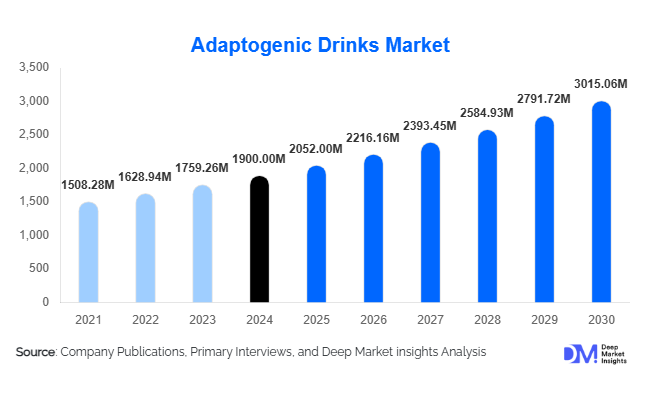

Global Adaptogenic Drinks Market Size

According to Deep Market Insights, the global adaptogenic drinks market size was valued at USD 2,980 million in 2025 and is projected to grow from USD 3,528.32 million in 2026 to reach USD 8,209.68 million by 2031, expanding at a CAGR of 18.4% during the forecast period (2026–2031). The market growth is primarily driven by rising consumer demand for stress-relief beverages, increasing adoption of functional and clean-label drinks, and the rapid expansion of wellness-oriented beverage consumption globally. Growing awareness of natural adaptogens such as ashwagandha, reishi mushroom, rhodiola, and ginseng is further accelerating product penetration across mainstream retail and e-commerce channels.

Key Market Insights

- Functional wellness beverages are replacing traditional sugary drinks as consumers prioritize stress relief, immunity, and cognitive health.

- Mushroom-based and herbal adaptogenic drinks are gaining rapid popularity, especially in North America and Europe.

- North America dominates the global market due to strong wellness culture and high disposable income.

- Asia-Pacific is the fastest-growing region, driven by Ayurveda-based consumption and rising middle-class health awareness.

- Clean-label, sugar-free, and organic formulations are becoming standard expectations across premium beverage categories.

- E-commerce and direct-to-consumer channels are reshaping distribution, enabling niche wellness brands to scale globally.

What are the latest trends in the adaptogenic drinks market?

Rise of Mushroom and Nootropic Beverages

Mushroom-based adaptogenic drinks, particularly those containing lion’s mane, reishi, and cordyceps, are becoming mainstream in functional beverage portfolios. These products are increasingly positioned as cognitive enhancers and stress-reduction solutions. Nootropic drinks targeting focus, productivity, and mental clarity are gaining traction among students, professionals, and gamers. Beverage brands are combining adaptogens with coffee alternatives, tea blends, and energy drinks to create hybrid functional products that deliver both taste and health benefits.

Clean-Label and Sugar-Free Transformation

The market is witnessing a strong shift toward clean-label formulations with minimal ingredients, natural sweeteners, and no artificial additives. Consumers are actively avoiding high-sugar energy drinks and artificial stimulants, pushing manufacturers to reformulate existing products. Organic certification and transparent sourcing are becoming critical purchasing factors. Brands are also investing in sustainable packaging solutions such as recyclable cans and biodegradable bottles to align with environmentally conscious consumer behavior.

What are the key drivers in the adaptogenic drinks market?

Rising Stress and Mental Wellness Awareness

Increasing levels of stress, anxiety, and burnout among urban populations are significantly driving demand for adaptogenic drinks. Consumers are shifting toward natural solutions that support emotional balance and mental resilience. Ingredients like ashwagandha and rhodiola are widely recognized for stress reduction benefits, making them key components in functional beverages. The growing focus on preventive healthcare is further strengthening long-term demand.

Expansion of Functional Beverage Industry

The rapid expansion of the functional beverage industry is a major growth driver. Consumers are moving away from carbonated soft drinks toward beverages that offer added health benefits such as immunity support, energy enhancement, and cognitive improvement. Adaptogenic drinks are benefiting from this shift, positioning themselves within premium wellness beverage categories alongside kombucha, probiotics, and plant-based drinks.

