Clean Label Bakery Market Size

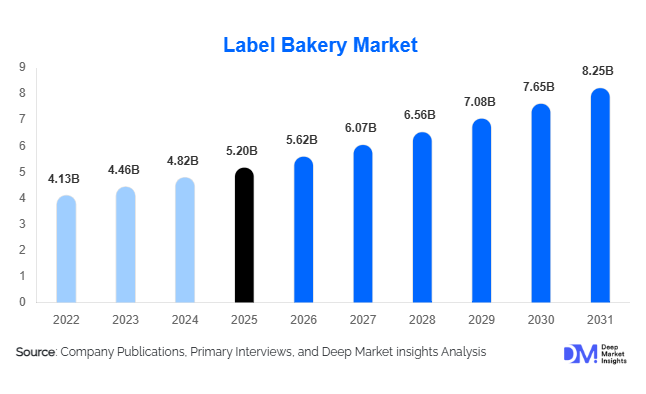

According to Deep Market Insights, the global clean-label bakery market was valued at USD 5.2 billion in 2025 and is projected to grow from USD 5.62 billion in 2026 to USD 8.25 billion by 2031, expanding at a CAGR of 8.0% during the forecast period (2026–2031). The clean label bakery market growth is primarily driven by rising consumer demand for transparency in food labeling, increasing preference for natural and minimally processed ingredients, and strong reformulation efforts by bakery manufacturers to eliminate artificial additives, preservatives, and synthetic processing aids.

Key Market Insights

- Clean-label bakery products are transitioning from niche to mainstream, with bread, rolls, and everyday baked goods increasingly reformulated using natural ingredients.

- Household consumption dominates global demand, driven by frequent purchase behavior and heightened health awareness among consumers.

- North America leads the global market, supported by strict labeling regulations, mature retail infrastructure, and high consumer awareness.

- Europe remains a strong and stable market, driven by clean ingredient regulations and a preference for artisanal bakery traditions.

- Asia-Pacific is the fastest-growing region, fueled by urbanization, rising disposable incomes, and growing adoption of Western bakery products.

- Technological innovation in natural preservatives and fermentation-based solutions is enabling longer shelf life without compromising clean label claims.

What are the latest trends in the clean-label bakery market?

Rapid Reformulation of Core Bakery Staples

One of the most prominent trends in the clean-label bakery market is the reformulation of high-volume, everyday products such as bread, rolls, and buns. Manufacturers are replacing artificial dough conditioners, emulsifiers, and preservatives with fermentation-derived enzymes, natural acids, and plant-based alternatives. Sourdough fermentation, extended proofing, and enzyme-based systems are increasingly used to achieve texture, volume, and shelf stability. This trend reflects a strategic shift, as clean label positioning is no longer limited to premium or specialty products but is becoming standard across mass-market bakery items.

Growth of Functional and Specialty Clean Label Bakery

Functional bakery products incorporating ancient grains, high fiber, high protein, and gluten-free formulations are gaining strong traction. Consumers associate clean label claims with overall health benefits, driving demand for products that combine nutritional enhancement with simple ingredient lists. Ancient grains such as spelt, millet, and quinoa are increasingly used to differentiate offerings, while reduced-sugar and allergen-friendly formulations are expanding the consumer base. This trend is particularly strong among younger and urban consumers seeking healthier daily staples.

What are the key drivers in the clean-label bakery market?

Rising Consumer Demand for Transparency and Natural Ingredients

Consumers are increasingly scrutinizing ingredient labels and actively avoiding products with artificial additives, preservatives, and complex chemical names. Clean-label bakery products align with this preference by offering short, recognizable ingredient lists that enhance trust and brand loyalty. This shift has compelled large bakery manufacturers to invest heavily in clean reformulation to maintain competitiveness and protect market share.

Retailer Support and Private Label Expansion

Major retailers are actively promoting clean-label bakery products through private-label offerings and dedicated shelf space. Supermarkets and hypermarkets are increasingly introducing clean-label bread and baked goods under store brands, offering competitive pricing while maintaining quality. This has significantly improved product accessibility and accelerated market penetration, particularly in North America and Europe.

What are the restraints for the global market?

Higher Production and Ingredient Costs

Clean-label bakery products typically involve higher production costs due to the use of organic flours, natural preservatives, and specialty ingredients. These costs often result in premium pricing, limiting adoption among highly price-sensitive consumers, particularly in emerging markets. Margin pressure remains a key challenge, especially for small and mid-sized bakeries.

