Smart Pet Collar Market Size

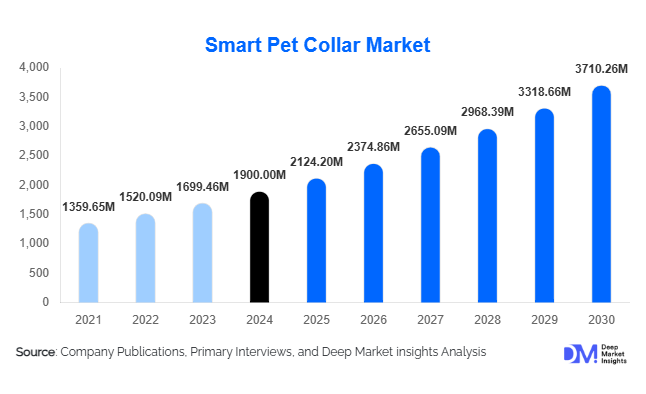

According to Deep Market Insights, the global Smart Pet Collar market size was valued at USD 1,900 million in 2025 and is projected to grow from USD 2,124.2 million in 2026 to reach USD 3,710.26 million by 2031, expanding at a CAGR of 11.8% during the forecast period (2026–2031). The smart pet collar market growth is primarily driven by the increasing adoption of connected devices, rising urban pet ownership, and growing awareness about pet health monitoring and safety solutions.

Key Market Insights

- GPS-enabled and health-monitoring collars dominate adoption, providing real-time tracking, vital monitoring, and activity insights for pets, particularly dogs and cats.

- North America remains the largest market, driven by high disposable incomes, technological adoption, and widespread e-commerce penetration.

- APAC is the fastest-growing region, led by China and India, due to rising urban pet ownership and expanding online retail channels.

- Integration with AI and IoT technologies is creating smarter collars capable of predictive health analytics and enhanced owner engagement.

- Online retail dominates distribution, accounting for over 55% of global sales, supported by convenient purchasing and direct-to-consumer platforms.

- Veterinary clinics and pet service providers are increasingly adopting smart collars for professional pet health monitoring, expanding end-use applications.

Smart Pet Collar Market Trends

AI-Enabled Health and Activity Monitoring

Smart pet collars are increasingly leveraging AI and connected technologies to provide predictive health analytics, behavioral monitoring, and activity tracking. Advanced sensors measure heart rate, body temperature, and sleep patterns, while AI algorithms alert owners to potential health concerns. Some collars integrate with mobile apps and IoT ecosystems, allowing real-time updates and long-term tracking of pet wellness. This trend appeals to tech-savvy pet owners seeking data-driven insights and proactive pet care solutions, particularly in North America and Europe.

IoT and Mobile Connectivity Integration

Collars with cellular, Wi-Fi, and Bluetooth connectivity enable real-time location tracking, automated activity logging, and integration with smart home devices. Mobile app connectivity allows pet owners to monitor multiple pets simultaneously, set geofences, and receive alerts for abnormal activity. Hybrid collars combining multiple connectivity technologies are gaining traction, enhancing adoption across urban and suburban regions, and bridging gaps where Wi-Fi or Bluetooth alone is insufficient.

Smart Pet Collar Market Drivers

Rising Pet Ownership and Humanization Trends

Increasing global pet populations, particularly in urban centers, are driving demand for smart collars. Owners treat pets as family members, investing in safety, activity monitoring, and health solutions. Dogs dominate the market, accounting for 60% of the animal-type segment in 2025, as owners seek GPS-enabled collars for outdoor safety and activity tracking.

Technological Advancements in Wearable Devices

The proliferation of IoT-enabled, GPS-tracked, and AI-driven collars is transforming pet care. Features like heart rate monitoring, geofencing, and behavior alerts differentiate products in a competitive market. Cellular collars, representing 35% of the connectivity segment, enable long-range tracking, fueling adoption in regions with advanced mobile infrastructure.

Expansion of E-commerce Channels

Online retail dominates global sales, accounting for over 55% in 2025. E-commerce platforms provide extensive product selection, pricing transparency, and customer reviews, facilitating rapid adoption of smart collars. Direct-to-consumer strategies allow brands to showcase AI-enabled and premium collars to a tech-savvy audience.

Smart Pet Collar Market Restraints

High Product Costs

Advanced collars, particularly those with GPS, cellular connectivity, and AI features, are costly, limiting adoption in price-sensitive markets. Premium pricing restricts penetration in emerging economies and among cost-conscious pet owners.

Battery Life and Maintenance Challenges

Smart collars require frequent charging or battery replacement, which can be inconvenient for pet owners. Limited battery life reduces the effectiveness of continuous health and location monitoring, potentially hindering long-term adoption.

