Smart Home Installation Service Market Size

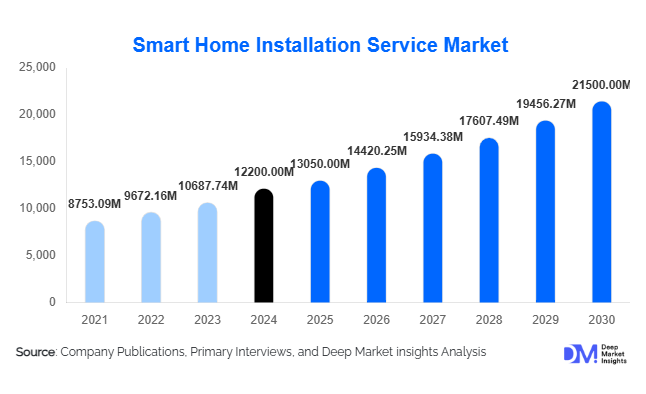

According to Deep Market Insights, the global smart home installation service market size was valued at USD 12,200 million in 2025 and is projected to grow from USD 13,050 million in 2026 to reach USD 21,500 million by 2031, expanding at a CAGR of 10.5% during the forecast period (2026–2031). The market growth is primarily driven by increasing adoption of IoT-enabled devices, rising demand for home automation, and the need for energy-efficient and secure smart home systems globally.

Key Market Insights

- Residential properties dominate the market, with high demand for smart security, lighting, HVAC, and energy management solutions among urban households.

- Integration with energy management and AI-enabled devices is accelerating, enabling consumers to optimize energy use and simplify home control through centralized platforms.

- North America holds the largest market share, driven by early adoption, high disposable incomes, and strong security awareness.

- Asia-Pacific is the fastest-growing region, led by urbanization, smart city initiatives, and increasing middle-class adoption in China and India.

- Government programs and smart city initiatives, such as “Make in India” and smart urban infrastructure projects, are fueling installation service demand.

- Technological integration, including AI, voice assistants, IoT hubs, and mobile app-enabled management, is enhancing customer engagement and driving market expansion.

Smart Home Installation Service Market Trends

AI and IoT Integration Enhancing Smart Homes

Smart home installation services are increasingly integrating AI-driven devices and IoT-enabled platforms. This allows homeowners to manage lighting, security, HVAC, and entertainment systems through centralized mobile applications. Predictive analytics, energy optimization, and voice assistant integration have made installations more complex and reliant on professional services. This trend has particularly boosted the demand for retrofit installations in existing homes, as consumers seek to upgrade older systems to modern, intelligent setups.

Rising Retrofits and Multi-System Integrations

With the growing number of existing homes lacking smart infrastructure, retrofit installations have emerged as a major growth driver. Multi-system integration, including security, energy management, and entertainment, requires skilled professionals, creating opportunities for specialized service providers. Consumers are increasingly seeking end-to-end solutions where devices from multiple brands are seamlessly integrated into a single ecosystem, making professional installations essential.

Smart Home Installation Service Market Drivers

Growing Smart Device Adoption

The proliferation of smart devices such as thermostats, locks, cameras, and lighting systems is a primary driver. As households adopt multiple devices, the need for professional installation and integration services increases. This trend is particularly pronounced in high-income urban areas in North America and Europe, where consumers demand reliable, secure, and fully integrated smart home solutions.

Security and Energy Efficiency Concerns

Heightened security concerns and the desire to reduce energy consumption are motivating homeowners to invest in smart home systems. Professional installers are essential to ensure proper integration and configuration of security cameras, alarms, and energy-saving devices, boosting service demand across residential and commercial properties.

Smart City and Government Initiatives

Government programs and smart city initiatives encourage smart home adoption in both residential and public infrastructure sectors. Projects promoting energy efficiency, home automation, and urban digitization create lucrative opportunities for professional installation services, particularly in emerging economies such as India and China.

Smart Home Installation Service Market Restraints

High Initial Costs

The high costs of devices and professional installations remain a significant restraint, particularly in price-sensitive regions. Consumers in developing countries may delay adoption due to budget constraints, limiting the market’s immediate growth potential.

Complexity of Integration

Compatibility issues across devices and platforms pose challenges for installers. Lack of standardized protocols increases technical complexity and operational costs, making adoption slower in markets where consumer knowledge about smart homes is limited.

