Slider Zipper Pouch Market Size

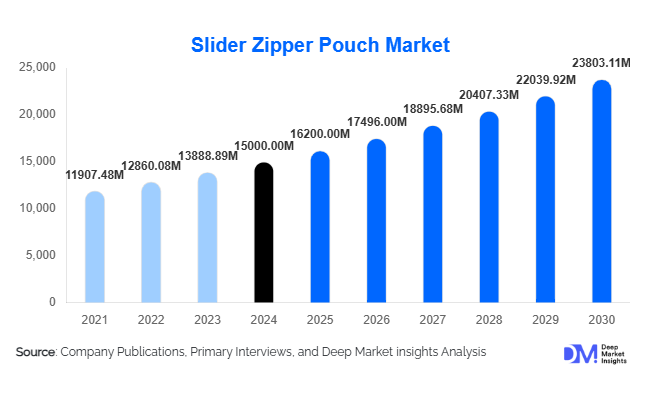

According to Deep Market Insights, the global slider zipper pouch market size was valued at USD 15,000 million in 2025 and is projected to grow from USD 16,200 million in 2026 to reach USD 23,803.11 million by 2031, expanding at a CAGR of 8.0% during 2026–2031. Market growth is driven by the rising demand for convenient, resealable, and sustainable flexible packaging solutions across the food, pharmaceutical, and personal-care industries. Technological innovation in materials, recyclability, and smart packaging features is further transforming the global packaging landscape.

Key Market Insights

- Resealable convenience and consumer-centric packaging are primary drivers, aligning with on-the-go lifestyles and waste-reduction goals.

- Plastic materials (PE/PP) dominate production due to flexibility, cost-efficiency, and compatibility with slider closures.

- Stand-up pouches lead product adoption, favored by global food and pet-food brands for shelf appeal and ease of use.

- Asia-Pacific is the fastest-growing region, driven by rapid retail expansion and packaged-food consumption in China and India.

- North America and Europe collectively account for 55% of the 2025 global market value, supported by a mature packaging infrastructure.

- Sustainability trends, including recyclable mono-material films and PCR content, are reshaping manufacturing and design priorities.

Latest Market Trends

Sustainability and Recyclable Packaging Solutions

Manufacturers are investing heavily in recyclable and bio-based materials to meet evolving environmental regulations and corporate sustainability goals. Mono-material polyethylene and polypropylene pouches are being developed to replace multi-layer laminates that hinder recyclability. Partnerships between packaging firms and polymer producers are advancing the creation of post-consumer-recycled (PCR) slider zipper pouches. Consumers and brand-owners increasingly prefer eco-friendly packaging, boosting demand for compostable, lightweight, and reusable formats that reduce carbon footprint while maintaining product integrity.

Smart and Functional Packaging Integration

The integration of smart features such as QR codes, RFID tags, and tamper-evident sliders is enhancing the functionality of slider zipper pouches. These innovations enable traceability, consumer engagement, and product authentication. Barrier enhancements and vapor-control technologies are improving shelf life for perishable goods. Advanced printing and automation are also streamlining mass customization, enabling brands to create differentiated designs and connect digitally with consumers through interactive packaging experiences.

Slider Zipper Pouch Market Drivers

Growing Preference for Convenience and Resealability

Consumer lifestyles emphasizing portability and portion control have made resealable slider pouches indispensable. Their easy-open and secure closure systems align with modern consumption habits, especially in snacks, pet food, and household products. The ability to maintain freshness and reduce food waste significantly increases consumer satisfaction, reinforcing repeat purchases and brand loyalty.

Expansion of Flexible Packaging Applications

Slider zipper pouches are increasingly replacing rigid containers due to superior material efficiency and lower transportation costs. Industries beyond food, such as healthcare, cosmetics, and electronics, are adopting these formats for hygienic, lightweight, and tamper-evident packaging needs. The expansion into diverse sectors broadens the market base and stabilizes revenue streams across cyclical industries.

Emergence of Emerging Market Demand

Rising disposable incomes and the modernization of retail in Asia-Pacific and Latin America are driving demand for packaged goods. With growing middle-class populations and improved logistics, slider zipper pouch adoption is accelerating. Manufacturers localizing production and distribution in these regions are positioned to capture substantial market share over the next five years.

Market Restraints

Volatility in Raw-Material Prices

Fluctuating polymer and aluminum prices directly impact production costs. As the industry heavily depends on petrochemical inputs, sharp crude oil price swings compress converter margins. Companies face difficulty in cost pass-through, particularly in competitive, price-sensitive consumer-goods markets.

Recycling and Regulatory Compliance Challenges

Multi-layer laminated pouches remain difficult to recycle, raising compliance costs under emerging circular-economy regulations. Governments are tightening mandates on single-use plastics, prompting urgent innovation in recyclable designs. Adapting to these policies requires capital-intensive R&D, which may constrain smaller converters.

