Plant-Based Leather Market Size

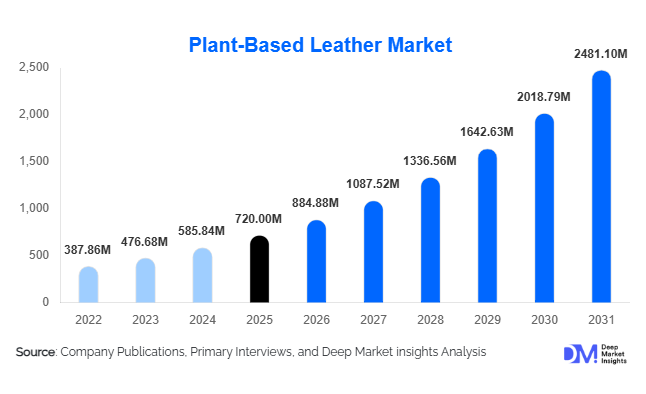

According to Deep Market Insights, the global plant-based leather market size was valued at USD 720 million in 2025 and is projected to grow from USD 884.88 million in 2026 to reach USD 2,481.10 million by 2031, expanding at a CAGR of 22.9% during the forecast period (2026–2031). The plant-based leather market growth is driven by accelerating demand for sustainable alternatives to animal leather, rising adoption across fashion and automotive industries, and increasing regulatory pressure to reduce carbon emissions, water consumption, and toxic chemical usage associated with conventional leather processing.

Key Market Insights

- Plant-based leather is rapidly transitioning from niche innovation to commercial-scale adoption, supported by luxury brands, EV manufacturers, and sustainable furniture producers.

- Mushroom (mycelium)-based leather leads material innovation, offering scalability, durability, and strong sustainability credentials.

- Europe dominates global demand, driven by stringent environmental regulations and strong consumer preference for cruelty-free materials.

- Asia-Pacific is the fastest-growing regional market, supported by cost-efficient manufacturing ecosystems and expanding vegan consumer bases.

- Footwear and fashion applications account for the largest consumption share, supported by high-volume sneaker, casual wear, and accessories production.

- Declining production costs and improved material performance are accelerating penetration into mass-market and automotive interior applications.

What are the latest trends in the plant-based leather market?

Rapid Commercialization of Mycelium-Based Leather

Mycelium-based leather is emerging as the most technologically advanced and commercially scalable plant-based leather segment. Continuous improvements in fermentation control, fiber bonding, and bio-coating technologies have significantly enhanced tensile strength, abrasion resistance, and moisture stability. Automotive OEMs and luxury fashion houses are increasingly entering long-term supply agreements with mycelium leather producers, signaling confidence in its durability and lifecycle performance. As production facilities scale and unit costs decline, mycelium leather is expanding beyond premium applications into mid-range footwear, furniture upholstery, and automotive interiors.

Integration of Circular Economy and Agricultural Waste Inputs

Another key trend is the increasing use of agricultural waste streams, including pineapple leaves, apple pomace, grape skins, and cactus fibers, as raw material inputs. Brands are prioritizing materials with strong circular economy credentials to meet ESG reporting requirements and sustainability targets. This trend is strengthening partnerships between plant-based leather manufacturers and agri-processing industries, enabling waste valorization while reducing raw material volatility. Materials derived from agricultural by-products are gaining traction, particularly in Europe and North America, where lifecycle transparency and traceability are critical procurement criteria.

What are the key drivers in the plant-based leather market?

Regulatory Pressure on Traditional Leather and Synthetic Materials

Stringent environmental regulations targeting chrome tanning, wastewater discharge, and VOC emissions are accelerating the shift toward plant-based leather. Regulatory frameworks such as REACH in Europe and state-level chemical restrictions in North America are compelling manufacturers to adopt low-impact materials. Plant-based leather provides compliance advantages while aligning with corporate sustainability and carbon-neutral commitments, making regulation a primary growth driver.

Rising Ethical and Vegan Consumer Preferences

Consumer demand for cruelty-free, vegan, and sustainable products is reshaping material selection across fashion, footwear, and interior design. Gen-Z and millennial consumers are particularly influential, favoring brands that demonstrate environmental responsibility and ethical sourcing. This shift is driving consistent demand growth for plant-based leather across both premium and mass-market product categories.

What are the restraints for the global market?

