for both food and pharmaceutical applications. Volumetric fillers are also prominent, particularly in high-speed beverage lines, offering consistent fill volumes and reliability. Rotary and inline fillers dominate high-capacity production lines due to faster throughput, while semi-automatic and manual fillers cater to SMEs requiring lower volumes and operational simplicity.

Application Insights

Food & beverage applications hold the largest share at 45% of the market in 2025, driven by bottled water, carbonated drinks, sauces, and dairy products. Pharmaceutical applications are growing rapidly, contributing 25% due to injectable, aseptic, and liquid oral formulations. Cosmetic and personal care applications are expanding steadily, particularly in skincare and haircare products requiring precise volumetric filling. Industrial chemicals and household products form the remaining share, often using volumetric or piston filling systems to handle viscous liquids.

Distribution Channel Insights

Direct sales by manufacturers dominate, accounting for 60% of transactions, especially for large-scale clients requiring customized systems. Distributors and system integrators serve SMEs and mid-sized companies, providing turnkey solutions, installation, and after-sales services. E-commerce and online marketplaces are slowly emerging for smaller machines and spare parts, enabling faster procurement and wider geographic reach.

End-Use Insights

The food & beverage sector remains the largest end-user, driven by global demand for packaged drinks, dairy, and sauces. Pharmaceutical end-users are expanding rapidly, fueled by injectable and vaccine production. Cosmetics and personal care are emerging as high-growth segments, particularly in the Asia-Pacific. Export-driven demand is prominent in the beverage and pharmaceutical sectors, with equipment manufactured in Europe and North America increasingly exported to emerging markets, supporting cross-border industrial growth.

Explore more data points, trends and opportunities Download Free Sample Report

Filling Equipment Market Segmentations

By Product Type

- Piston Fillers

- Volumetric Fillers

- Rotary Fillers

- Inline Fillers

- Semi-Automatic & Manual Fillers

By Application

- Food & Beverage

- Pharmaceuticals

- Cosmetics & Personal Care

- Industrial & Household Chemicals

By Distribution Channel

- Direct Sales

- Distributors & System Integrators

- Online Platforms & E-commerce

Regional Insights

North America

North America accounts for 28% of the global filling equipment market in 2025. The U.S. leads with strong pharmaceutical and food & beverage industries, high automation adoption, and stringent regulatory compliance. Canada is smaller but growing steadily, driven by the beverage manufacturing and cosmetic industries. The region’s mature infrastructure and high CapEx spending support consistent growth.

Europe

Europe holds 25% of the market, with Germany, Italy, and France dominating. Strong industrial automation, compliance with EU regulations, and advanced manufacturing capabilities drive demand. Germany is the hub for equipment innovation, particularly in high-speed bottling lines. The region is also witnessing moderate growth due to sustainability regulations and retrofitting of older lines.

Asia-Pacific

APAC is the fastest-growing region (12% CAGR), with China, India, and Japan leading. Industrialization, urbanization, and rising packaged goods consumption are fueling demand. China dominates in sheer volume, while India is emerging as a manufacturing hub with government initiatives such as “Make in India” supporting investment in automated equipment. Japan focuses on high-precision pharmaceutical filling technologies.

Latin America

Brazil, Mexico, and Argentina are key markets. Growth is moderate but steady, supported by beverage production and cosmetic manufacturing. Industrial modernization is accelerating equipment adoption, especially automated piston and volumetric fillers.

Middle East & Africa

Demand in the Middle East is rising due to food & beverage processing investments in Saudi Arabia and the UAE. Africa’s growth is slower but promising in South Africa, Egypt, and Kenya, where beverage, dairy, and pharmaceutical production is expanding. Export-driven demand from Europe and Asia contributes significantly.

Key Players in the Filling Equipment Market

- IMA Group

- ProMach

- GEA Group

- Krones AG

- Coesia S.p.A.

- Optima Packaging Group

- Bosch Packaging Technology

- Filamatic

- All-Fill Inc.

- Robert Bosch GmbH

- Barry-Wehmiller

- Serac Group

- CFT Group

- Multipack Systems

- Sidel Group