Strength Training Equipment Market Size

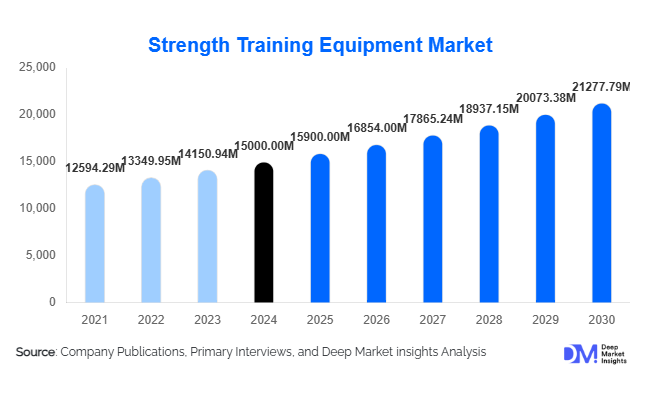

According to Deep Market Insights, the global strength training equipment market size was valued at USD 15,000 million in 2025 and is projected to grow from USD 15,900 million in 2026 to reach USD 21,277.79 million by 2031, expanding at a CAGR of 6% during the forecast period (2026–2031). Growth in the strength training equipment market is driven by rising health awareness, the expanding home fitness segment, and increasing adoption of smart, connected equipment across commercial and residential settings.

Key Market Insights

- Free weights dominate the product landscape, accounting for nearly 40% of the global market in 2025, driven by affordability, versatility, and wide adoption across gyms and homes.

- Commercial fitness centers remain the largest end-user group, contributing over 60% of global revenues, though residential demand is growing fastest post-pandemic.

- North America leads the global market with a 40% share in 2025, while Asia-Pacific is the fastest-growing region at a 7–9% CAGR.

- Smart and connected equipment is reshaping consumer preferences, with IoT-enabled resistance machines and app-integrated free weights gaining traction.

- Mass-market and mid-tier products account for over two-thirds of global revenues, though premium and luxury equipment segments are seeing faster growth.

- Supply chain pressures and raw material price fluctuations remain challenges, impacting pricing and margins across manufacturers.

Strength Training Equipment Market Trends

Smart & Connected Equipment on the Rise

Technology integration has become a defining trend, with consumers demanding performance tracking, virtual coaching, and connectivity with wearables and fitness apps. IoT-enabled machines, smart adjustable dumbbells, and app-synced resistance bands are growing in popularity. This trend is reshaping how consumers engage with equipment, enhancing personalization and providing new revenue streams for manufacturers via subscription services and digital ecosystems.

Shift Toward Home Fitness Solutions

The post-pandemic fitness landscape continues to support demand for compact, multifunctional, and space-saving home equipment. Adjustable free weights, foldable benches, and hybrid racks are increasingly marketed to urban consumers. Bundled digital training subscriptions further add value, encouraging households to replicate gym experiences at home. This segment is expected to be the fastest-growing end-use category through 2031.

Strength Training Equipment Market Drivers

Rising Health and Fitness Awareness

The global rise in lifestyle diseases and obesity, combined with growing awareness of strength training’s role in long-term wellness, is fueling demand across age groups. Strength training is increasingly promoted for bone health, muscle mass preservation, and injury prevention, driving adoption beyond athletes and fitness enthusiasts.

Hybrid Fitness Models and Subscription Ecosystems

Consumers are embracing hybrid fitness models that combine gym memberships with home training. This has increased demand for both commercial-grade and household-friendly strength equipment. Subscription-based ecosystems that bundle digital coaching, progress tracking, and virtual communities are reinforcing long-term demand for hardware.

Premiumization and Innovation

Consumers are increasingly willing to invest in premium products offering superior durability, design, and advanced features. Innovative materials, modular designs, and eco-friendly manufacturing practices are differentiating products in a competitive market while strengthening brand loyalty and margins.

Strength Training Equipment Market Restraints

High Equipment Costs

Strength training equipment, particularly resistance machines and smart systems, involves significant upfront costs. This limits adoption in price-sensitive markets and among budget-conscious households. Rising raw material prices and transportation costs add further pressure, making affordability a persistent barrier.

