Wedding Ring Market Size

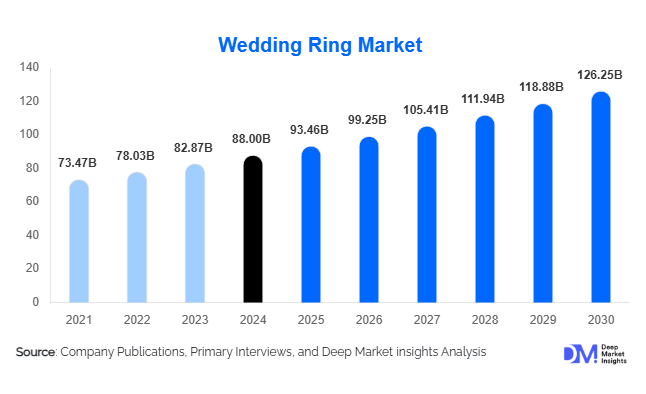

According to Deep Market Insights, the global wedding ring market size was valued at USD 88.00 billion in 2025 and is projected to grow from USD 93.46 billion in 2026 to reach USD 126.25 billion by 2031, expanding at a CAGR of 6.2% during the forecast period (2026–2031). Market growth is primarily driven by rising wedding expenditures worldwide, increasing demand for customised and sustainable jewellery, and the rapid expansion of online jewellery retail channels that enhance accessibility and personalisation.

Key Market Insights

- Gold wedding rings dominate global demand, accounting for over 50% of total sales due to cultural significance, design flexibility, and enduring consumer trust.

- Asia-Pacific is the fastest-growing region, driven by rising disposable incomes in India and China, cultural emphasis on gold jewellery, and the growing influence of digital retail platforms.

- Mid-range rings lead by value share, as couples seek premium quality and craftsmanship at affordable prices.

- Offline retail remains dominant, but online sales are growing rapidly through augmented-reality try-ons, digital customisation, and direct-to-consumer models.

- Sustainability and ethical sourcing are becoming decisive purchasing factors, with growing adoption of recycled gold, lab-grown diamonds, and transparent supply chains.

- Women’s rings represent the largest consumer segment, contributing around two-thirds of total market revenue in 2025.

Wedding Ring Market Trends

Customisation and Digital Design Experiences

Personalised and bespoke wedding rings are becoming mainstream, with consumers favouring unique designs that reflect individuality and emotional connection. Jewellery brands are integrating 3D design software, AR-based try-on tools, and online configurators that allow buyers to preview metal types, gemstone settings, and engravings before purchase. This digital transformation enhances customer engagement and enables brands to capture higher margins by offering on-demand customisation, merging tradition with technology.

Ethical and Sustainable Jewellery Demand

Consumers are increasingly prioritising sustainability in wedding jewellery purchases. The adoption of lab-grown diamonds, recycled metals, and conflict-free gemstones is accelerating across global markets. Leading brands are highlighting traceability and environmental stewardship in their marketing strategies. Ethical sourcing certifications, carbon-neutral manufacturing, and eco-friendly packaging are now key differentiators influencing millennial and Gen Z buyers who prefer conscious luxury over conspicuous consumption.

Wedding Ring Market Drivers

Rising Global Wedding Expenditure

The resurgence of large-scale weddings post-pandemic, coupled with higher disposable incomes, is fueling growth in the wedding ring market. Couples increasingly allocate greater portions of their wedding budgets to high-quality or branded jewellery. In emerging economies, cultural traditions emphasising gold and diamond jewellery as investments further strengthen long-term demand for wedding rings.

Expansion of Online and Omni-Channel Retail

The jewellery industry’s digital shift is a major growth catalyst. E-commerce and hybrid retail models allow consumers to compare designs, access competitive pricing, and enjoy doorstep delivery with authenticity guarantees. Platforms featuring virtual consultations and AR previews enhance consumer confidence in high-value online purchases. As a result, digital channels are expected to register double-digit growth through 2031, particularly among younger demographics.

Wedding Ring Market Restraints

Volatility in Precious Metal and Gemstone Prices

Fluctuating prices of gold, platinum, and diamonds directly affect production costs and retail pricing, constraining affordability for middle-income consumers. Rapid price increases may deter purchases or push buyers toward alternative materials, impacting profit margins, especially for small and mid-sized jewellers operating on thin spreads.

Intense Competition and Market Fragmentation

The global wedding ring industry is highly fragmented, with thousands of regional and independent jewellers competing alongside global luxury houses. Intense price competition in the mid-range and economy segments, coupled with limited product differentiation, exerts pressure on margins. Brand loyalty is increasingly influenced by design innovation and digital engagement rather than legacy reputation alone.

Wedding Ring Market Opportunities

Emerging Markets and Regional Expansion

Rapid urbanisation, rising incomes, and strong cultural emphasis on marriage are creating lucrative opportunities across Asia-Pacific, the Middle East, and Latin America. Localised designs, regional gemstone preferences, and hybrid offline–online retail strategies can help brands capture untapped demand. Markets such as India and China are poised to contribute a majority of global volume growth through 2031.

