Pond Liners Market Size

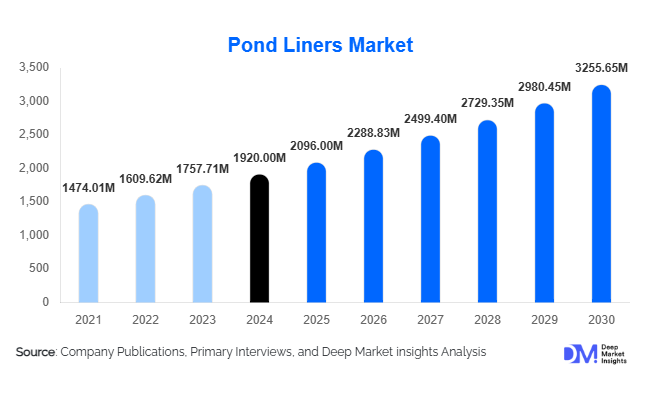

According to Deep Market Insights, the global pond liners market size was valued at USD 1,920 million in 2025 and is projected to grow from USD 2,096.64 million in 2026 to reach USD 3,255.65 million by 2031, expanding at a CAGR of 9.2% during the forecast period (2026–2031). The pond liners market growth is primarily driven by rising investments in water conservation infrastructure, expansion of aquaculture and agricultural water storage systems, and increasing environmental regulations mandating industrial and mining containment solutions.

Key Market Insights

- HDPE liners dominate the global pond liners market, accounting for approximately 38% of total revenue in 2025, owing to superior strength, chemical resistance, and long service life.

- Agriculture and aquaculture applications collectively hold about 45% of the market share, driven by growing water scarcity and rising global demand for efficient irrigation and fish farming systems.

- North America leads the global market, representing around 33% of 2025 revenues due to stringent environmental containment standards and strong industrial adoption.

- Asia-Pacific is the fastest-growing region, fueled by rapid agricultural expansion, aquaculture development, and infrastructure investments across China, India, and Southeast Asia.

- Material innovation and sustainability initiatives, such as composite geomembranes, recycled liners, and sensor-integrated monitoring, are reshaping competitive dynamics.

- Government water-management programs and public infrastructure spending on reservoirs, irrigation ponds, and waste-containment projects are sustaining long-term demand growth.

Latest Market Trends

Advanced Geomembrane Technologies and Smart Liners

Manufacturers are increasingly integrating advanced geomembrane materials, multi-layer composites, and intelligent monitoring systems into pond liners. Smart liners equipped with embedded sensors enable real-time leak detection and performance monitoring, reducing maintenance costs and environmental risk. The development of UV-resistant, thermally stable, and eco-friendly liner formulations is expanding adoption across agriculture, aquaculture, and mining sectors. These advancements also align with global sustainability goals by extending liner lifespan and improving recyclability.

Rising Adoption in Aquaculture and Agricultural Water Storage

As global fish farming and agriculture industries face escalating water scarcity challenges, the use of pond liners in aquaculture and irrigation reservoirs is rapidly expanding. Farmers are increasingly turning to synthetic liners to prevent seepage, maintain water quality, and improve crop yields. Government subsidies for farm pond development, particularly in India and Southeast Asia, are boosting liner demand. The trend toward larger, modular water-retention systems favors durable materials such as HDPE and EPDM, accelerating overall market expansion.

Pond Liners Market Drivers

Growing Agricultural and Aquaculture Demand

Expanding global food production and aquaculture industries are major demand drivers for pond liners. Modern fish farms and agricultural irrigation ponds require impermeable, durable containment solutions to preserve water quality and reduce seepage losses. In 2025, this segment represented nearly 45% of total demand, with Asia-Pacific accounting for a substantial share due to rapid agricultural modernization.

Environmental Regulations and Industrial Containment Requirements

Tighter regulations surrounding waste containment, tailings ponds, and industrial wastewater storage are fueling the adoption of advanced liner systems. Industries such as mining, chemical processing, and oil & gas increasingly rely on HDPE and composite geomembranes to meet environmental compliance standards. This regulatory trend enhances long-term market stability and encourages technological innovation in premium liners.

Urbanization and Landscaping Development

Urban expansion and the popularity of decorative water features in residential and commercial landscaping are supporting incremental growth. Demand for flexible, aesthetic pond liners for water gardens, resorts, and municipal beautification projects adds to the market’s diversity. Though smaller in volume, this segment offers attractive margins and recurring replacement opportunities.

Market Restraints

High Installation and Material Costs

The high upfront cost of durable liner systems and professional installation remains a challenge, particularly for small-scale farmers and landscapers. Material costs for HDPE, EPDM, and composite membranes can be substantial, and site preparation further raises total expenses. Cost sensitivity in developing regions often drives users toward cheaper or traditional alternatives such as clay-lined ponds.

Raw Material Price Volatility and Substitute Availability

Fluctuating polymer prices directly affect production costs and profit margins for liner manufacturers. The availability of substitutes such as geosynthetic clay liners and earthen containment solutions creates additional pricing pressure. Managing raw material sourcing and optimizing manufacturing efficiency are, therefore, critical to maintaining competitiveness.

