Studio Lighting Market Size

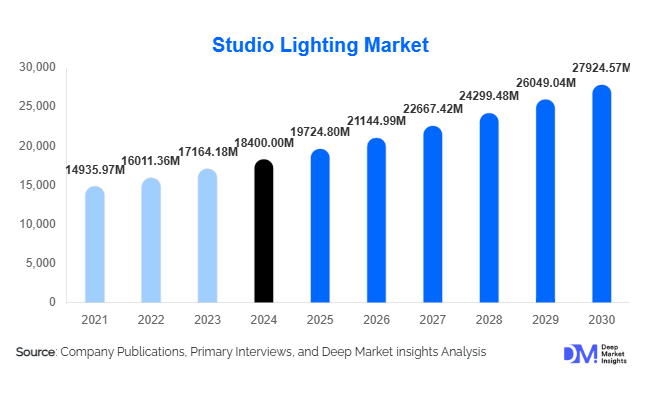

According to Deep Market Insights, the global studio lighting market size was valued at USD 18,400 million in 2025 and is projected to grow from USD 19,724.8 million in 2026 to reach USD 27,924.57 million by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). The market growth is primarily driven by the increasing adoption of LED and smart lighting solutions, rising demand from media, entertainment, and e-commerce industries, and the expansion of digital content creation platforms requiring professional-grade illumination.

Key Market Insights

- LED-based studio lighting continues to dominate the market, offering energy efficiency, longevity, and precise color rendering preferred by professional photographers and videographers.

- Portable and IoT-integrated lighting systems are rapidly gaining traction, allowing content creators to adjust lighting wirelessly and automate studio setups for efficiency.

- North America holds the largest market share, led by the U.S., due to strong media and entertainment production industries, along with widespread adoption of high-end studio solutions.

- Asia-Pacific is the fastest-growing region, driven by rising demand for digital content, e-commerce product photography, and social media influencer setups in China, India, and Japan.

- Europe shows steady adoption, with Germany and the U.K. driving demand for professional and broadcast studio lighting solutions, emphasizing quality and technological innovation.

- Technological advancements, including smart lighting, bi-color LEDs, and wireless control systems, are reshaping studio setups for photography, videography, and live streaming applications.

Studio Lighting Market Trends

LED Lighting Continues to Dominate Professional Studios

The transition from conventional tungsten and fluorescent lighting toward LED-based solutions remains one of the most significant trends shaping the studio lighting market. Professional photographers, filmmakers, broadcasters, and content creators increasingly prefer LED fixtures due to their lower energy consumption, longer operating life, superior color rendering capabilities, and reduced heat generation. Modern LED systems offer adjustable color temperatures, RGB capabilities, wireless control, and integration with production software, enabling greater creative flexibility. Manufacturers are also introducing compact and portable LED solutions designed specifically for mobile content creation and remote production environments. As sustainability becomes a higher priority across production facilities, LED adoption is expected to continue replacing legacy lighting technologies globally.

Rise of Virtual Production and Smart Lighting Integration

The rapid expansion of virtual production studios is reshaping lighting requirements across the film and television industry. LED volume stages require advanced lighting systems capable of synchronizing with digital environments rendered in real time. Manufacturers are responding by introducing smart lighting platforms that integrate with virtual production software, enabling dynamic color adjustments and automated scene matching. AI-powered lighting control systems are also gaining traction by helping production teams optimize illumination settings, reduce setup times, and improve workflow efficiency. This trend is particularly prominent among major film studios, streaming platforms, and premium content producers seeking greater production flexibility and cost efficiency.

Studio Lighting Market Drivers

Expansion of Digital Content Creation Industry

The exponential growth of digital content creation across YouTube, Instagram, TikTok, podcasts, online education platforms, and corporate communication channels continues to fuel demand for professional studio lighting equipment. Content quality has become a critical factor influencing audience engagement and platform monetization, encouraging creators and businesses to invest in advanced lighting systems. Small businesses, educational institutions, and independent professionals are increasingly establishing dedicated production spaces equipped with professional-grade lighting infrastructure.

Growing Adoption of Energy-Efficient LED Technologies

LED lighting technology has become the preferred choice across studio environments due to its superior energy efficiency, lower maintenance requirements, longer lifespan, and improved color consistency. Compared to traditional lighting systems, LED solutions significantly reduce operating costs while delivering enhanced performance. Continuous advancements in LED chip efficiency, wireless controls, and intelligent lighting management are further accelerating adoption among professional and semi-professional users. Government initiatives promoting energy-efficient technologies are also supporting market expansion.

Studio Lighting Market Restraints

High Initial Capital Investment Requirements

Professional-grade studio lighting systems, particularly those designed for broadcast production, cinematic applications, and virtual production environments, often require substantial upfront investment. Comprehensive studio setups involving lighting fixtures, modifiers, controllers, mounting systems, and power solutions can create budget constraints for small businesses, freelance creators, and emerging production houses. This cost barrier continues to limit adoption among price-sensitive customer segments.