Higher Production Costs Compared to PU Leather

Despite cost reductions, plant-based leather remains more expensive than conventional PU leather due to complex processing, limited scale, and higher CapEx requirements. This limits adoption in price-sensitive markets and mass-volume applications, particularly in developing economies.

Durability and Performance Perception Challenges

Although material performance has improved, concerns around long-term durability, water resistance, and heat tolerance persist, particularly for heavy-duty applications such as automotive seating and commercial furniture. Overcoming these perceptions remains critical for broader market penetration.

What are the key opportunities in the plant-based leather industry?

Automotive Interior Substitution

Electric vehicle manufacturers are standardizing vegan interiors to reduce lifecycle emissions and differentiate brand identity. Plant-based leather offers lightweight, customizable, and sustainable alternatives to animal leather, creating large-volume, long-term supply opportunities for material producers.

Expansion into Emerging Consumer Markets

Rising disposable incomes and sustainability awareness in Asia-Pacific and Latin America are creating new demand pools for affordable plant-based leather products. Localized manufacturing and regional sourcing strategies are expected to accelerate adoption across footwear and lifestyle applications.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 720 Million |

| Market Size in 2026 | USD 884.88 Million |

| Market Size in 2031 | USD 2481.10 Million |

| CAGR | 22.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Sheets and rolls dominate the plant-based leather market due to their versatility and broad applicability across footwear, fashion, furniture, and automotive industries, accounting for approximately 46% of total market volume in 2025. Their flexibility enables manufacturers to meet diverse production requirements, from large-scale cutting for sneakers and upholstery to customized design for fashion accessories. Pre-molded components are gaining significant traction in automotive interiors, driven by OEMs’ focus on reducing production waste, improving assembly efficiency, and meeting sustainability mandates. Coated and laminated variants are increasingly utilized in furniture and hospitality sectors, where enhanced stain resistance, durability, and fire-retardant properties are critical. The adoption of coatings and laminates is further supported by growing demand for premium commercial interiors that combine aesthetics with long-lasting performance. Overall, product innovation and process optimization are key drivers for each segment, positioning sheets and rolls as the market leader globally.

Application Insights

Footwear continues to be the largest application segment, representing nearly 34% of global demand in 2025. High-volume sneaker and casual shoe manufacturing, particularly in North America, Europe, and the Asia-Pacific region, drives this dominance. Fashion and accessories follow closely, with premium and mid-range brands increasingly integrating plant-based leather into handbags, belts, and apparel, benefiting from sustainability-conscious consumer trends. Automotive interiors are the fastest-growing application segment, fueled by the rise of electric vehicles, OEM sustainability mandates, and regulatory pressure to reduce carbon footprints. Furniture and hospitality applications are steadily expanding, particularly in luxury hotels, commercial offices, and eco-conscious interior projects, where consumers prioritize sustainable and visually appealing materials. The combination of durability, aesthetic flexibility, and regulatory compliance underpins the rapid growth of these applications globally.

Distribution Channel Insights

Direct B2B contracts remain the dominant distribution channel, accounting for approximately 52% of global sales. Major automotive OEMs, furniture manufacturers, and global fashion brands increasingly secure long-term supply agreements to ensure consistent material quality and sustainability compliance. Brand-owned manufacturing and captive sourcing models are expanding among large fashion houses, particularly in Europe and North America, as they seek to maintain control over supply chains and guarantee product traceability. Third-party converters and fabricators play a key role in regional markets by customizing plant-based leather for specific end-use applications and adapting products to local standards. E-commerce and digital procurement platforms are gradually gaining prominence, enabling smaller brands to access specialized plant-based leather products efficiently. Overall, the distribution strategy is evolving toward closer collaboration between manufacturers and end-users to meet sustainability and performance requirements.

End-Use Industry Insights

Fashion and luxury brands remain the largest end-use industry, accounting for nearly 38% of total market demand in 2025. Mass-market apparel and footwear brands are rapidly increasing adoption as production costs decline and consumer demand for sustainable products rises. Automotive OEMs and Tier-1 suppliers represent the fastest-growing end-use segment, driven by electrification trends, ESG compliance, and increasing consumer preference for vegan and sustainable interiors. Furniture, hospitality, and commercial interiors are emerging as stable long-term demand contributors, particularly in Europe and North America, where regulatory frameworks and green building standards incentivize sustainable material adoption. The convergence of consumer preference, regulatory push, and technological advancements in material performance continues to shape the end-use demand globally.

