Delivery Robot Market Size

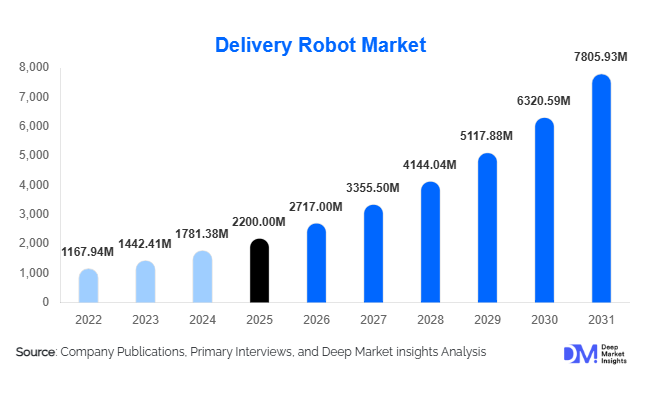

According to Deep Market Insights, the global delivery robot market size was valued at USD 2,200 million in 2025 and is projected to grow from USD 2,717.00 million in 2026 to reach USD 7,805.93 million by 2031, expanding at a CAGR of 23.5% during the forecast period (2026–2031). The delivery robot market growth is primarily driven by rising last-mile delivery automation demand, increasing labor shortages across logistics and food services, and rapid advancements in autonomous navigation, artificial intelligence, and sensor technologies.

Key Market Insights

- Ground-based delivery robots dominate the market, driven by widespread adoption in food delivery, campus logistics, and urban last-mile applications.

- Fully autonomous robots are gaining rapid traction as AI-enabled navigation systems reduce the need for human supervision and improve scalability.

- North America leads global adoption, supported by favorable regulations, strong venture funding, and early commercialization.

- Asia-Pacific is the fastest-growing region, driven by smart city initiatives, dense urban populations, and aggressive automation strategies.

- Food & beverage delivery remains the largest application, accounting for the highest revenue contribution in 2025.

- Hybrid navigation technologies combining LiDAR, vision, and GPS are becoming the industry standard for urban deployments.

What are the latest trends in the delivery robot market?

Rapid Commercialization of Autonomous Last-Mile Delivery

Delivery robots are transitioning from pilot-stage deployments to commercial-scale operations across urban neighborhoods, university campuses, and mixed-use developments. Food delivery platforms, e-commerce players, and logistics providers are increasingly integrating robot fleets to reduce last-mile delivery costs and improve service efficiency. Fleet-based deployment models, supported by centralized command centers and AI-driven routing software, are becoming mainstream. Cities with established regulatory frameworks are witnessing sustained rollouts, signaling a shift from experimentation toward revenue-generating autonomous delivery ecosystems.

Software-Driven Differentiation and Fleet Intelligence

Technology adoption is increasingly focused on software rather than hardware alone. Vendors are embedding AI-powered fleet orchestration, predictive maintenance, real-time analytics, and cloud-based monitoring platforms to enhance operational efficiency. Subscription-based software services and long-term service contracts are emerging as key revenue streams. Integration with IoT systems, e-commerce platforms, and food ordering applications is further strengthening the value proposition of delivery robots, particularly for enterprise customers managing large-scale deployments.

What are the key drivers in the delivery robot market?

Growing Demand for Last-Mile Automation

The rapid expansion of e-commerce and on-demand food delivery services has intensified pressure on last-mile logistics, the most expensive and labor-intensive segment of the supply chain. Delivery robots offer a cost-effective alternative by enabling short-distance, high-frequency deliveries without human couriers. Their ability to operate continuously and navigate dense urban environments makes them particularly attractive for last-mile optimization, driving strong adoption across developed and emerging economies.

Labor Shortages and Rising Operating Costs

Persistent labor shortages and rising wage costs in logistics, healthcare, and food services are accelerating automation investments. Delivery robots help organizations mitigate workforce challenges by reducing dependency on human delivery personnel. This driver is especially prominent in North America, Europe, and parts of Asia-Pacific, where demographic shifts and workforce attrition are increasing operational costs for service providers.