Rapid Technology Obsolescence

The pace of innovation within lighting technology creates challenges for end users seeking long-term equipment investments. Frequent improvements in LED efficiency, wireless communication protocols, software integration capabilities, and AI-driven controls can shorten replacement cycles and increase ownership costs. Production companies must continuously upgrade equipment to remain competitive, particularly in industries where visual quality standards evolve rapidly.

Studio Lighting Market Opportunities

Expansion of Creator Economy and Live Streaming Infrastructure

The global creator economy is generating substantial opportunities for studio lighting manufacturers. Millions of influencers, streamers, podcasters, educators, and freelance content creators are upgrading their production capabilities to improve content quality and audience engagement. Demand for compact, affordable, and user-friendly lighting systems continues to increase, particularly in emerging economies where digital content monetization is accelerating. Manufacturers offering integrated lighting ecosystems with app-based controls and cloud connectivity are well positioned to capitalize on this expanding customer base.

Growth of Virtual Production Studios

Virtual production technologies are becoming increasingly mainstream within film, television, advertising, and gaming industries. The development of LED volume stages requires highly specialized lighting systems capable of interacting seamlessly with digital backgrounds and real-time rendering platforms. Lighting manufacturers that develop products optimized for virtual production workflows, color synchronization, and automated scene matching are expected to benefit from premium pricing opportunities and long-term demand growth.

Product Type Insights

Continuous LED lights dominate the studio lighting market, accounting for 55% of the 2025 market. Their energy efficiency, portability, and consistent color rendering make them ideal for photography studios, online content creation, and broadcast studios. Flash lighting, including monolights and pack-and-head systems, serves specialized applications such as high-speed photography and commercial shoots, but represents a smaller share due to higher initial costs and limited portability.

Application Insights

Photography studios remain the largest application segment (40% of market share), driven by fashion, product, and corporate photography needs. Videography studios are rapidly adopting LED and portable lighting kits for film production, live streaming, and TV content creation. Broadcast studios rely on high-end, IoT-integrated lighting for consistent quality in news, sports, and entertainment shows. Emerging applications include e-learning studios, influencer content rooms, and live streaming setups, expanding the market scope beyond traditional photography and videography.

Distribution Channel Insights

Online platforms lead studio lighting distribution (35% of 2025 sales) due to convenience, product variety, and direct-to-consumer availability. Specialty retail stores and direct sales channels remain significant for high-end and professional lighting solutions. Increasing digital marketing, influencer endorsements, and e-commerce expansion are shaping consumer purchase behavior, particularly among freelancers, small studios, and educational institutions seeking affordable yet high-quality solutions.

End-Use Insights

Media and entertainment dominate end-use applications (45% market share), fueled by demand for high-quality content in film, television, and streaming platforms. Advertising, marketing, and e-commerce product photography are fast-growing segments, requiring precise and adaptable lighting setups. Educational institutions, live-streaming studios, and corporate content creation are emerging users, reflecting the growing adoption of portable and smart studio lighting systems for diverse applications.

| By Technology | By End-use | By Form Factor |

|---|---|---|

|

|

|

Regional Insights

North America

North America holds the largest market share (30% in 2025), led by the U.S. due to its strong media, entertainment, and e-commerce sectors. Professional studios and content creators prioritize advanced LED and IoT-enabled lighting solutions. Canada also shows steady growth, with investments in film production and online content creation supporting the regional market.

Europe

Europe accounts for 25% of the global market, with Germany, the U.K., and France driving demand. Broadcasters and commercial studios invest in high-end, energy-efficient lighting solutions, emphasizing quality and technological integration. The region demonstrates moderate growth with the adoption of smart lighting systems and bi-color LEDs.

Asia-Pacific

Asia-Pacific is the fastest-growing region (10% CAGR), led by China and India. Rapid adoption in digital media, influencer content creation, and e-commerce photography is driving demand for affordable yet professional lighting solutions. Japan and South Korea represent mature markets, focused on high-quality, technologically advanced products.

Latin America

Brazil and Argentina are emerging markets for studio lighting, primarily for photography and content creation studios. Growth is supported by rising e-commerce adoption and small studio setups requiring professional-grade lighting.

Middle East & Africa

The Middle East, led by the UAE and Saudi Arabia, shows increasing demand for premium studio lighting driven by media, corporate, and event production. Africa remains a niche market, with gradual adoption in commercial photography and educational institutions.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Studio Lighting Market

- Aputure

- Profoto

- Godox

- Broncolor

- Dedolight

- Nanlite

- Westcott

- Kino Flo

- Rotolight

- Falcon Eyes

- Elinchrom

- Arri

- Yongnuo

- Lume Cube

- Photogenic

Recent Developments

- In June 2025, Aputure launched a new line of bi-color LED panels with app-controlled wireless settings for small studios and live streaming applications.

- In March 2025, Profoto introduced a compact portable lighting kit targeting e-commerce product photography, emphasizing energy efficiency and color accuracy.

- In January 2025, Godox expanded its LED lighting portfolio in Asia-Pacific, providing affordable solutions for content creators and educational institutions.