Vegan Collagen Market Size

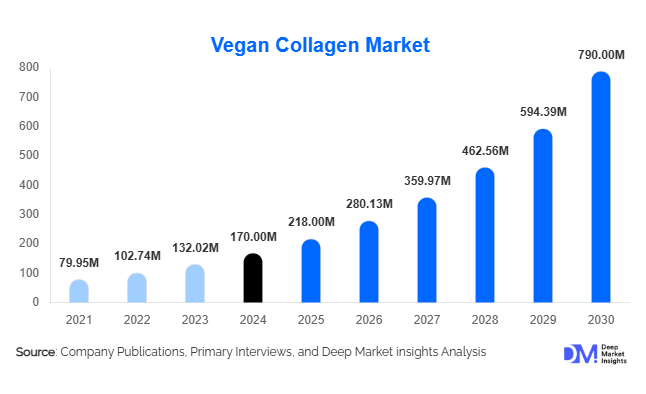

According to Deep Market Insights, the global vegan collagen market size was valued at USD 170 million in 2025 and is projected to grow from USD 218 million in 2026 to reach USD 790 million by 2031, expanding at a CAGR of 28.5% during the forecast period (2026–2031). The vegan collagen market growth is primarily driven by increasing demand for cruelty-free alternatives to animal-derived collagen, the rapid adoption of synthetic biology and fermentation technologies, and expanding applications across nutraceuticals, beauty, food & beverages, and pharmaceuticals.

Key Market Insights

- Rising demand for plant-based and cruelty-free products is reshaping the collagen market, driving preference for sustainable vegan collagen solutions.

- North America dominates the global market in 2025, accounting for more than 35% of demand, led by strong nutraceutical and beauty industries.

- The Asia-Pacific region is the fastest-growing, supported by booming personal care industries in China, Japan, and South Korea, as well as the expanding vegan population in India and Australia.

- Technological innovations in fermentation, CRISPR-based bioengineering, and recombinant DNA synthesis are making large-scale vegan collagen production commercially viable.

- Cosmetics and personal care remain the leading application, accounting for nearly 42% of the total global revenue in 2025.

- Online retail platforms are emerging as a primary sales channel, driven by direct-to-consumer strategies and the rapid expansion of e-commerce.

Latest Market Trends

Biotechnology-Powered Collagen Production

One of the most prominent trends in the vegan collagen market is the use of advanced biotechnology, including precision fermentation and recombinant DNA technology, to replicate human collagen proteins without animal inputs. Startups and biotech firms are partnering with established nutraceutical and skincare companies to scale production. This enables the development of “bio-identical” collagen with enhanced purity, stability, and safety compared to animal-sourced collagen, meeting demand from premium healthcare and beauty industries.

Expansion into Functional Foods and Beverages

Vegan collagen is increasingly being incorporated into functional foods and beverages, such as protein bars, gummies, fortified waters, and plant-based smoothies. Consumers are looking for holistic wellness products that combine beauty, nutrition, and convenience. Food manufacturers are leveraging vegan collagen as a differentiator, marketing it as a sustainable and ethical ingredient to appeal to younger demographics and eco-conscious buyers.

Vegan Collagen Market Drivers

Growing Consumer Shift Toward Plant-Based Products

Rising global veganism and flexitarian diets are accelerating demand for sustainable collagen alternatives. Consumers are increasingly conscious of the environmental impact of livestock farming and animal welfare concerns, driving the adoption of vegan collagen. The plant-based trend has moved beyond food into supplements, personal care, and healthcare, aligning perfectly with vegan collagen’s positioning.

Expanding Application in Beauty & Personal Care

Cosmetics and personal care companies are increasingly integrating vegan collagen into serums, creams, and hair care formulations. Anti-aging and skin-repair properties are fueling demand, particularly in regions with mature beauty markets such as North America, Europe, and East Asia. Vegan collagen appeals strongly to Millennials and Gen Z consumers, who favor ethical and eco-friendly beauty solutions.

