Digestive Enzyme Supplements Market Size

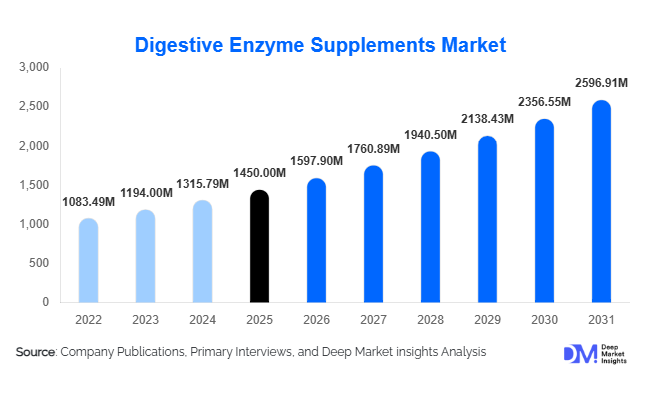

According to Deep Market Insights, the global digestive enzyme supplements market size was valued at USD 1450 million in 2025 and is projected to grow from USD 1597.90 million in 2026 to reach USD 2596.91 million by 2031, expanding at a CAGR of 10.2% during the forecast period (2026–2031). The digestive enzyme supplements market growth is primarily driven by the rising prevalence of digestive disorders, increasing awareness of gut health and preventive nutrition, and the rapid expansion of the global nutraceutical and dietary supplements industry.

Key Market Insights

- Digestive enzyme supplements are increasingly used as preventive healthcare products, supported by growing consumer focus on gut health, immunity, and metabolic wellness.

- Microbial- and plant-derived enzymes dominate product development, driven by demand for vegan, clean-label, and allergen-free formulations.

- North America leads global consumption, supported by high dietary supplement penetration and strong clinical nutrition demand.

- Asia-Pacific is the fastest-growing region, fueled by rising disposable income, urbanization, and increasing digestive health awareness in China and India.

- Online and direct-to-consumer channels are expanding rapidly, driven by subscription models and personalized nutrition platforms.

- Technological advancements in microbial fermentation, encapsulation, and enzyme stabilization are improving product efficacy and shelf life.

What are the latest trends in the digestive enzyme supplements market?

Shift Toward Plant-Based and Clean-Label Enzymes

Consumers are increasingly favoring plant- and microbial-derived digestive enzymes over animal-based alternatives due to ethical, dietary, and sustainability considerations. This trend is accelerating the adoption of vegan-certified and non-GMO enzyme supplements, particularly in North America and Europe. Manufacturers are reformulating products to remove allergens, artificial additives, and synthetic excipients, positioning clean-label enzymes as premium offerings. Transparent labeling and traceable sourcing are becoming critical brand differentiators, driving higher consumer trust and repeat purchases.

Integration with Personalized Nutrition and Gut Health Platforms

Digestive enzyme supplements are increasingly integrated into personalized nutrition programs supported by gut microbiome testing, AI-driven diet planning, and DNA-based wellness assessments. Subscription-based enzyme supplementation tailored to individual digestive needs is gaining traction, particularly among urban consumers. This trend is expanding average order values and strengthening long-term customer engagement. Digital health platforms and nutraceutical brands are partnering to bundle enzyme supplements with probiotics, prebiotics, and functional fibers, reinforcing holistic gut health positioning.

What are the key drivers in the digestive enzyme supplements market?

Rising Prevalence of Digestive Disorders

The increasing incidence of lactose intolerance, irritable bowel syndrome (IBS), acid reflux, and enzyme insufficiencies is a major growth driver. Modern diets high in processed foods, combined with sedentary lifestyles and stress, have increased digestive discomfort across age groups. Digestive enzyme supplements offer convenient, non-prescription solutions, driving widespread adoption among preventive and therapeutic users.