What are the restraints for the global market?

Regulatory Fragmentation and Compliance Complexity

Delivery robots operate in public and semi-public spaces, making them subject to varying local regulations related to pedestrian safety, sidewalk usage, and data privacy. Regulatory inconsistency across cities and countries increases deployment complexity and slows scaling for global vendors. Obtaining approvals for autonomous operations remains a key challenge, particularly in regions with strict urban mobility regulations.

High Initial Capital Investment

Despite long-term cost savings, delivery robots require significant upfront investment in hardware, infrastructure integration, and fleet management systems. Small and mid-sized businesses may hesitate to adopt robotic delivery without clearly defined return-on-investment timelines, limiting penetration in cost-sensitive customer segments.

What are the key opportunities in the delivery robot industry?

Healthcare and Pharmaceutical Logistics Automation

Hospitals, medical campuses, and pharmaceutical facilities are increasingly adopting delivery robots for the secure transport of medicines, lab samples, and medical supplies. This segment offers high-margin opportunities due to predictable demand, regulatory compliance requirements, and lower price sensitivity. Indoor and campus-based robots tailored for sterile environments are gaining strong traction, positioning healthcare logistics as a major growth avenue.

Smart City and Public Infrastructure Integration

Government-backed smart city initiatives are creating favorable environments for delivery robot deployment. Municipal pilots integrating robots into sidewalks, campuses, and mixed-use developments are reducing regulatory friction and enabling long-term fleet contracts. Vendors that align their solutions with urban mobility and sustainability goals stand to benefit significantly from public infrastructure investments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2200 Million |

| Market Size in 2026 | USD 2717 Million |

| Market Size in 2031 | USD 7805.93 Million |

| CAGR | 23.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Ground delivery robots continue to dominate the market, accounting for approximately 62% of global revenue in 2025. Their versatility in urban sidewalks, corporate campuses, and mixed-use developments makes them ideal for last-mile delivery operations. These robots are increasingly preferred due to their ability to navigate complex urban environments safely, carry moderate payloads efficiently, and integrate seamlessly with AI-powered fleet management systems. Aerial delivery robots, primarily drones, represent a smaller yet rapidly growing segment, catering to parcel delivery in remote, time-sensitive, or hard-to-reach areas. Their growth is propelled by technological advancements in autonomous flight, longer battery life, and integration with e-commerce platforms. Indoor delivery robots are gaining traction in controlled environments such as hospitals, hotels, and corporate offices. Here, their demand is driven by the need for sterile, predictable, and secure internal logistics, where human intervention is minimized, and efficiency is maximized.

Payload Capacity Insights

Delivery robots with payload capacities of 10–50 kg lead the market, holding nearly 48% share in 2025. This range provides an optimal balance between load capability, energy consumption, and operational flexibility, making these robots suitable for groceries, parcels, and medical supplies. Lightweight robots under 10 kg are predominantly used in food delivery, where speed, maneuverability, and frequent short-distance trips are prioritized. On the other hand, heavy-duty robots above 50 kg are emerging in industrial logistics, university campuses, and corporate settings, where bulk transportation of goods over medium distances enhances operational efficiency. The preference for mid-range payload robots is also supported by cost-effectiveness, reduced maintenance requirements, and compatibility with existing delivery infrastructure.

Application Insights

The food & beverage delivery segment remains the largest application globally, contributing around 40% of total market revenue in 2025. Its dominance is driven by rising consumer demand for on-demand delivery services, rapid growth of cloud kitchens, and increasing reliance on autonomous systems to overcome labor shortages. Parcel and e-commerce delivery is the fastest-growing application, fueled by the continuous expansion of online shopping platforms and increasing consumer expectations for same-day or ultra-fast delivery. Healthcare delivery and industrial campus logistics are emerging as high-growth, high-margin applications, benefiting from predictable usage patterns, compliance requirements, and automation initiatives that optimize internal transportation efficiency.

