Rice Water Skincare Market Size

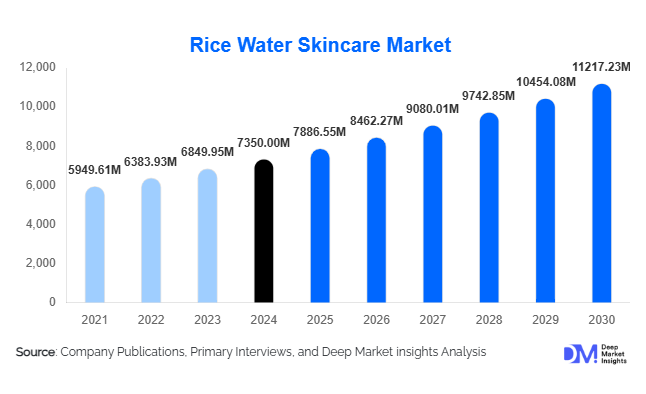

According to Deep Market Insights, the global Rice Water Skincare Market size was valued at USD 7,350 million in 2025 and is projected to grow from USD 7,886.55 million in 2026 to reach USD 11,217.23 million by 2031, expanding at a CAGR of 7.30% during the forecast period (2026–2031). The market growth is primarily driven by rising consumer preference for natural and heritage-based beauty ingredients, rapid expansion of e-commerce channels, and increasing demand for high-performance skincare products infused with traditional Asian formulations.

Key Market Insights

- The growing popularity of clean and natural skincare is fueling demand for rice water-based formulations known for their soothing, hydrating, and brightening properties.

- The Asia-Pacific region dominates the global rice water skincare market due to its strong cultural association with rice-based beauty rituals and the growing demand for premium skincare products.

- Fermented rice water formulations are emerging as the fastest-growing product category, driven by superior efficacy and premium positioning.

- Online retail channels account for approximately 40% of global sales, supported by influencer marketing and direct-to-consumer brand strategies.

- Women consumers represent nearly 70% of the market, reflecting the historical concentration of skincare spending in the female demographic.

- Innovation in ingredient extraction and biotechnology is enabling brands to develop more stable, potent, and sustainable rice water skincare products.

Rice Water Skincare Market Trends

Premiumisation and Ingredient Storytelling

Modern skincare consumers are increasingly demanding transparency and authenticity in their ingredients. Rice water’s roots in Japanese and Korean beauty traditions position it as a heritage ingredient that combines efficacy with cultural depth. Premium brands are leveraging fermented rice water, organic certifications, and traceable sourcing to create storytelling-led marketing campaigns. This trend has encouraged luxury skincare brands to incorporate rice-derived actives into high-end serums and creams, driving category value growth and consumer loyalty.

Technology-Driven Formulations

Emerging technologies such as microencapsulation, fermentation biotechnology, and AI-based skincare personalization are revolutionizing rice water product innovation. These advancements enhance ingredient stability, improve skin absorption, and allow for customizable routines. Smart delivery systems and hybrid formulations combining rice water with peptides, niacinamide, and antioxidants are gaining traction among millennial and Gen Z consumers who seek targeted, multi-benefit skincare solutions. E-commerce platforms further amplify visibility through digital try-ons and AR-based skin analysis tools.

Rice Water Skincare Market Drivers

Rising Demand for Natural and Heritage-Based Ingredients

Consumers are increasingly avoiding synthetic chemicals and gravitating toward natural, traditional remedies. Rice water, rich in amino acids and minerals, aligns perfectly with this clean-beauty trend. Its long-standing presence in Asian skincare culture enhances credibility and consumer trust, making it a preferred natural ingredient for hydration and brightening formulations.

Expanding E-Commerce and Social Media Influence

The proliferation of digital retail and influencer-driven marketing has democratized access to rice water skincare globally. Platforms such as Instagram, TikTok, and YouTube have fueled viral trends showcasing rice water routines, accelerating adoption beyond Asia. Online-exclusive launches and subscription-based skincare models are boosting sales volumes and customer engagement.

Rising Skincare Awareness in Emerging Markets

Rapid urbanization, increasing disposable incomes, and heightened beauty consciousness in emerging economies, particularly in China, India, and Southeast Asia, are driving the uptake of rice water skincare products. Consumers in these regions are adopting multi-step skincare routines inspired by K-beauty and J-beauty traditions, boosting product demand across mass and premium price points.

Rice Water Skincare Market Restraints

Price Pressure and Ingredient Commoditization

As rice water formulations become mainstream, increased competition and imitation are compressing margins. Low-cost entrants and private-label products offering similar claims threaten brand differentiation, forcing established players to focus on innovation and brand equity to maintain profitability.

Formulation and Regulatory Challenges

Maintaining the stability and efficacy of rice water-based ingredients can be challenging due to oxidation and fermentation sensitivity. Furthermore, varying cosmetic regulations across regions complicate compliance. Brands must invest heavily in R&D and quality testing to ensure long-term shelf stability and validated skincare claims.

Rice Water Skincare Market Opportunities

Premium and Fermented Rice Water Innovations

Fermented rice water formulations offer superior antioxidant and brightening benefits, making them ideal for premium product lines. This segment, representing nearly 20% of the market, allows brands to justify higher price points and capture wellness-driven consumers seeking potent natural actives. Investment in R&D to optimize fermentation processes presents a strong opportunity for differentiation.

Emerging Market Expansion and Export Opportunities

Asia-Pacific brands have a competitive edge in heritage-based formulations, creating export potential to Western markets. Simultaneously, international brands entering Asia benefit from local sourcing of rice-based ingredients. This bidirectional trade and rising cross-border e-commerce open lucrative opportunities for both ingredient suppliers and finished product brands.