Growth of the Global Nutraceutical Industry

The rapid expansion of the nutraceutical and functional food sector has significantly boosted demand for digestive enzymes. These supplements are increasingly incorporated into protein powders, meal replacements, and clinical nutrition formulations. Their compatibility with sports nutrition and elderly care products is further expanding the addressable market.

What are the restraints for the global market?

Regulatory Inconsistencies Across Regions

Digestive enzyme supplements face varying regulatory classifications across regions, ranging from food supplements to therapeutic products. This creates compliance challenges, increases approval timelines, and raises development costs for global manufacturers.

Price Sensitivity in Emerging Markets

In price-sensitive markets, premium enzyme formulations may be perceived as non-essential. Limited reimbursement coverage and lower physician recommendations in some regions can slow adoption, particularly among lower-income consumer groups.

What are the key opportunities in the digestive enzyme supplements industry?

Expansion in Emerging Markets

Rapid urbanization, westernization of diets, and rising healthcare awareness in emerging economies such as India, China, Brazil, and Southeast Asia present strong growth opportunities. Local manufacturing under initiatives such as “Make in India” is improving affordability and market penetration.

Clinical Nutrition and Geriatric Care Applications

Increasing use of digestive enzymes in hospitals, long-term care facilities, and geriatric nutrition presents a high-growth opportunity. Enzymes are increasingly prescribed for post-surgical recovery, chronic digestive conditions, and age-related enzyme deficiencies.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1450 Million |

| Market Size in 2026 | USD 1597.90 Million |

| Market Size in 2031 | USD 2596.91 Million |

| CAGR | 10.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Multi-enzyme blends dominate the global digestive enzyme supplements market, accounting for approximately 42% of total demand. Their leadership is driven by their ability to address multiple digestive challenges, such as protein, carbohydrate, fat, and lactose digestion, within a single formulation, making them highly attractive for general wellness consumers and aging populations. The growing prevalence of complex digestive disorders and the rising preference for all-in-one gut health solutions continue to strengthen demand for multi-enzyme products.

Single-enzyme supplements, including lactase, protease, and amylase, maintain strong adoption among consumers with specific food intolerances, such as lactose intolerance or protein malabsorption. These products benefit from targeted clinical recommendations and increasing diagnostic awareness of digestive enzyme deficiencies.By source, microbial-derived enzymes represent the leading category due to their superior stability across varying pH levels, cost-effective large-scale production, and compatibility with vegetarian and vegan formulations. The shift toward plant-based diets and clean-label supplements further reinforces the dominance of microbial enzyme sources.

Dosage Form Insights

Capsules remain the most widely used dosage form, representing nearly 46% of the global market. Their dominance is driven by ease of consumption, precise dosing, improved bioavailability, and longer shelf life. Encapsulation technologies also enable delayed-release and enteric-coated formulations, enhancing enzyme effectiveness in targeted areas of the digestive tract.

Powders and chewable formats are gaining traction, particularly among pediatric, sports nutrition, and lifestyle consumers who prefer customizable dosing and flavor-enhanced delivery. These formats benefit from increasing use in protein blends, meal replacements, and functional beverages.Liquid digestive enzyme formulations are increasingly adopted in clinical nutrition, geriatric care, and hospital settings due to faster absorption and ease of administration for patients with swallowing difficulties, supporting steady niche growth.

Distribution Channel Insights

Pharmacies and drug stores continue to dominate the distribution landscape, supported by strong consumer trust, pharmacist guidance, and physician recommendations for digestive health management. These outlets remain particularly important for therapeutic and clinically positioned enzyme supplements.

Online retail and direct-to-consumer (DTC) platforms represent the fastest-growing distribution channels, driven by subscription-based purchasing models, personalized nutrition solutions, aggressive digital marketing, and expanding e-commerce penetration. Convenience, wider product availability, and price transparency further accelerate online adoption.Specialty health and wellness stores play a critical role in premium, organic, and practitioner-recommended digestive enzyme supplements, particularly among health-conscious consumers seeking clean-label and customized formulations.