Advancements in Biotechnology

The use of genetically engineered yeast, bacteria, and algae for collagen synthesis is dramatically improving scalability and reducing costs. These innovations ensure vegan collagen can be manufactured at industrial levels with consistent quality, positioning it as a viable alternative to traditional collagen. Biotech collaborations and R&D investments are accelerating product commercialization globally.

Market Restraints

High Production Costs

Despite advancements, the production of vegan collagen remains more expensive than animal-derived collagen. High R&D costs, expensive fermentation setups, and limited large-scale capacity hinder wider adoption, especially in price-sensitive developing markets.

Regulatory Uncertainty

The regulatory framework for bioengineered vegan collagen is still evolving across regions. Differing standards for labeling, safety approvals, and marketing claims create challenges for companies entering multiple markets. This could slow global commercialization efforts.

Vegan Collagen Market Opportunities

Expansion into Pharmaceuticals & Biomedical Applications

Vegan collagen holds significant potential in pharmaceuticals and biomedicine, especially in tissue engineering, wound healing, and drug delivery systems. Its biocompatibility and ethical production process make it highly attractive for medical use. With increasing clinical studies validating its efficacy, this segment is expected to be one of the most lucrative growth avenues over the next decade.

Export-Led Growth from Asia-Pacific

Asia-Pacific, particularly China, India, and South Korea, is emerging as a key production hub for vegan collagen. Governments in these regions are investing heavily in biotechnology infrastructure, and local manufacturers are scaling capacity for global exports. Rising demand from North America and Europe presents strong export-driven opportunities for APAC-based suppliers.

Integration with Wellness and Fitness Nutrition

The fitness industry is embracing vegan collagen supplements as alternatives to whey protein and animal-derived collagen powders. Plant-based athletes and health-conscious consumers are driving adoption, particularly in North America and Europe. This segment represents a high-potential growth area as sports nutrition evolves toward plant-based formulations.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 170 Million |

| Market Size in 2026 | USD 218 Million |

| Market Size in 2031 | USD 790 Million |

| CAGR | 28.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Powders and capsules dominate the vegan collagen market in 2025, accounting for 48% of global revenue. These formats are preferred due to their convenience, ease of integration into daily routines, and versatility across dietary and functional applications. Powders are highly favored as they can be easily mixed into drinks, smoothies, and functional foods, making them ideal for health-conscious consumers seeking flexible supplementation. Capsules and tablets appeal to consumers who prioritize convenience and dosage precision for daily supplementation. Topical and skincare formulations, such as creams and serums, are experiencing strong growth due to rising consumer focus on cruelty-free and vegan cosmetics, particularly in Europe and North America. Vegan collagen drinks and functional foods are projected to grow at the fastest rate, with a CAGR of over 32%, as consumers increasingly prefer convenient, ready-to-consume products that combine nutrition and beauty benefits.

Application Insights

Cosmetics & personal care remain the leading application, representing 42% of the global market share in 2025. This is driven by the growing demand for anti-aging, skin rejuvenation, and hair care products, especially among younger and middle-aged demographics in developed markets. Nutraceuticals and dietary supplements follow closely with a 34% share, supported by an expanding health-conscious population and increased awareness of joint, bone, and skin health benefits. Functional beverages are rapidly emerging as a key growth segment, fueled by the trend of protein-enriched, plant-based, and fortified drinks. Pharmaceuticals and biomedical applications, although smaller currently, are expected to grow rapidly post-2026, driven by regulatory approvals and increasing clinical adoption of vegan collagen in tissue engineering, wound healing, and regenerative medicine.

Distribution Channel Insights

Online retail is the dominant distribution channel, accounting for nearly 55% of total revenue in 2025. The surge in e-commerce and direct-to-consumer platforms enables brands to reach health-conscious, vegan, and millennial consumers globally. These channels allow for better transparency, education about product benefits, and influencer-driven marketing campaigns. Offline channels such as specialty health stores, pharmacies, and supermarkets/hypermarkets remain important for premium buyers and older demographics who prefer physical product evaluation. Supermarkets and hypermarkets are also increasing shelf space for vegan and plant-based products, enhancing visibility and accessibility.