Smart Home Installation Service Market Opportunities

Expansion in Emerging Markets

Rapid urbanization and rising middle-class incomes in APAC and LATAM present major growth opportunities. China, India, Brazil, and Mexico are witnessing increasing demand for smart home installations in both new constructions and retrofits. Service providers can capture these markets by offering cost-effective, scalable solutions.

Integration with Renewable Energy Systems

As consumers prioritize energy efficiency, integrating solar systems, smart meters, and battery storage with home automation presents opportunities for differentiated service offerings. Bundled installations that combine security, lighting, and energy management systems are likely to gain traction.

Technological Innovations and AI-Enabled Services

Advanced AI, predictive maintenance, and voice-assisted home management systems are creating new installation requirements. Service providers offering seamless integration of these technologies can differentiate themselves and gain a competitive advantage in high-growth markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 12200 Million |

| Market Size in 2026 | USD 13050 Million |

| Market Size in 2031 | USD 21500 Million |

| CAGR | 10.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Service Type Insights

Installation services dominate the market, representing 42% of the 2025 market. The technical complexity of integrating multiple devices into a centralized system drives professional service demand. Consultation and maintenance services are also growing, but remain secondary compared to core installation operations.

Device Category Insights

Security and surveillance systems lead globally, with a 30% share of the 2025 market. Rising security concerns and IoT-enabled camera adoption drive this trend. Energy management and entertainment systems are growing rapidly, particularly in regions focusing on energy efficiency and smart living.

End-User Insights

Residential end-users account for 65% of total demand in 2025. Urban homeowners and apartment dwellers are driving growth, especially in North America, Europe, and APAC. Commercial and government installations are increasing due to smart building initiatives and municipal projects.

Installation Type Insights

Retrofit installations represent 55% of the market, as older homes seek upgrades for smart energy, security, and entertainment systems. New construction installations are growing steadily, particularly in APAC, where smart city projects are emerging.

Explore more data points, trends and opportunities Download Free Sample Report

Smart Home Installation Service Market Segmentations

By Service Type

- Consultation & Planning Services

- Installation Services

- Integration Services

- Maintenance & Support Services

By Device Category

- Security & Surveillance Systems

- Lighting & HVAC Control Systems

- Home Entertainment Systems

- Smart Appliances & Kitchen Devices

- Energy Management Systems

By End-User

- Residential

- Commercial

- Government & Public Infrastructure

By Installation Type

- New Construction

- Retrofit Installation

Regional Insights

North America

North America remains the largest market (35% share in 2025), led by the U.S. High disposable income, security concerns, and early adoption of smart technologies drive demand. Canada shows steady growth, primarily in retrofit projects.

Europe

Europe accounts for 28% of the market, with Germany, the UK, and France leading adoption. Retrofit demand and energy efficiency initiatives are driving growth, particularly in older housing stock. Germany is the fastest-growing European market due to government incentives for energy-efficient home automation.

Asia-Pacific

APAC is the fastest-growing region, with adoption driven by China, India, Japan, and South Korea. Urbanization, rising middle-class incomes, and smart city initiatives contribute to double-digit CAGR growth. China leads residential adoption, while India benefits from retrofit programs and government incentives.

Middle East & Africa

The UAE and Saudi Arabia show increasing demand in luxury residential and commercial installations. Government smart city programs and high disposable incomes support adoption. Africa’s smart home adoption is emerging slowly, focused on high-end residences.

Latin America

Brazil and Mexico are the largest markets, with growing demand for security and energy management systems. Adoption remains limited by cost sensitivity, but urban residential retrofits are driving growth.

Key Players in the Smart Home Installation Service Market

- Honeywell

- Siemens

- Schneider Electric

- Johnson Controls

- ABB

- Crestron

- Control4

- Legrand

- Somfy

- Bosch

- Savant

- Lutron

- Assa Abloy

- Vivint

- ADT

Recent Developments

- In March 2025, Honeywell launched a new AI-enabled smart home installation package in the U.S., integrating energy management and security solutions.

- In February 2025, Siemens expanded its smart home installation services in Europe, focusing on retrofitting legacy homes with integrated HVAC and lighting systems.

- In January 2025, Vivint announced expansion in APAC, establishing service centers in India and China to meet growing residential retrofit demand.