E-commerce and Direct-to-Consumer Growth

Digital retail platforms have enabled small and emerging wellness brands to scale globally without traditional retail barriers. Subscription-based beverage models, influencer marketing, and wellness communities are accelerating product discovery and repeat purchases. Online platforms also allow brands to educate consumers about adaptogenic ingredients, further improving adoption rates.

What are the restraints for the global market?

High Product Pricing and Limited Affordability

Adaptogenic drinks are positioned as premium wellness products due to costly raw materials, organic certifications, and advanced formulation processes. This results in higher retail prices compared to conventional beverages, limiting adoption in price-sensitive markets. While premium consumers continue to drive growth, mass-market penetration remains constrained.

Regulatory and Ingredient Compliance Challenges

Regulatory frameworks for functional claims and botanical ingredients vary significantly across regions. In several markets, manufacturers must provide clinical validation before making health-related claims. This increases R&D costs and delays product launches. Inconsistent global standards also create barriers for international expansion.

What are the key opportunities in the adaptogenic drinks industry?

Personalized Functional Nutrition

The emergence of personalized nutrition presents a major opportunity for adaptogenic drink manufacturers. AI-driven wellness platforms and consumer health tracking tools are enabling brands to develop customized beverage solutions targeting stress, sleep, focus, and immunity. This personalization trend is expected to drive premiumization and increase consumer loyalty.

Expansion in Emerging Economies

Asia-Pacific, Latin America, and parts of the Middle East offer significant untapped potential. Rising disposable income, urbanization, and growing awareness of herbal wellness are fueling demand. Countries like India and China, with strong cultural familiarity with adaptogens, are expected to become major growth engines for the global market.

Sports Nutrition Integration

Adaptogenic beverages are increasingly being adopted in sports nutrition for endurance, recovery, and performance enhancement. Ingredients such as cordyceps and maca are being integrated into energy and recovery drinks. Fitness clubs, gyms, and wellness centers are emerging as key distribution channels for performance-focused adaptogenic products.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2980.00 Million |

| Market Size in 2026 | USD 3528.32 Million |

| Market Size in 2031 | USD 8209.68 Million |

| CAGR | 18.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Adaptogenic functional beverages have emerged as one of the most dynamic categories within the global wellness industry, driven by a convergence of lifestyle changes, rising health consciousness, and increasing demand for convenient nutrition solutions. Among all product types, ready-to-drink (RTD) adaptogenic beverages represent the leading segment, largely due to their strong alignment with modern urban consumption habits. Consumers increasingly prefer beverages that require no preparation while still delivering targeted health benefits such as stress relief, improved focus, or enhanced immunity. This convenience-driven demand is further amplified by fast-paced lifestyles, longer working hours, and the growing popularity of on-the-go nutrition, particularly in metropolitan regions.Tea and coffee-based adaptogenic beverages also represent a rapidly expanding sub-segment, particularly mushroom coffee alternatives that replace or reduce conventional caffeine content. The demand for these products is primarily driven by rising concerns over caffeine sensitivity, anxiety, and sleep disruption. Consumers are actively seeking balanced energy solutions that enhance mental clarity without causing jitters or crashes. This shift is further reinforced by the growing biohacking culture and the influence of wellness communities promoting cognitive enhancement through natural adaptogens.Energy drinks infused with adaptogenic ingredients are also gaining significant traction as healthier substitutes for synthetic stimulant-based beverages. The key driver in this segment is the repositioning of energy drinks from purely performance-based products to holistic wellness enhancers. Younger consumers, in particular, are drawn to formulations that combine energy support with stress reduction and recovery benefits. Additionally, kombucha and fermented adaptogenic beverages are expanding steadily due to their dual functionality, offering both gut health and stress support benefits. The rising awareness of the gut-brain connection has further strengthened demand for probiotic-rich functional drinks, positioning fermented beverages as a core growth pillar in the market.