Smart Pet Collar Market Opportunities

Integration with AI and IoT Ecosystems

Manufacturers can develop advanced collars with AI predictive analytics and IoT connectivity, allowing integration with mobile apps, smart homes, and veterinary platforms. These innovations provide enhanced insights into pet health, automated alerts, and personalized recommendations, creating premium product differentiation and additional revenue streams.

Expansion in Emerging Markets

Regions such as India, China, and Brazil are experiencing rising pet ownership and growing e-commerce penetration. Localized marketing, partnerships with veterinary clinics, and targeted product launches can help brands capture early market share. Urbanization, rising disposable income, and growing awareness of pet wellness are key enablers for market expansion in these regions.

Regulatory Support and Government Initiatives

Policies promoting digital pet identification and welfare are encouraging adoption of smart collars. Collaboration with authorities for pilot programs, certifications, and public awareness campaigns can strengthen brand credibility and consumer trust. Such initiatives create opportunities for manufacturers to participate in government-backed projects and public-private partnerships.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1900 Million |

| Market Size in 2026 | USD 2124.2 Million |

| Market Size in 2031 | USD 3710.26 Million |

| CAGR | 11.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

GPS-enabled collars dominate the product type segment, accounting for 42% of the global market in 2025. They are preferred for real-time tracking and pet safety, particularly in urban areas. Health-monitoring collars are also gaining traction due to rising awareness of pet wellness. Activity-tracking collars and RFID-enabled collars are niche but growing, as owners increasingly demand multi-functional devices that integrate tracking, health, and identification features.

Connectivity Technology Insights

Cellular collars are the leading technology, capturing 35% of the connectivity segment in 2025. Their ability to provide real-time updates over long distances makes them preferable for outdoor and urban pet owners. Bluetooth-based and Wi-Fi collars remain popular for indoor or short-range monitoring, while hybrid collars combining multiple technologies are emerging as the next growth frontier.

Animal Type Insights

Dogs account for 60% of the animal-type market, reflecting the high investment owners make in their pets’ safety and wellness. Cats are gradually adopting smart collars, particularly for indoor-outdoor monitoring. Other pets, including rabbits and exotic animals, represent a smaller but growing segment, primarily in urban households with niche interests.

Distribution Channel Insights

Online retail is the leading distribution channel, representing 55% of global sales. E-commerce allows pet owners to compare products, access real-time reviews, and purchase premium collars conveniently. Offline retail contributes 30% and caters to first-time buyers and in-store demonstrations. Veterinary clinics and pet service providers account for 15%, offering professional adoption for health and behavioral monitoring applications.

Explore more data points, trends and opportunities Download Free Sample Report

Smart Pet Collar Market Segmentations

By Function

- GPS tracking

- Health & activity monitoring

- Training & behavior control

By Connectivity

- Bluetooth-only

- GPS/LTE-enabled

- Hybrid (BLE + cloud)

By Pet type

- Dogs

- Cats

- Small pets & others

Regional Insights

North America

North America holds the largest market share at 38% in 2025. The U.S. drives growth, with high disposable income, urban pet populations, and advanced technological infrastructure supporting adoption. Canada also shows strong demand, particularly for GPS-enabled collars. Customization, AI analytics, and integration with mobile apps are key trends in this region.

Europe

Europe accounts for 28% of the market, led by Germany, the U.K., and France. Demand is driven by health-monitoring and activity-tracking collars, rising urbanization, and awareness about pet wellness. The region favors eco-friendly, sustainable, and technologically advanced smart collars.

Asia-Pacific

APAC is the fastest-growing region, with China and India as key markets. Rapid urbanization, growing middle-class affluence, and increasing e-commerce penetration fuel adoption. Japanese and Australian markets are mature, with steady demand for advanced features such as health monitoring and multi-connectivity collars.

Latin America

Brazil, Argentina, and Mexico are the main contributors, with rising interest in premium collars and online retail. Growth is moderate but supported by increasing pet care awareness.

Middle East & Africa

The Middle East, led by the UAE and Saudi Arabia, shows rising adoption due to high-income populations and interest in premium pet care. Africa remains a small but emerging market with opportunities in urban centers and for export-driven products.

Key Players in the Smart Pet Collar Market

- Whistle

- FitBark

- Garmin

- Tractive

- PetPace

- Link AKC

- Sure Petcare

- Pawtrack

- Pawfit

- Petfon

- Invoxia

- Kippy

- Tagg

- Petcube

- Pod Trackers

Recent Developments

- In May 2025, Whistle launched a new AI-enabled GPS collar series with predictive health analytics and mobile app integration for dogs and cats.

- In April 2025, Tractive expanded its cellular collar offerings to APAC markets, targeting high-growth regions like India and China with e-commerce-focused campaigns.

- In February 2025, Garmin introduced a hybrid collar combining GPS, activity monitoring, and Wi-Fi connectivity, enhancing multi-pet tracking capabilities for urban households.