End-Use Insights

Restaurants, food delivery platforms, and e-commerce companies are the largest end users of delivery robots, primarily leveraging them to reduce operational costs and improve delivery speed. Healthcare institutions represent one of the fastest-growing end-use segments, deploying robots for intra-hospital logistics, medication distribution, and laboratory sample transport. Corporate campuses, educational institutions, and industrial facilities are increasingly integrating delivery robots to streamline internal supply chains, enhance operational efficiency, and reduce dependency on human labor for repetitive or high-volume tasks. These end-use trends reinforce the growth of mid-range payload and ground-based delivery robots across multiple sectors.

Explore more data points, trends and opportunities Download Free Sample Report

Delivery Robot Market Segmentations

By Product Type

- Ground Delivery Robots

- Aerial Delivery Robots (Drones)

- Indoor Delivery Robots

By Payload Capacity

- Less than 10 kg

- 10–50 kg

- Above 50 kg

By Application

- Food & Beverage Delivery

- Parcel & E-commerce Delivery

- Healthcare & Pharmaceutical Delivery

- Industrial & Campus Logistics

By End-Use Industry

- Restaurants & Food Delivery Platforms

- E-commerce Companies

- Healthcare Institutions

- Corporate & Industrial Campuses

- Educational Institutions

Regional Insights

North America

North America accounted for approximately 38% of the global delivery robot market in 2025, led by the United States. The region’s growth is driven by favorable regulations that facilitate sidewalk and campus robot deployments, strong venture capital funding, and an early-mover advantage in commercialization. Urban food delivery platforms, large university campuses, and corporate parks are key drivers, leveraging delivery robots to offset labor shortages and reduce operational costs. Additionally, advanced infrastructure, high technology adoption, and the presence of leading robotics manufacturers are supporting continued expansion across ground-based and fully autonomous delivery robot segments.

Asia-Pacific

Asia-Pacific held nearly 34% market share in 2025 and is the fastest-growing region, expanding at over 26% CAGR. Key contributors include China, Japan, and South Korea. Regional growth is fueled by dense urban populations, government-backed smart city initiatives, and domestic manufacturing capabilities that lower robot costs. E-commerce expansion and food delivery demand in mega-cities drive the adoption of ground delivery robots with mid-range payload capacities. Additionally, rising labor costs, technological readiness, and strong urban mobility planning are further accelerating the deployment of both indoor and outdoor autonomous delivery systems.

Europe

Europe represents around 20% of the market, with Germany, the UK, and Nordic countries driving growth. Adoption is supported by sustainability-focused urban mobility policies, increasing integration of AI and robotics in healthcare logistics, and growing demand for last-mile automation in dense city environments. Government incentives for smart mobility, regulatory frameworks supporting safe robot operation, and high consumer acceptance of autonomous solutions are key drivers for regional growth, particularly for ground delivery robots in food and parcel delivery applications.

Latin America

Latin America remains an emerging market, with Brazil and Mexico showing early adoption, contributing modestly to the global market. Growth is driven by expanding e-commerce penetration, urbanization trends, and pilot programs in smart city logistics. Food delivery platforms are leading the adoption due to labor challenges and rising consumer expectations for rapid deliveries. Infrastructure improvements in key cities, coupled with interest from private logistics providers, are expected to accelerate market penetration, particularly for lightweight and mid-range payload delivery robots.

Middle East & Africa

The Middle East, led by the UAE and Saudi Arabia, is witnessing growing deployment through smart city projects, government-backed innovation hubs, and rising interest in AI-powered logistics solutions. Ground and indoor delivery robots are being adopted in commercial districts, airports, and hospitals. Africa remains nascent but shows long-term potential, particularly in controlled-environment settings such as universities, corporate campuses, and healthcare facilities. Regional drivers include increasing urbanization, infrastructure development, and investments in autonomous technology pilots that demonstrate cost savings and operational efficiency.

Key Players in the Delivery Robot Market

- Starship Technologies

- Nuro

- JD Logistics

- Meituan Robotics

- Amazon Robotics

- Kiwibot

- Serve Robotics

- Pudu Robotics

- Segway-Ninebot

- Ottonomy.io

- Neolix

- Coco Robotics

- Boxbot

- TeleRetail

- Xiaomi Robotics