End-Use Insights

Healthcare and medical applications are projected to grow the fastest, with a CAGR of over 30% during 2026–2031, propelled by biomedical research and the adoption of vegan collagen in tissue engineering and wound healing. Beauty and personal care remain the largest end-use segment, driven by anti-aging skincare, hair, and dermatology-focused applications. Fitness and sports nutrition are emerging as high-growth areas, particularly in North America and Asia-Pacific, where younger consumers and plant-based athletes are driving demand for collagen-enriched protein powders and functional beverages. Food and nutrition applications, such as collagen-fortified snacks and beverages, are expanding rapidly due to rising consumer preference for holistic wellness solutions.

Explore more data points, trends and opportunities Download Free Sample Report

Vegan Collagen Market Segmentations

By Product Type

- Vegan Collagen Powders

- Vegan Collagen Capsules & Tablets

- Vegan Collagen Drinks & Shots

- Vegan Collagen Creams & Serums

- Vegan Collagen Functional Foods (Bars, Gummies)

By Application

- Nutraceuticals & Dietary Supplements

- Cosmetics & Personal Care

- Food & Beverages

- Pharmaceuticals

- Biomedical Applications

By Distribution Channel

- Online Retail (E-commerce & D2C)

- Pharmacies & Specialty Health Stores

- Supermarkets & Hypermarkets

- B2B (Clinics, Hospitals, Beauty Brands)

Regional Insights

North America

North America leads the global vegan collagen market, with the U.S. contributing more than 30% of global revenue in 2025. The region’s growth is driven by a strong health and wellness trend, a high vegan population, and increasing adoption of functional supplements and beverages. High disposable income, advanced biotech infrastructure, and robust awareness campaigns on plant-based nutrition further support market penetration. Canada shows steady growth due to rising nutraceutical innovations and increasing demand for anti-aging and beauty supplements.

Europe

Europe holds a 28% share of the global market, led by Germany, the U.K., and France. The growth is primarily driven by consumer preference for cruelty-free, ethical, and clean-label skincare products, which has fueled demand for vegan collagen in cosmetics. EU-funded biotechnology projects, strong regulatory support for sustainable ingredients, and rising awareness of plant-based nutrition contribute to regional adoption. Anti-aging products and functional supplements continue to be key growth levers for cosmetics and nutraceutical applications.

Asia-Pacific

Asia-Pacific is the fastest-growing region, projected to expand at over 35% CAGR. China and Japan dominate beauty-focused collagen demand, while India’s growing vegan population and investment in biotechnology research make it a future growth hub. South Korea, a K-beauty leader, is rapidly integrating vegan collagen into skincare products. Growth is supported by a rising middle class, increasing awareness of anti-aging products, urbanization, and digital adoption, enabling online access to premium collagen products.

Latin America

Latin America is in an emerging phase but shows strong growth potential, particularly in Brazil and Mexico. The region’s adoption is fueled by rising vegan diets, increasing disposable incomes, and the expansion of e-commerce platforms that enable easier access to vegan collagen products. Health-conscious consumer behavior and interest in anti-aging skincare are also contributing to the adoption of supplements and topical formulations.

Middle East & Africa

MEA represents a smaller share of the global market but demonstrates a growing demand for cruelty-free and natural products, particularly in the UAE, Saudi Arabia, and South Africa. Rising disposable incomes, growing awareness of plant-based and ethical wellness products, and import-driven supply chains are key growth drivers. The market is further supported by increasing urbanization and the adoption of international beauty and health trends.

Key Players in the Vegan Collagen Market

- Geltor Inc.

- Jland Biotech

- Amino Co.

- Collplant Biotechnologies Ltd.

- Modern Meadow

- Ecovative Design

- Vital Proteins (vegan range)

- NutraIngredients Collagen Solutions

- JBS Biotech Innovation

- Conagen Inc.

- FermentationExperts

- PlantFusion

- Herbaland Naturals

- Sunwarrior

- MyProtein (Vegan line)