Slider Zipper Pouch Market Opportunities

Shift Toward Sustainable and Circular Packaging

Developing recyclable and compostable slider zipper pouches represents a key growth frontier. Investment in mono-material films and biodegradable polymers will create opportunities to serve eco-conscious brands seeking to meet net-zero packaging commitments. This evolution supports premium pricing and long-term partnerships with global FMCG leaders.

Expansion in Emerging Economies

India, China, Brazil, and Southeast Asian countries are seeing explosive packaged-food and personal-care growth. Establishing regional manufacturing hubs enables cost advantages and quicker delivery, allowing companies to address local demand efficiently. Market entrants can capture first-mover advantages by offering affordable slider pouch solutions in these high-volume markets.

Smart Slider Closures and Digital Integration

Innovations such as tactile sliders, multi-track zips, and integrated RFID or QR systems are adding premium functionality. Smart closures not only improve usability but also support brand authentication and interactive marketing, aligning with consumer trends in personalization and digital engagement.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 15000 Million |

| Market Size in 2026 | USD 16200.00 Million |

| Market Size in 2031 | USD 23803.11 Million |

| CAGR | 8.0% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Stand-up slider pouches dominate the market, accounting for roughly 30% of 2025 sales. Their upright display, strong branding surface, and ease of reseal make them ideal for food and pet-food packaging. Other formats, such as flat-bottom and quad-seal pouches, serve specialized applications requiring additional stability or higher barrier protection.

Material Insights

Plastic films (PE and PP) remain the cornerstone of slider zipper pouch manufacturing, holding about 65% of global share in 2025. Their strength, versatility, and compatibility with various slider mechanisms ensure scalability. Paper and aluminum laminates are niche but growing due to sustainability and premium-product demand.

Closure Type Insights

The slider-zip format leads with around 55% market share in 2025. It is preferred for its convenience, durability, and premium feel compared with press-to-close designs. Continuous innovation in slider tracks and ergonomic designs is strengthening its appeal across household and food applications.

End-Use Industry Insights

The food segment represents approximately 45% of market demand in 2025, driven by ready-to-eat snacks, pet food, and frozen products. Pharmaceutical and cosmetic applications are growing fastest, with strong emphasis on hygiene, barrier protection, and tamper evidence. Industrial and electronic applications are emerging as additional niche uses, benefiting from resealability and anti-static protection.

Explore more data points, trends and opportunities Download Free Sample Report

Slider Zipper Pouch Market Segmentations

By Material Type

- Polyethylene (PE)

- Polypropylene (PP)

- Polyethylene Terephthalate (PET)

- Aluminum Foil Laminates

- Paper-Based Slider Pouches

- Biodegradable & Compostable Materials

By Closure Type

- Plastic Sliders

- Metal Sliders

- Press-to-Close Sliders

- Ergonomic Grip Sliders

By Application

- Food & Beverages

- Pharmaceuticals

- Personal Care & Cosmetics

- Household Products

- Pet Food

- Industrial Goods

By Distribution Channel

- B2B (Direct Sales to Manufacturers)

- Retail Packaging Suppliers

- Online Distributors

- Wholesale Packaging Stores

By End-Use Industry

- FMCG

- E-commerce & Logistics

- Healthcare

- Agriculture & Horticulture

- Automotive & Industrial Packaging

Regional Insights

North America

North America accounts for about 30% of the 2025 market (USD 4.5 billion). High consumer awareness and established packaging standards drive steady adoption across the food and pet-care industries. Technological sophistication and sustainability commitments by leading CPG brands maintain regional leadership.

Europe

Europe holds roughly 25% market share (USD 3.8 billion) and prioritizes recyclable, mono-material pouches aligned with EU circular-economy directives. Germany, the U.K., and France spearhead R&D in sustainable flexible packaging, boosting adoption among major retailers and food brands.

Asia-Pacific

APAC represents 28% of the 2025 market value (USD 4.2 billion) and is the fastest-growing region (9–10% CAGR). China and India drive consumption of packaged snacks and personal-care goods. Rapid modernization of packaging infrastructure and expansion of manufacturing capacity sustain regional momentum.

Latin America

Latin America holds about 8–10% (USD 1.2 billion). Brazil and Mexico are key markets supported by expanding retail and food-processing industries. Local pouch production facilities and affordable slider formats are emerging to serve domestic demand.

Middle East & Africa

MEA contributes around 7–8% (USD 1.1 billion) of the global market share. Growth stems from rising packaged-food imports, increasing pet ownership, and modern retail chains in GCC countries and South Africa. Government investment in industrial packaging and logistics supports long-term growth.

Top 15 Companies in the Slider Zipper Pouch Market

- Amcor Plc

- Berry Global Group Inc.

- Coveris Holdings S.A.

- Sonoco Products Company

- Sealed Air Corporation

- Glenroy Inc.

- Printpack Inc.

- Winpak Ltd.

- ProAmpac LLC

- International Plastics Inc.

- American Packaging Corporation

- Constantia Flexibles Group GmbH

- Mondi Plc

- Flair Flexible Packaging Corporation

- Interflex Group Inc.