Shelf-Life and Supply Chain Constraints

Maintaining shelf stability without synthetic preservatives remains a technical challenge. Clean label formulations are often more sensitive to temperature fluctuations and logistics inefficiencies. Inconsistent supply of certified clean-label ingredients further complicates production planning and cost management.

What are the key opportunities in the clean-label bakery industry?

Expansion of Functional and Lifestyle-Oriented Bakery Products

The convergence of clean label and functional food trends presents a significant growth opportunity. Products targeting gluten-free, high-protein, low-sugar, and plant-based diets allow manufacturers to command premium pricing while meeting evolving consumer needs. These segments are growing faster than conventional bakery categories and offer higher margins.

Digital and Direct-to-Consumer Distribution Models

E-commerce and direct-to-consumer channels are emerging as important growth avenues, particularly for specialty and artisanal clean-label bakery brands. Online platforms allow manufacturers to educate consumers, offer customization, and build brand loyalty without heavy dependence on traditional retail channels.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.2 Billion |

| Market Size in 2026 | USD 5.62 Billion |

| Market Size in 2031 | USD 8.25 Billion |

| CAGR | 8.0% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Bread and rolls dominate the clean-label bakery market, accounting for approximately 45% of total market value in 2025, making them the single largest product category globally. The high frequency of bread consumption primarily drives this dominance as a daily staple across households, combined with heightened consumer scrutiny of artificial preservatives, dough conditioners, and emulsifiers traditionally used in conventional bread formulations. Clean-label bread products, such as sourdough, wholegrain, multigrain, and organic variants, benefit from strong consumer trust, shorter ingredient lists, and perceived nutritional superiority. Additionally, retailers have aggressively expanded clean-label bread offerings under both branded and private-label portfolios, further strengthening volume sales.

Sweet baked goods, including cakes, muffins, and pastries, represent a significant portion of market demand, particularly in urban and premium retail settings. Growth in this segment is supported by indulgence-without-guilt positioning, where consumers seek familiar treats made with natural sweeteners, clean fats, and minimally processed ingredients. Meanwhile, specialty and functional bakery products, such as gluten-free, high-protein, low-sugar, and ancient grain-based baked goods, are the fastest-growing product category. Their growth is driven by rising health awareness, dietary preferences, and willingness among consumers to pay premium prices for clean-label products offering added functional benefits.

Ingredient Category Insights

Flours and grains constitute the largest ingredient category in the clean-label bakery market, accounting for nearly 30% of total market value. Demand is strongly driven by the shift toward organic, wholegrain, unbleached, and ancient grain flours, which align closely with clean label principles. Ingredients such as spelt, rye, millet, oats, and quinoa are increasingly incorporated to enhance nutritional profiles while maintaining ingredient transparency. The leading role of flours and grains is also attributed to their foundational presence across all bakery product types, making them the most critical input for clean-label reformulation.

Natural sweeteners, including honey, cane sugar, coconut sugar, and plant-derived alternatives, are gaining prominence as manufacturers reduce reliance on artificial sweeteners and high-fructose syrups. Similarly, natural preservatives and fermentation-based solutions are emerging as key growth drivers, as they enable shelf-life extension while preserving clean label integrity. Enzyme-based systems and plant extracts are increasingly replacing synthetic additives, allowing manufacturers to balance taste, texture, and product stability without compromising consumer trust.

Distribution Channel Insights

Retail channels, including supermarkets and hypermarkets, account for approximately 50% of global clean-label bakery sales, making them the dominant distribution channel. This leadership is driven by high consumer footfall, wide product assortment, and aggressive expansion of clean-label private-label bakery offerings by large retail chains. Supermarkets play a crucial role in normalizing clean-label products by positioning them alongside conventional bakery items, thereby accelerating mainstream adoption.

Specialty health and organic stores serve as an important channel for premium and niche clean-label bakery products, particularly organic, gluten-free, and functional offerings. These outlets support higher price points and cater to highly informed consumers seeking specialized products. E-commerce is the fastest-growing distribution channel, driven by convenience, broader product discovery, and increasing digital adoption. Direct-to-consumer bakery brands and online grocery platforms are leveraging digital marketing, subscription models, and personalized offerings to expand reach, especially among younger and urban consumers.

