Car Jump Starter Market Size

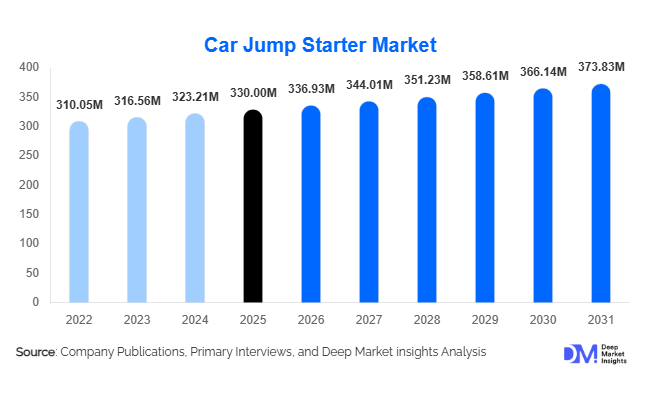

According to Deep Market Insights, the global car jump starter market size was valued at USD 330.00 million in 2025 and is projected to grow from USD 336.93 million in 2026 to reach USD 373.83 million by 2031, expanding at a CAGR of 2.1% during the forecast period (2026–2031). The market’s expansion is primarily driven by the rising adoption of lithium-ion portable jump starters, increasing demand from individual car owners and fleet operators, and continuous innovations in safety and multi-functionality.

Key Market Insights

- Lithium-ion jump starters dominate the market, accounting for nearly three-quarters of 2025 sales due to compact size, portability, and enhanced safety features.

- Portable and multi-function jump starters lead in product adoption, capturing about 45% of the market, driven by e-commerce penetration and consumer preference for convenience.

- Passenger car owners represent the largest end-use group, making up over 55% of demand in 2025, supported by growing consumer awareness of roadside safety.

- North America remains the largest regional market, with around 38% share in 2025, while Asia-Pacific is the fastest-growing region, driven by rising vehicle ownership in China and India.

- Online retail channels are expanding rapidly, enabling direct-to-consumer sales models, subscription-based roadside assistance packages, and stronger brand visibility.

- Technological integration, such as Bluetooth connectivity, app-based diagnostics, and EV auxiliary battery support, is reshaping competitive dynamics.

Car Jump Starter Market latest trends

Integration with Electric Vehicle (EV) Systems

As EV adoption accelerates, demand for auxiliary 12V battery jump starters tailored for hybrids and EVs is emerging. Manufacturers are developing low-current, high-safety solutions compatible with modern electrical architectures. This trend ensures product relevance in the evolving automotive landscape and offers a growth avenue for premium product lines.

Smart and Multi-Functional Devices

Consumers increasingly expect advanced safety features such as reverse polarity protection, short-circuit prevention, and temperature control. Beyond jump-starting, devices now double as portable power banks, emergency lights, and diagnostic tools. The convergence of multiple functions into compact units enhances consumer appeal and supports higher price points.

Car Jump Starter Market drivers

Rising Global Vehicle Population and Aging Fleets

The global increase in vehicle ownership, combined with aging fleets in mature markets, has amplified battery failure risks. Cold climates and longer vehicle idle periods post-pandemic have further driven demand for reliable jump-start solutions, particularly in the consumer segment.

Advancements in Lithium-Ion Technology

Lithium-ion battery improvements, including higher energy density, longer life cycles, and reduced weight, are reshaping the market. These devices are compact, portable, and more efficient than legacy lead-acid alternatives, accelerating adoption across both consumer and fleet applications.

Heightened Consumer Awareness of Roadside Safety

Growing awareness of road safety and preparedness, supported by insurance companies and roadside assistance programs, has boosted adoption. Marketing campaigns and influencer-driven reviews on e-commerce platforms further highlight the importance of owning personal jump starter devices.

Car Jump Starter Market restraints

High Costs of Advanced Models

Smart lithium-ion jump starters are significantly more expensive than basic lead-acid models. This cost barrier limits adoption in price-sensitive regions such as parts of Asia-Pacific, Africa, and Latin America, slowing overall market penetration.