Application Insights

Stress management remains the most dominant application segment within the adaptogenic beverages market, primarily driven by the global rise in mental health challenges, workplace burnout, and lifestyle-induced stress. Increasing awareness of mental wellness has encouraged consumers to seek natural, non-pharmaceutical solutions, positioning adaptogenic beverages as an accessible daily support system. The normalization of stress-related discussions across workplaces and social platforms has further accelerated adoption.Immunity-boosting beverages have also gained significant momentum, particularly in the post-pandemic environment. Consumers have become more proactive about preventive health, leading to sustained demand for ingredients that support immune resilience. This shift is reinforced by seasonal health concerns, rising pollution levels, and increased exposure to urban lifestyle risks. Adaptogenic formulations combined with vitamins, antioxidants, and herbal extracts are increasingly positioned as daily immunity solutions.Sports recovery applications are expanding as athletes and fitness enthusiasts transition toward natural performance enhancement and recovery solutions. The key driver in this segment is the shift away from synthetic supplements toward plant-based alternatives that support endurance, reduce inflammation, and improve recovery times. Sleep-support and relaxation beverages represent an emerging high-growth niche, driven by increasing sleep disorders, screen exposure, and irregular work schedules. Ingredients such as ashwagandha, chamomile, and valerian root are widely incorporated to support relaxation and sleep quality, addressing a critical unmet need in modern lifestyles.

Distribution Channel Insights

Supermarkets and hypermarkets continue to dominate distribution channels for adaptogenic beverages due to their extensive product availability, strong consumer trust, and ability to offer a wide variety of brands under one roof. These channels benefit from high foot traffic and impulse purchasing behavior, particularly in urban retail environments. In-store promotions and product sampling also play a significant role in driving awareness for functional beverages.However, online retail and direct-to-consumer (DTC) platforms represent the fastest-growing distribution channels, fundamentally reshaping the way adaptogenic beverages reach consumers. The key driver of this shift is the digitalization of wellness consumption, where consumers increasingly rely on online reviews, influencer marketing, and social media education before making purchase decisions. Subscription-based models are particularly influential, enabling brands to build long-term customer relationships while offering personalized wellness solutions. E-commerce platforms also provide smaller brands with global visibility, accelerating market fragmentation and innovation.Specialty health stores and pharmacies maintain strong relevance, especially for premium and clinically positioned products. These channels benefit from credibility and perceived product authenticity, making them important for consumers seeking trusted wellness solutions. Cafés, gyms, and wellness centers are emerging as experiential retail environments where consumers can directly engage with functional beverages. These locations act as trial hubs, allowing consumers to experience benefits in real-time, thereby strengthening brand trust and repeat purchases. The overall distribution landscape is increasingly moving toward omnichannel integration, where physical and digital ecosystems work together to enhance accessibility and engagement.

Consumer Segment Insights

Millennials represent the largest consumer segment in the adaptogenic beverages market, primarily driven by strong health consciousness, high digital engagement, and willingness to experiment with functional wellness products. This demographic actively seeks products that support work-life balance, stress management, and long-term health optimization. Their purchasing behavior is strongly influenced by sustainability, ingredient transparency, and brand authenticity.Generation Z is emerging as a highly influential consumer group, driving rapid adoption through social media platforms, wellness trends, and peer-driven recommendations. The key driver for this segment is experimentation and lifestyle expression, where functional beverages are seen not only as health products but also as part of identity and self-care culture. Influencer marketing and short-form video content significantly shape purchasing decisions in this cohort.Working professionals form another critical consumer base, with demand primarily driven by workplace stress, cognitive overload, and productivity requirements. Adaptogenic beverages are increasingly integrated into daily routines as alternatives to traditional caffeine-heavy drinks. Older consumers are also steadily adopting these beverages, primarily for immunity support, sleep improvement, and general wellness maintenance. The aging global population, combined with increased focus on preventive healthcare, continues to support long-term demand stability across this segment.

