Wi-Fi Module Market Size

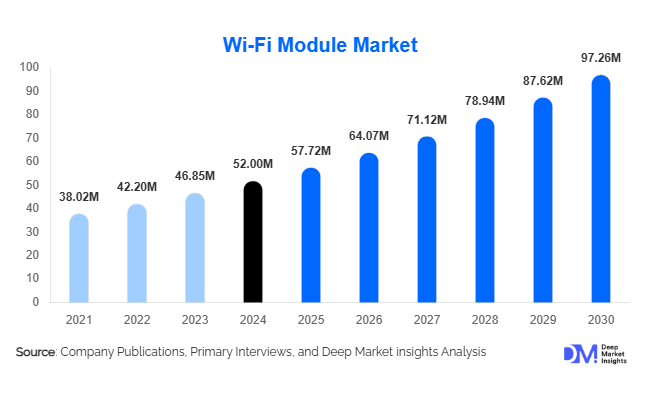

According to Deep Market Insights, the global WiFi module market size was valued at USD 52 million in 2025 and is projected to grow from USD 57.72 million in 2026 to reach USD 97.26 million by 2031, expanding at a CAGR of 11% during the forecast period (2026–2031). The Wi-Fi module market growth is primarily driven by the rapid adoption of IoT devices, rising demand for smart homes and industrial automation, and increasing integration of wireless connectivity across consumer electronics and automotive applications.

Key Market Insights

- IoT proliferation is the strongest growth driver, with Wi-Fi modules serving as the backbone of connected ecosystems across consumer, industrial, and healthcare applications.

- Smart home penetration is accelerating, fueled by demand for smart speakers, connected appliances, and home security systems integrated with Wi-Fi modules.

- Automotive adoption of Wi-Fi modules is surging, enabling in-car connectivity, infotainment systems, and vehicle-to-everything (V2X) communication.

- Asia-Pacific dominates the market, led by China’s large-scale electronics manufacturing and rapid smart device adoption.

- North America remains a major hub for innovation in Wi-Fi technologies, driven by strong IoT penetration and advanced network infrastructure.

- Advancements in Wi-Fi 6 and Wi-Fi 7 technologies are reshaping module design, enabling higher speeds, lower latency, and improved energy efficiency.

Wi-Fi Module Market Trends

Shift Toward Wi-Fi 6 and Wi-Fi 7 Modules

Manufacturers are increasingly developing modules compatible with Wi-Fi 6 and emerging Wi-Fi 7 standards. These next-gen technologies offer improved data throughput, enhanced coverage, and reduced power consumption, making them ideal for high-density IoT environments, smart factories, and AR/VR applications. This trend is expected to accelerate adoption in both consumer and industrial segments, with Wi-Fi 7 positioning as a critical enabler for ultra-low latency use cases.

Integration with AI and Edge Computing

Wi-Fi modules are being integrated with AI-enabled edge devices, enabling real-time data processing and reduced dependence on cloud connectivity. This trend supports applications such as predictive maintenance in manufacturing, intelligent healthcare monitoring, and smart retail analytics. AI-powered Wi-Fi modules also enhance network efficiency by optimizing bandwidth allocation and reducing interference in multi-device environments.

Wi-Fi Module Market Drivers

IoT Expansion Across Industries

The exponential growth of IoT devices, from smart appliances and wearables to industrial sensors, is fueling demand for Wi-Fi modules. Their ability to provide reliable, high-speed connectivity makes them integral to applications such as remote monitoring, connected healthcare, and energy management. The growing adoption of smart city initiatives further supports this expansion.

Rising Consumer Electronics Demand

Consumer electronics, including smartphones, laptops, gaming consoles, and smart TVs, account for a significant share of Wi-Fi module demand. As consumer preferences shift toward wireless and always-connected devices, manufacturers are embedding advanced Wi-Fi modules to enhance user experience and enable seamless multi-device integration.

Wi-Fi Module Market Restraints

High Power Consumption Concerns

Traditional Wi-Fi modules consume more power compared to alternatives such as Bluetooth Low Energy (BLE) and Zigbee. This limits their adoption in battery-powered IoT devices where energy efficiency is critical, posing a challenge for broader integration in portable applications.

Security and Privacy Challenges

Wi-Fi modules are vulnerable to cyberattacks such as unauthorized access, malware, and data breaches. As IoT ecosystems expand, ensuring robust encryption and security protocols becomes increasingly complex. These vulnerabilities may slow adoption in sensitive applications such as healthcare and financial services.

Wi-Fi Module Market Opportunities

Smart Home and Building Automation

Rising global investment in smart homes and intelligent building systems presents significant opportunities for Wi-Fi module providers. Integration into smart lighting, HVAC systems, and security solutions is expanding the consumer base and driving long-term demand for high-performance modules.

Automotive and Industrial IoT Expansion

The automotive industry is increasingly adopting Wi-Fi modules for in-vehicle entertainment, telematics, and V2X communication. Meanwhile, industrial IoT applications, such as predictive maintenance, robotics, and remote asset monitoring, are expected to generate substantial demand for rugged, low-latency Wi-Fi modules.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 52 Million |

| Market Size in 2026 | USD 57.72 Million |

| Market Size in 2031 | USD 97.26 Million |

| CAGR | 11% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Embedded Wi-Fi modules dominate the market, offering plug-and-play connectivity for a wide range of IoT and consumer devices. Standalone modules are gaining traction in applications requiring flexibility and scalability, particularly in industrial IoT and automotive sectors. Surface-mount modules are also seeing growth due to compact design requirements in wearables and portable electronics.

Application Insights

Consumer electronics remain the largest application segment, followed by smart homes and industrial automation. Healthcare applications, such as connected medical devices and patient monitoring systems, are expanding rapidly. The automotive sector is expected to witness the fastest CAGR, driven by rising demand for connected and autonomous vehicles.

Explore more data points, trends and opportunities Download Free Sample Report

Wi-Fi Module Market Segmentations

By Module Type

- Chipset

- SiP

- SiM

By Standard

- Wi-Fi 4

- Wi-Fi 5

- Wi-Fi 6

- Wi-Fi 6E

- Wi-Fi 7

By Application

- IoT

- Consumer

- Automotive

- Industrial

By Channel

- OEM

- Distribution

Regional Insights

Asia-Pacific

Asia-Pacific leads the global market, supported by China’s massive electronics ecosystem, India’s smart city initiatives, and Japan’s advancements in consumer electronics. Strong manufacturing capabilities and cost advantages position the region as the hub for global Wi-Fi module production.

North America

North America maintains a strong demand, led by widespread IoT adoption, advanced network infrastructure, and heavy investment in smart home technologies. The U.S. remains a key innovator in Wi-Fi 6/7 module development.

Europe

Europe is witnessing steady growth, driven by regulatory support for energy-efficient buildings and rising adoption of industrial IoT solutions. Germany, the U.K., and France are leading adopters of advanced Wi-Fi-enabled applications in both consumer and industrial domains.

Latin America

Latin America is an emerging market, with demand concentrated in Brazil and Mexico. Growing internet penetration and increasing affordability of connected devices are driving regional adoption of Wi-Fi modules.

Middle East & Africa

MEA is gradually expanding its presence in the global Wi-Fi module market, supported by smart city projects in the UAE and Saudi Arabia. Africa is showing early-stage adoption, with demand primarily in consumer electronics and telecom infrastructure.

Key Players in the Wi-Fi Module Market

- Murata Manufacturing

- Qualcomm Technologies

- Broadcom Inc.

- Intel Corporation

- Texas Instruments

- Espressif Systems

- Cypress Semiconductor (Infineon Technologies)