End-Use Insights

Household consumption represents approximately 60% of total clean-label bakery demand, underscoring the category’s role as a daily dietary staple rather than an occasional indulgence. Growth in this segment is fueled by rising health awareness, increased at-home consumption, and growing trust in clean-label products for family and long-term consumption. Consumers increasingly prefer clean-label bread and baked goods for regular meals due to perceived safety, simplicity, and nutritional benefits.

Commercial and institutional demand, including cafés, hotels, restaurants, and foodservice operators, is growing steadily. Clean label positioning is becoming a key differentiator in the HoReCa sector, as foodservice providers respond to consumer demand for transparency and healthier menu options. Premium cafés, quick-service restaurants, and hospitality chains are increasingly incorporating clean-label bakery items into menus to enhance brand credibility and customer loyalty.

Explore more data points, trends and opportunities Download Free Sample Report

Label Bakery Market Segmentations

By Product Type

- Bread & Rolls

- Sweet Baked Goods (Cakes, Muffins, Pastries)

- Savory Baked Goods (Crackers, Biscuits, Pretzels)

- Specialty & Functional Bakery (Gluten-Free, High-Protein, Organic)

- Bakery Mixes & Doughs

By Ingredient Category

- Flours & Grains (Organic, Wholegrain, Ancient Grains)

- Natural Sweeteners

- Natural Preservatives

- Natural Emulsifiers & Texturizers

- Natural Leavening Agents

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Health & Organic Stores

- E-commerce / Direct-to-Consumer

- Foodservice & HoReCa

By End-Use

- Household / At-Home Consumption

- Commercial & Institutional

- Retail & Bakery Chains

Regional Insights

North America

North America leads the global clean-label bakery market with an estimated 35% share in 2025. The United States is the largest contributor, driven by high consumer awareness of food ingredients, strong regulatory emphasis on labeling transparency, and widespread availability of clean label products across both branded and private label retail channels. Consumers in the U.S. actively avoid artificial preservatives and additives, accelerating reformulation across mass-market bread and bakery products.

Canada also demonstrates strong adoption, particularly in organic and specialty bakery categories, supported by health-conscious consumers and favorable regulatory standards. The region’s leadership is further reinforced by advanced retail infrastructure, strong private label penetration, and continuous innovation in clean ingredient technologies.

Europe

Europe accounts for approximately 28% of the global clean-label bakery market share, supported by major countries such as Germany, the U.K., and France. Growth in the region is driven by stringent food safety and labeling regulations, deep-rooted bakery consumption culture, and strong consumer preference for artisanal and traditionally produced baked goods. European consumers place high importance on ingredient origin, minimal processing, and authenticity, which aligns naturally with clean label propositions.

Additionally, widespread acceptance of organic certification and sustainability-focused food policies supports steady demand. Although Europe is a relatively mature market, innovation in functional bakery products and clean-label private labels continues to drive incremental growth.

Asia-Pacific

Asia-Pacific represents around 20% of the global market and is the fastest-growing region during the forecast period. Key markets include China, India, Japan, and Australia. Growth is driven by rapid urbanization, rising disposable incomes, expanding middle-class populations, and increasing adoption of Western-style bakery products. Consumers in metropolitan areas are becoming more health-conscious and are actively seeking premium, natural, and clean-label food options.

Japan and Australia exhibit strong demand for high-quality, premium clean-label bakery products, while China and India offer large-scale volume opportunities due to population size and growing modern retail penetration. Increased exposure to global food trends and digital retail platforms further accelerates market expansion in the region.

Latin America

Latin America holds close to 10% of the global clean-label bakery market, led by Brazil and Mexico. Market growth is supported by expanding urban populations, improving retail infrastructure, and rising awareness of health and nutrition. However, price sensitivity remains a limiting factor, restricting the rapid penetration of premium clean-label products. As incomes rise and local production of clean-label ingredients improves, adoption is expected to strengthen steadily.

Middle East & Africa

The Middle East & Africa region accounts for roughly 7% of global demand, with growth primarily concentrated in GCC countries such as the UAE and Saudi Arabia. Demand is driven by high per-capita income levels, strong reliance on imported premium food products, and increasing health awareness among urban consumers. Expansion of modern retail formats and premium bakery chains is supporting clean label adoption, while Africa represents a long-term growth opportunity as urbanization and packaged food consumption increase.

Key Players in the Clean Label Bakery Market

- Grupo Bimbo

- Flowers Foods

- Associated British Foods

- Aryzta AG

- Barilla Group

- General Mills Inc.

- Britannia Industries

- Warburtons

- Nature’s Path Foods

- Bob’s Red Mill Natural Foods