End-Use Insights

Dietary supplement consumers account for over 60% of total market demand, driven by the growing emphasis on preventive healthcare, gut microbiome awareness, and rising self-care practices. Daily digestive support products remain the primary revenue contributor within this segment.

Clinical nutrition and therapeutic applications represent the fastest-growing end-use segment, supported by increasing hospital admissions related to gastrointestinal disorders, aging populations, and the rising use of enzyme therapy in post-surgical and chronic digestive condition management.Sports nutrition and pediatric nutrition are emerging as niche, high-growth segments. In sports nutrition, enzymes are increasingly incorporated to improve nutrient absorption and recovery, while pediatric applications benefit from rising awareness of childhood digestive sensitivities and food intolerances.

Explore more data points, trends and opportunities Download Free Sample Report

Digestive Enzyme Supplements Market Segmentations

By Enzyme Type

- Proteases

- Amylases

- Lipases

- Lactase

- Cellulase

- Multi-Enzyme Blends

By Source

- Animal-Derived Enzymes

- Plant-Derived Enzymes

- Microbial-Derived Enzymes

By Dosage Form

- Capsules

- Tablets

- Powders

- Liquids & Drops

- Chewables

By Functionality

- General Digestive Health

- Lactose Intolerance Management

- Protein Digestion Support

- Fat Digestion Support

- Gut Microbiome & IBS Support

By Distribution Channel

- Pharmacies & Drug Stores

- Supermarkets & Hypermarkets

- Online Retail & Direct-to-Consumer

- Specialty Health & Nutrition Stores

By End Use

- Dietary Supplement Consumers

- Clinical Nutrition & Therapeutic Use

- Sports Nutrition

- Pediatric & Geriatric Nutrition

Regional Insights

North America

North America accounts for approximately 34% of the global digestive enzyme supplements market, led by the United States. Regional growth is driven by high supplement consumption rates, widespread awareness of gut health, and a well-established preventive healthcare culture. Strong product innovation, physician-recommended supplementation, and the presence of leading nutraceutical brands further support sustained demand. Canada contributes steadily, supported by clean-label preferences and growing interest in digestive wellness.

Europe

Europe holds nearly 27% of the global market share, with Germany, the U.K., France, and Italy serving as key revenue contributors. Growth is supported by aging populations, rising prevalence of digestive disorders, and stringent regulatory standards that reinforce consumer trust in supplement quality. Increasing demand for organic, non-GMO, and clean-label enzyme products further accelerates regional adoption.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at a CAGR exceeding 12%. Growth is driven by rapid urbanization, dietary transitions, rising disposable incomes, and increasing awareness of digestive health. China leads regional consumption due to expanding middle-class populations and e-commerce penetration, while India is the fastest-growing country, supported by expanding local manufacturing, traditional digestive health awareness, and government initiatives promoting nutraceutical production.

Latin America

Latin America accounts for approximately 7% of the global market, led by Brazil and Mexico. Regional growth is driven by improving healthcare access, increasing consumer awareness of digestive wellness, and the expansion of organized retail pharmacy chains. Rising adoption of dietary supplements among urban populations further supports market expansion.

Middle East & Africa

The Middle East & Africa region represents around 5% of the global market, with demand concentrated in the UAE, Saudi Arabia, and South Africa. Growth is supported by rising healthcare expenditure, increasing prevalence of lifestyle-related digestive disorders, and growing demand for premium imported supplements among high-income consumers. Gradual improvements in healthcare infrastructure are expected to sustain long-term growth.

Key Players in the Digestive Enzyme Supplements Market

- Nestlé Health Science

- Abbott Laboratories

- Amway

- Garden of Life

- NOW Foods

- Herbalife Nutrition

- Blackmores

- Nature’s Bounty

- Danone

- Enzymedica

- Integrative Therapeutics

- Jamieson Wellness

- BioGaia

- Pharmavite

- Himalaya Wellness