Integration of Smart Beauty Technologies

Artificial intelligence and personalized skincare diagnostics are enabling brands to tailor rice water products to individual skin profiles. AI-powered recommendation engines, AR skin scanners, and data-driven formulation development can enhance consumer engagement and drive higher conversion rates, especially in online retail environments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 7350 Million |

| Market Size in 2026 | USD 7886.55 Million |

| Market Size in 2031 | USD 11217.23 Million |

| CAGR | 7.30% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Moisturizers and creams dominate the rice water skincare market, accounting for approximately 25% of total revenue in 2025 (USD 1.6 billion). These products form the cornerstone of daily skincare routines, capitalizing on rice water’s hydration benefits. Serums and masks are emerging as high-growth categories driven by consumer preference for concentrated, treatment-based skincare solutions. Toners and cleansers continue to maintain steady demand, while the use of rice water in body lotions and eye-care products is expanding the category’s reach.

Application Insights

Among application segments, products targeting dry skin lead the market, representing roughly 18% of total sales in 2025. Rice water’s natural starches and amino acids help retain moisture and strengthen the skin barrier, making it a preferred ingredient in hydrating formulations. Brightening and anti-aging applications are gaining traction globally, with strong appeal in Asia-Pacific markets known for skin tone and radiance-focused beauty routines.

Distribution Channel Insights

Online retail dominates distribution, contributing about 40% of global sales in 2025. Direct-to-consumer brands leveraging social media and influencer collaborations are driving this growth. Offline retail, particularly through beauty specialty stores and pharmacies, remains critical for premium product trials and consumer trust. Salons and spas are also adopting rice water skincare lines for professional treatments, adding to brand visibility.

Consumer Orientation Insights

Women account for approximately 70% of the total market share, reflecting their higher skincare expenditure and adoption of multi-step routines. However, men’s grooming and unisex skincare lines are growing rapidly as social acceptance of skincare routines among male consumers increases. Brands introducing gender-neutral packaging and fragrance-free rice water formulations are appealing to a broader audience.

Explore more data points, trends and opportunities Download Free Sample Report

Rice Water Skincare Market Segmentations

By Product Type

- Rice Water Cleansers

- Rice Water Toners

- Rice Water Serums & Essences

- Rice Water Moisturizers & Creams

- Rice Water Masks & Exfoliators

- Rice Water Sunscreens

By Formulation Type

- Fermented Rice Water-Based

- Non-Fermented Rice Water-Based

- Blended (Rice Water + Botanical Extracts)

By Skin Concern

- Brightening and Radiance

- Anti-Aging and Firming

- Hydration and Moisturization

- Acne and Oil Control

- Sensitive Skin and Soothing

By Distribution Channel

- Online Retail (E-commerce Platforms, Brand Websites)

- Specialty Beauty Stores

- Supermarkets and Hypermarkets

- Pharmacies and Drugstores

- Departmental Stores

By End-User

- Women

- Men

- Unisex

Regional Insights

Asia-Pacific

Asia-Pacific leads the global rice water skincare market, holding around 35% share (USD 2.27 billion in 2025). Japan, South Korea, and China dominate the market due to their deep-rooted beauty traditions and high per-capita spending on skincare. China is the fastest-growing market, fueled by e-commerce penetration and consumer enthusiasm for natural, effective ingredients. India is emerging as a promising market with local rice-based skincare startups gaining traction.

North America

North America accounts for about 20% of global demand (USD 1.3 billion in 2025). The market is driven by growing consumer preference for clean, vegan, and cruelty-free products. Influencer marketing and collaborations with K-beauty brands have boosted awareness. Premium rice water products retailing through Sephora and Ulta are expanding consumer reach.

Europe

Europe holds roughly 22% market share (USD 1.43 billion). Germany, France, and the U.K. lead demand due to their established natural cosmetics industry. Regulatory emphasis on sustainable sourcing and transparency aligns well with Rice Water’s eco-friendly positioning. Growth is expected at a 7–8% CAGR through 2031.

Middle East & Africa

This region represents approximately a 15% share (USD 975 million in 2025). The GCC countries, led by Saudi Arabia and the UAE, are witnessing rising demand for luxury and organic skincare products. Increasing tourism and retail expansion are fostering new opportunities for premium rice water brands.

Latin America

Latin America contributes about 8% of the global market (USD 520 million in 2025). Brazil and Mexico are the key growth centers, with beauty-conscious consumers adopting natural skincare trends. Online retail and influencer collaborations are accelerating market entry for niche Asian brands.

Key Players in the Rice Water Skincare Market

- SK-II (Procter & Gamble)

- Tatcha (The Estée Lauder Companies)

- Innisfree (Amorepacific Group)

- The Face Shop (LG Household & Health Care)

- Amorepacific

- Laneige

- Sulwhasoo

- COSRX

- Beauty of Joseon

- Haruharu Wonder

- TonyMoly

- Shiseido

- L’Oréal

- Unilever

- Estée Lauder

Recent Developments

- In June 2025, Amorepacific launched a new fermented rice enzyme cream line under Innisfree, targeting premium hydration and anti-aging consumers.

- In April 2025, Tatcha expanded its rice water-based “The Essence” range into new European markets with sustainable packaging initiatives.

- In February 2025, L’Oréal introduced a new rice water brightening line under its Garnier brand, leveraging biotechnology-enhanced rice extract for global mass-market appeal.