Alternative Materials and Innovative Design

Growing acceptance of alternative materials such as titanium, tungsten, palladium, and carbon fibre presents new avenues for cost-effective innovation. These materials appeal to modern consumers seeking durability, unique aesthetics, and affordability. The increasing popularity of mixed-metal and unisex designs further expands the addressable market beyond traditional wedding jewellery.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 88 Billion |

| Market Size in 2026 | USD 93.46 Billion |

| Market Size in 2031 | USD 126.25 Billion |

| CAGR | 6.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Gold wedding rings dominate with over 50% market share due to cultural legacy and versatility. Platinum rings hold a strong position in premium markets, valued for purity and durability. Diamond and gemstone-set rings command the highest average selling price, driving revenue in luxury tiers. Alternative-material rings, such as titanium and tungsten, are emerging as fast-growing sub-categories among male and minimalist consumers, reflecting the shift toward modern, sustainable fashion choices.

Application Insights

Bridal jewellery remains the core application, accounting for the majority of market demand. Custom-designed and matching couple rings are increasingly popular among millennials and Gen Z couples seeking personalisation. Anniversary and vow-renewal rings represent a growing secondary segment, supported by marketing that emphasises lifelong symbolism and emotional storytelling. The rise of gender-neutral and same-sex wedding rings further diversifies the application landscape, promoting inclusivity and expanding the consumer base.

Distribution Channel Insights

Offline retail stores, including independent jewellers, boutique stores, and luxury chains, retain dominance due to consumer trust and in-person consultation. However, online and direct-to-consumer (D2C) channels are expanding fastest, fueled by digital marketing, AR-based try-ons, and influencer-driven campaigns. Hybrid omni-channel models combining online browsing with in-store pickup or customisation services are becoming standard among leading brands, bridging convenience with credibility.

Consumer Segment Insights

Women’s rings accounted for roughly 65% of global revenue in 2025, driven by higher unit prices and design complexity. Men’s wedding rings are gaining momentum, particularly in titanium, tungsten, and minimalist styles. The mid-range price segment leads globally with around 40% share, as it balances quality with affordability, while luxury rings continue to grow among affluent consumers seeking exclusivity and brand prestige.

Explore more data points, trends and opportunities Download Free Sample Report

Wedding Ring Market Segmentations

By Product Type

- Gold Wedding Rings

- Platinum Wedding Rings

- Diamond & Gemstone Wedding Rings

- Alternative Material Rings (Titanium, Tungsten, Carbon Fiber, Palladium)

- Lab-Grown Diamond Rings

By Design Type

- Classic Bands

- Solitaire Rings

- Halo Rings

- Vintage & Antique-Style Rings

- Customized & Personalized Rings

By Price Range

- Economy Rings (Below USD 500)

- Mid-Range Rings (USD 500 – USD 2,000)

- Premium Rings (USD 2,000 – USD 5,000)

- Luxury Rings (Above USD 5,000)

By Distribution Channel

- Offline Retail (Jewellery Boutiques, Franchise Stores, Department Stores)

- Online Retail (Brand Websites, E-Commerce Platforms, D2C Stores)

- Hybrid/Omni-Channel Distribution

By End User

- Women

- Men

- Unisex/Non-Binary Couples

Regional Insights

North America

North America holds a significant market share (35% in 2025), led by the U.S. The region’s consumers favour branded and premium rings, often featuring platinum or diamonds. Online jewellery sales have surged, supported by trusted e-commerce platforms and advanced customisation tools. The market is mature but remains strong in high-value purchases and brand loyalty.

Europe

Europe represents approximately 28% of the global market, with leading demand from the U.K., Germany, France and Italy. The region’s consumers prefer design-driven, sustainable rings featuring ethically sourced materials. Luxury brands such as Cartier and Bvlgari maintain strong footholds, while digital-first jewellers gain traction among younger consumers seeking transparency and convenience.

Asia-Pacific

Asia-Pacific is the fastest-growing region, projected to expand at 8–9% CAGR through 2031. Rising middle-class wealth, gold’s cultural significance, and an increasing number of weddings in India and China are key drivers. The proliferation of e-commerce platforms and government support for hallmarking and domestic jewellery production further fuel regional growth.

Latin America

Latin America accounts for around 6% of global revenue, led by Brazil and Mexico. The region’s market is characterised by growing middle-class spending and rising affinity for Western-style diamond engagement and wedding rings. Local jewellers are increasingly integrating online channels to reach younger consumers.

Middle East & Africa

This region, contributing about 4% of market share, exhibits strong demand for high-purity gold and elaborate designs. Gulf countries such as the UAE and Saudi Arabia remain key hubs for luxury jewellery consumption. Africa’s growing urban population and gold production base support long-term growth potential for both domestic sales and exports.

Key Players in the Wedding Ring Market

- Cartier International SNC

- Tiffany & Co.

- Pandora A/S

- Harry Winston Inc.

- Bvlgari S.p.A.

- Chopard & Cie SA

- De Beers Group

- James Allen Inc.

- Blue Nile Inc.

- Tacori Inc.

Recent Developments

- In June 2025, Tiffany & Co. announced a new sustainability initiative featuring 100% recycled gold bands and blockchain-based diamond traceability to enhance transparency.

- In April 2025, Pandora launched its “Brilliance Wedding” collection using exclusively lab-grown diamonds, expanding its ethical jewellery portfolio globally.

- In February 2025, Blue Nile introduced an augmented-reality try-on platform for online ring customization, aiming to boost digital engagement and conversion rates.