Pond Liners Market Opportunities

Public Infrastructure and Water-Management Programs

Government-funded projects aimed at water conservation, irrigation efficiency, and wastewater containment present significant growth opportunities. National programs in India, China, and the Middle East emphasize lined ponds for water storage, desalination brine containment, and stormwater management. Suppliers participating in these initiatives can secure long-term contracts and recurring service revenues.

Aquaculture Expansion in Emerging Markets

The global push toward sustainable protein production is fueling aquaculture expansion, especially in the Asia-Pacific and Latin America. Fish and shrimp farming operations are rapidly adopting liners to improve water quality and reduce disease risks. Tailored products offering UV protection, puncture resistance, and microbial barriers are in high demand, presenting major opportunities for specialized manufacturers.

Material Innovation and Smart Liner Systems

Developing next-generation liner materials, such as reinforced geomembranes, bio-based polymers, and smart liners with integrated monitoring, is an emerging opportunity. These technologies enhance containment reliability, reduce maintenance, and meet rising sustainability expectations. Companies investing in R&D and offering integrated installation and monitoring services will differentiate themselves in the evolving competitive landscape.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1920 Million |

| Market Size in 2026 | USD 2096 Million |

| Market Size in 2031 | USD 3255.65 Million |

| CAGR | 9.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

HDPE liners dominate the market with around 38% share in 2025 due to their superior durability, chemical resistance, and cost-effectiveness for large-scale projects. EPDM and PVC liners serve mid-range decorative and agricultural applications where flexibility and UV resistance are valued. Composite geomembranes are gaining traction in industrial containment and mining due to enhanced tensile strength and multi-layer protection. The shift toward sustainable materials and prefabricated liner panels is redefining product differentiation and reducing on-site installation times.

Application Insights

Aquaculture applications lead global demand, accounting for approximately 42% of market revenue in 2025. These include fish ponds, shrimp farms, and hatcheries requiring reliable, non-toxic liners for consistent water management. Agricultural irrigation ponds follow closely, supported by government incentives promoting lined water-retention systems. Industrial applications such as mining tailings ponds and chemical wastewater containment are rapidly growing, while decorative landscaping remains a niche but high-margin segment.

End-Use Industry Insights

The agriculture and aquaculture industries dominate global pond liner consumption, collectively representing 45% of 2025 demand. Rising food and fish production needs, coupled with climate-induced water scarcity, drive liner adoption for efficient storage and reduced losses. Industrial end-users, notably mining and oil & gas, represent the fastest-growing segment due to stringent environmental regulations. The residential and commercial landscaping sector is expanding steadily, offering recurring replacement and renovation opportunities.

Explore more data points, trends and opportunities Download Free Sample Report

Pond Liners Market Segmentations

By Product Type

- HDPE Pond Liners

- EPDM Pond Liners

- PVC Pond Liners

- Composite Geomembranes

- Others (LLDPE, Polypropylene Liners)

By Application

- Agriculture & Irrigation Ponds

- Aquaculture & Fish Farming

- Industrial Containment & Mining

- Decorative & Landscaping Ponds

- Wastewater Management

By End-Use Industry

- Agriculture

- Aquaculture

- Mining & Industrial

- Residential & Commercial Landscaping

- Municipal Water Management

By Distribution Channel

- Direct Sales

- Distributors & Dealers

- Online Retail

- Specialty Construction Suppliers

- Government & Institutional Procurement

Regional Insights

North America

North America leads the global pond liners market with approximately 33% share in 2025. The United States accounts for most regional demand, driven by advanced industrial containment projects, regulated waste management, and high adoption in landscaping and aquaculture. The region’s mature infrastructure and early adoption of HDPE and composite liners ensure stable, long-term demand.

Europe

Europe holds around 25% of the global market in 2025, with Germany, the U.K., and France as key contributors. Strict environmental compliance standards and widespread adoption of geomembrane technology sustain demand. European buyers emphasize product recyclability and long service life, promoting innovation in eco-friendly liner systems.

Asia-Pacific

Asia-Pacific is the fastest-growing region, driven by agricultural and aquaculture expansion across China, India, Indonesia, and Vietnam. Government initiatives supporting lined irrigation ponds and fish-farming facilities are propelling growth. The region is expected to achieve double-digit CAGR in some markets, supported by urbanization, industrialization, and foreign investment in infrastructure.

Latin America

Latin America accounts for roughly 12% of the global market in 2025, led by Brazil, Chile, and Mexico. Mining and aquaculture activities dominate regional demand, while government-supported agricultural programs provide additional momentum. Expanding exports of HDPE liners from North America and Asia-Pacific are meeting growing local demand.

Middle East & Africa

The Middle East & Africa region represents a smaller but rapidly growing market segment. Water scarcity, desert agriculture projects, and mining containment requirements drive adoption in countries such as Saudi Arabia, the UAE, and South Africa. Infrastructure investments and renewable water management programs are likely to sustain growth through 2031.

Key Players in the Pond Liners Market

- GSE Environmental LLC

- AGRU America Inc.

- Firestone Building Products Company LLC

- Reef Industries Inc.

- BTL Liners

- Solmax International Inc.

- Naue GmbH & Co. KG

- Officine Maccaferri S.p.A.

- Layfield Group Ltd.

- DuraLine Corporation

- JUTA a.s.

- Carlisle SynTec Systems

- Plastika Kritis S.A.

- Gundle/SLT Environmental Inc.

- Environmental Specialists Inc.