Market Saturation in Mature Economies

North America and Western Europe are highly mature markets, with widespread gym penetration and home fitness adoption. Growth in these regions is primarily replacement-driven, making it difficult for new entrants to capture market share without significant innovation or pricing advantage.

Strength Training Equipment Market Opportunities

Emerging Market Expansion

Asia-Pacific, Latin America, and the Middle East present untapped growth opportunities due to rising disposable incomes, growing urbanization, and government-led wellness initiatives. Establishing localized manufacturing and cost-optimized product lines can enable companies to capture these high-growth regions.

Sustainability and Eco-Friendly Manufacturing

Consumer demand for sustainable products is driving interest in recycled materials, energy-efficient production, and longer product lifecycles. Brands that integrate eco-friendly materials and circular economy models, such as refurbishment or leasing programs, can differentiate themselves in competitive markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 15000 Million |

| Market Size in 2026 | USD 15900 Million |

| Market Size in 2031 | USD 21277.79 Million |

| CAGR | 6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Free weights lead the market, accounting for a 40% share in 2025, owing to their versatility, affordability, and compatibility with diverse workout styles. Weight machines and cable systems follow, favored in commercial gyms for safety and standardization. Benches and racks remain essential accessories, particularly in institutional and sports training settings. Portable equipment like resistance bands and kettlebells is witnessing strong growth in the residential and functional training categories.

End-User Insights

Commercial gyms and health clubs dominate end-use demand, contributing over 60% of revenues in 2025. This segment is driven by bulk purchases, frequent upgrades, and premiumization. Residential demand, however, is expanding fastest, supported by e-commerce growth and hybrid fitness models. Institutional buyers, including schools, rehabilitation centers, and sports organizations, represent a stable but smaller share, with procurement cycles tied to budgets and government support.

Distribution Channel Insights

Offline channels continue to account for 65% of global revenues, as buyers of heavy equipment prioritize in-person evaluation, installation services, and long-term warranties. However, online platforms are gaining share rapidly, supported by direct-to-consumer models, transparent pricing, and bundled digital subscriptions. The growth of e-commerce logistics networks is enabling the delivery of bulky items, positioning online as a future growth driver.

Explore more data points, trends and opportunities Download Free Sample Report

Strength Training Equipment Market Segmentations

By Equipment

- Free Weights

- Machines

- Resistance Bands

By End-user

- Commercial Gyms

- Home

- Rehab

By Distribution

- Dealers

- Direct

- Online

Regional Insights

North America

North America leads the global market with a 40% share in 2025, dominated by the U.S. Rising demand for premium and connected equipment, coupled with established gym culture, underpins steady growth. However, saturation limits CAGR to 4% through 2031, with replacement demand as the primary driver.

Europe

Europe holds 30% of global revenues in 2025, with strong markets in Germany, the U.K., and France. Focus on sustainability, premium fitness experiences, and home adoption drives regional demand. CAGR is projected at 4–6% through 2031.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at a 7–9% CAGR, led by China, India, Japan, and South Korea. Rising disposable incomes, expanding fitness chains, and government health campaigns are boosting demand. India stands out as the fastest-growing country within APAC.

Latin America

Latin America contributes 6% of global revenues in 2025, led by Brazil and Argentina. Demand for affordable equipment and the growth of boutique gyms support steady expansion at a 5–6% CAGR.

Middle East & Africa

MEA holds 4% of global revenues, with GCC countries and South Africa driving demand. Investment in luxury gyms, wellness tourism, and fitness infrastructure supports growth, though dependency on imports remains high.

Key Players in the Strength Training Equipment Market

- Life Fitness

- Technogym

- Precor

- Nautilus

- Johnson Health Tech

- Rogue Fitness

- ICON Health & Fitness

- Core Health & Fitness

- Eleiko

- Hammer Strength

- Body-Solid

- Cybex International

- Torque Fitness

- Matrix Fitness

- Hoist Fitness