Performance and Regulatory Challenges

Battery efficiency drops in extreme temperatures, affecting performance in very cold or hot regions. Moreover, lithium battery shipping and compliance with safety certifications (UN38.3, CE, UL) increase logistical complexity and cost, acting as hurdles for manufacturers.

Car Jump Starter Market opportunities

Growth in EV-Compatible Solutions

Manufacturers have an opportunity to develop jump starters designed for EV auxiliary systems. With EV penetration rising, this niche segment could evolve into a mainstream product line, helping sustain market growth beyond traditional internal combustion vehicle demand.

Expansion of E-Commerce and Direct-to-Consumer Channels

Online platforms are providing new avenues for brands to directly target consumers, offer bundled roadside subscriptions, and gather customer feedback. This shift reduces distribution costs and enables innovative pricing models while enhancing customer engagement.

Emerging Market Demand

Asia-Pacific, Latin America, and parts of Africa are witnessing rapid increases in vehicle ownership. Affordable, rugged, and feature-rich devices tailored for these markets represent a substantial opportunity for global and local players alike.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 330 Million |

| Market Size in 2026 | USD 336.93 Million |

| Market Size in 2031 | USD 373.83 Million |

| CAGR | 2.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Portable and multi-function jump starters dominate the product landscape, holding around 45% of the 2024 market share. Their popularity stems from compactness, convenience, and compatibility with passenger vehicles. Heavy-duty professional units, though smaller in share, maintain demand from workshops and fleet operators where higher amperage outputs are critical.

Application Insights

Passenger car owners account for nearly 58% of the market demand in 2024. Fleet operators and workshops represent growing segments, particularly in logistics-heavy economies where downtime costs are high. Recreational and off-road applications, such as for RVs and boats, are expanding as consumers seek rugged multi-use devices for adventure travel.

Distribution Channel Insights

E-commerce is the fastest-growing channel, driven by consumer reliance on online reviews, competitive pricing, and direct-to-consumer offerings. Traditional offline retail auto parts stores and specialty shops remain significant, particularly in Europe and North America, but online penetration is shifting revenue distribution globally.

Explore more data points, trends and opportunities Download Free Sample Report

Car Jump Starter Market Segmentations

Type

- Lithium-ion

- Lead-acid

- Hybrid/Other

Capacity/Power

- Under 10000mAh

- 10000–20000mAh

- Above 20000mAh

Distribution/Usage

- Consumer Retail

- Professional/Workshop

- Automotive OEM/Dealer

Regional Insights

North America

North America held about 38% of the market in 2024, with the U.S. leading demand. Harsh winters, high vehicle ownership, and a strong aftermarket culture support sustained demand for portable lithium-ion jump starters. Premium models with advanced safety features are particularly popular in this region.

Europe

Europe accounted for nearly 28% of the global market in 2024, led by Germany, the U.K., and France. Strict safety standards, cold weather conditions, and a robust automotive service industry drive adoption. Premiumization trends favor lithium-ion and smart models.

Asia-Pacific

Asia-Pacific is the fastest-growing region, currently holding about 22% of the market. China dominates both as a producer and consumer, while India and Southeast Asia are witnessing sharp growth in portable, affordable jump starter demand. Rising vehicle ownership and e-commerce adoption amplify this trend.

Latin America

Latin America represented around 7% of the 2024 market, with Brazil and Mexico leading. Cost sensitivity drives demand for affordable lead-acid and entry-level lithium-ion units, though rising middle-class incomes are creating opportunities for higher-end products.

Middle East & Africa

MEA accounted for just 5% of the 2024 market but shows steady growth. Harsh climates in Saudi Arabia, the UAE, and South Africa accelerate battery failures, creating a natural need for jump starters. Distribution and affordability remain challenges.

Key Players in the Car Jump Starter Market

- NOCO

- Clore Automotive

- Stanley Black & Decker

- Schumacher Electric Corporation

- GOOLOO

- Boltpower

- Antigravity Batteries

- TACKLIFE

- Audew

- DBPOWER

- CAT Professional Power Solutions

- HULKMAN

- Jump-N-Carry

- TOPVISION

- Beatit