Explore more data points, trends and opportunities Download Free Sample Report

Plant-Based Leather Market Segmentations

By Raw Material

- Mushroom (Mycelium) Leather

- Pineapple Leaf Fiber (Piñatex)

- Apple Pomace Leather

- Cactus-Based Leather

- Corn & Bio-Polymer Blends

- Other Plant Sources (Grape, Banana, Cork)

By Product Type

- Sheets & Rolls

- Pre-Molded Components

- Coated & Laminated Plant Leather

- Textured & Finished Surfaces

By Application

- Footwear

- Fashion & Accessories

- Automotive Interiors

- Furniture & Upholstery

- Consumer Electronics & Lifestyle Products

By End-Use Industry

- Fashion & Luxury Brands

- Mass-Market Apparel & Footwear

- Automotive OEMs & Tier-1 Suppliers

- Furniture & Interior Design

- Hospitality & Commercial Spaces

By Distribution Channel

- Direct B2B Contracts

- Brand-Owned Manufacturing

- Third-Party Converters & Fabricators

Regional Insights

Europe

Europe accounted for approximately 36% of the global plant-based leather market in 2025, led by Germany, Italy, France, and the U.K. The region’s dominance is driven by strong regulatory frameworks, such as REACH and European Green Deal initiatives, which incentivize low-impact materials and sustainable sourcing. High consumer awareness of vegan and eco-friendly products fuels demand in fashion, luxury accessories, and furniture. The presence of established luxury fashion industries in Italy and France, combined with technological innovations in mushroom and cactus-based leather, supports rapid adoption. Additionally, government-backed sustainability funding, R&D tax incentives, and EU-wide standards for sustainable materials provide a favorable investment environment, further accelerating market growth.

North America

North America represented around 28% of global market demand in 2025, led primarily by the U.S. Key drivers include increasing production of electric vehicles, a strong startup ecosystem for sustainable materials, and growing consumer preference for vegan and cruelty-free products. Major footwear and apparel brands are actively integrating plant-based leather to meet ESG goals, while automotive OEMs are adopting it for interior components in EVs. Regulatory incentives, such as state-level chemical restrictions and corporate carbon disclosure mandates, further support market expansion. Investment in local manufacturing facilities and collaborations with agri-waste suppliers strengthen supply chain resilience and reduce dependency on imports, contributing to sustained regional growth.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at over 26% CAGR, led by China, Japan, South Korea, and India. Drivers include cost-efficient production, increasing domestic sustainability initiatives, and rapidly expanding middle-class consumer demand for ethical and eco-conscious products. China’s investment in plant-based material startups, Japan’s preference for premium sustainable fashion, and India’s growing footwear export sector collectively support robust growth. Government programs promoting circular economy practices and bio-based innovation, coupled with rising e-commerce penetration, further accelerate adoption. Asia-Pacific also benefits from abundant raw material availability, including pineapple, cactus, and apple-based inputs, which lowers production costs and improves scalability for global export markets.

Latin America

Latin America is an emerging market, with Brazil and Mexico showing increasing adoption, particularly in footwear and accessories manufacturing. Export-driven demand is a major growth driver, as manufacturers target North America and Europe. Government programs supporting agri-waste utilization and sustainable manufacturing, combined with rising middle-class consumption of eco-friendly products, are facilitating market expansion. Additionally, growing awareness among fashion brands regarding carbon footprint reduction is driving adoption in premium and mid-range product lines.

Middle East & Africa

The Middle East is witnessing rising adoption in luxury automotive interiors and high-end hospitality projects, led by the UAE, Saudi Arabia, and Qatar. High disposable incomes, strong interest in premium interiors, and direct air connectivity to Europe and Asia support growth. Africa is emerging as a raw material sourcing hub for pineapple and agricultural waste-based leather inputs. Local initiatives promoting circular economy practices, combined with international investment in sustainable materials, are driving the development of supply chains and local processing facilities. Additionally, government incentives for export-oriented sustainable manufacturing enhance Africa’s role in supporting global plant-based leather production.

Key Players in the Plant-Based Leather Market

- Bolt Threads

- MycoWorks

- Ananas Anam

- Desserto

- Natural Fiber Welding

- Modern Meadow

- Vegea

- Beyond Leather

- Fruitleather Rotterdam

- Ultrafabrics Bio

- Spinnova

- Circular Systems

- Pangaia Materials

- BioFabrix

- Econyl Bio