Explore more data points, trends and opportunities Download Free Sample Report

Adaptogenic Drinks Market Segmentations

By Product Type

- Adaptogenic Functional Beverages

- Adaptogenic Tea & Coffee Beverages

- Adaptogenic Energy Drinks

- Adaptogenic Dairy & Plant-Based Drinks

- Adaptogenic Kombucha & Fermented Drinks

- Adaptogenic Sports & Recovery Drinks

- Adaptogenic Sleep & Relaxation Drinks

By Ingredient Type

- Ashwagandha-Based Drinks

- Ginseng-Based Drinks

- Reishi & Lion’s Mane Mushroom Drinks

- Cordyceps-Based Drinks

- Rhodiola Rosea-Based Drinks

- Tulsi (Holy Basil)-Based Drinks

- Multi-Adaptogen Blends

By Functionality

- Stress Management & Relaxation

- Cognitive Enhancement & Focus

- Energy & Endurance Support

- Immunity Boosting Drinks

- Gut Health & Digestive Support

- Sleep Improvement & Recovery

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Health Stores

- Pharmacies & Drug Stores

- Online Retail & E-commerce Platforms

- Cafés & Foodservice Channels

- Fitness Centers & Wellness Stores

By Consumer Group

- Millennials

- Generation Z

- Working Professionals

- Athletes & Fitness Enthusiasts

- Aging Population

- Health-Conscious Urban Consumers

Regional Insights

North America

North America remains the most mature and leading market for adaptogenic beverages, driven by a deeply established wellness culture, high disposable income levels, and rapid product innovation. The United States dominates regional demand, supported by strong consumer awareness of functional ingredients and a well-developed health beverage ecosystem. Key growth drivers include the popularity of biohacking trends, increasing adoption of nootropic beverages, and strong penetration of mushroom-based coffee alternatives and wellness shots. Canada also demonstrates strong growth momentum, particularly in organic, clean-label, and sustainably sourced beverage categories. Regulatory openness to functional ingredients and strong retail infrastructure further enhance market expansion in the region.

Europe

Europe exhibits strong demand for natural, organic, and sustainably produced adaptogenic beverages. The region’s growth is primarily driven by environmental consciousness, strict regulatory standards for food and beverage quality, and deep-rooted herbal consumption traditions. Countries such as Germany, the United Kingdom, and France are key contributors, with consumers showing a strong preference for eco-certified and clean-label products. The increasing popularity of herbal teas, botanical infusions, and functional mushroom drinks reflects a broader shift toward preventive healthcare and natural wellness. Sustainability concerns and carbon-neutral production practices also play a significant role in shaping consumer preferences across Europe.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, fueled by rapid urbanization, rising disposable incomes, and strong cultural affinity for herbal and traditional medicine systems. Countries such as China, India, Japan, and South Korea are driving demand through a combination of ancient wellness practices and modern functional beverage innovation. India’s Ayurvedic heritage and China’s traditional herbal medicine systems provide a strong foundation for adaptogenic product acceptance. The expansion of e-commerce platforms, coupled with increasing health awareness among younger populations, is accelerating product penetration across both premium and mass-market segments. Additionally, urban stress levels and fast-paced lifestyles are significantly contributing to demand for stress-relief and cognitive-enhancing beverages.

Latin America

Latin America is an emerging market with strong growth potential, led by Brazil and Mexico. The region’s expansion is driven by increasing urbanization, rising health awareness, and growing interest in fitness and wellness lifestyles. Consumers are gradually shifting toward functional beverages as part of broader preventive health trends. The presence of international brands, combined with localized product adaptations, is enhancing accessibility and market penetration. Digital retail channels and social media influence are also playing a critical role in shaping consumer awareness and driving trial adoption in the region.

Middle East & Africa

The Middle East and Africa region is witnessing steady growth, supported by rising health consciousness, increasing disposable incomes in urban centers, and a strong preference for premium wellness products. Countries such as the United Arab Emirates and Saudi Arabia are leading demand, driven by luxury wellness trends and high consumption of imported functional beverages. The hot climate also contributes to sustained demand for hydrating and refreshing functional drinks. Africa plays a dual role as both a growing consumer base and a key source of herbal and botanical ingredients, supporting regional supply chain development and export-oriented production. Overall, the region is gradually evolving into an important emerging market for adaptogenic beverages, with strong long-term potential.

Key Players in the Global Adaptogenic Drinks Market

- PepsiCo Inc.

- The Coca-Cola Company

- Rebbl Inc.

- Four Sigmatic Foods Inc.

- Laird Superfood Inc.

- GT’s Living Foods

- Health-Ade LLC

- Sunwink Inc.

- Kin Euphorics

- Rasa Inc.

- Odyssey Wellness LLC

- Remedy Drinks

- Humm Kombucha LLC

- Mud/Wtr Inc.

- Buddha Brands Company Inc.